Supported by Greenhaven Road Capital, finding value off the beaten path.

This post was part of a week of posts about Rory Sutherland. I learned many things, but broadly Sutherland speaks about four big ideas; creative thinking is hard but worth it, rationality is the wrong model, framing and choice architecture change decisions, and butterfly effects are easiest using psychology. There’s also a Rory’s reads post.

Ready?

If you liked the Be Different post, you’ll love this one.

Drinking the spreadsheet Kool-Aid leads to causality hallucinations. Life isn’t cause and effect and even if it were we may not pay attention. If we were homo-economicus then a change in the weather would lead to a change in the wardrobe. Plummeting stocks would lead to buying, not selling. We may think we are, but we are not homo economicus.

Homo economicus is the ‘species’ invented by Nobel Prize winner Richard Thaler. It’s the person at the perfect weight, with the optimal savings, and one who strides gaily and daily for their ten thousand steps. This species is the one that not only thinks that time is money but disagrees with Rory about longer but more enjoyable train rides because they know how much productivity is lost. Rory kindly disagrees.

“What you have to realize is that most human behavior doesn’t follow physical laws.”

“Marketing is the science of knowing what economists are wrong about.”

“Consumer capitalism is like the Galapagos Islands for understanding human behavior.”

We must move past standard economic theory and physics precision. Spreadsheet cells don’t have elbow room.

“That does not mean that changing human behavior does not involve science. What it means is it’s a different kind of science. It’s less like physics and more like climatology.”

We need to study something different rather than study nothing at all. Sutherland compares psychology to technology. Thought is code. The rational agent model implies that code is buggy – but it is what it is.

One example from – another Nobel Prize winner – Daniel Kahneman is ease of remembering. What people do, says Kahneman, is that we equate recall with accuracy. If asked about the value of international trade deals, your opinion will mostly be based off what comes to mind. The worker who lost his job will have on point of view. The person with no relation to the company another.

Rare is the person who will say ‘I don’t know.’ Why is that? Internal trade is a huge issue. It’s an idea that circles the world like a spool of thread around a globe. It’s complicated, but we don’t say that. Instead, we take the easy way out and believe that what comes to mind is the answer. Kahneman has an acronym for this idea; WYSIATS. What you see is all there is.

This system isn’t good or bad – it just is. When Gerd Gigerenzer asked German students to identify which city is larger, Detroit or Milwaukee, they largely guessed correctly. Americans did not. “I recognize that” is a good heuristic, writes Gigerenzer. That’s our code.

Sutherland wants people to understand that. In one talk he said, “My first very simple and important point to make is; psychology is technology…As you get better understanding these properties, technology gets better.” People are complicated. Here’s how.

Satisficing and maximizing. We tend to choose good enough results.

“Most real-life decisions aren’t like archery; aim for the ten, if you just miss you get a nine, if you miss that you get an eight. Most real-life decisions are more like darts. If you aren’t very good at darts aim for the southwest corner of the board. You won’t get a triple twenty but you won’t get a one or a five. The average score is better. This is called satisficing.”

Satisficing is good enough and it’s a helpful decision-making strategy.

“We are descended from people – whatever their other faults – who avoided making really really shitty choices…People pay a premium for brands not because they think Brand B is better than Brand A but because they’re more certain it’s good. It’s less likely to be terrible. It’s insurance against disappointment.”

When we buy brands we buy assurance. During the early days of mp3 players, there were as many devices as options for illegally downloading music for the device. It was great, but I couldn’t understand why Apple products were so popular. There was no logical reason for it. Apple wasn’t the behemoth they are now but their brand was still strong. The iPod satisficed.

“The idea is that when you make decisions in an uncertain setting, you have to care about not only the expected outcome, but also the possible variance. We’ll pay a premium not only for ‘better,’ but for ‘less likely to be terrible.’ That seems to be an important thing to understand when analyzing decision making.”

I recognize this as an iPhone owner. There are (probably) better phones than the one in my pocket, but I don’t want to take the time to learn a new operating system and research brands in an attempt to maximize my experience. I’ll satisfice instead.

Here’s another. Why is Airbnb a billion dollar company but no one talks about Craigslist rooms? It wasn’t always this way. During their early days, the Airbnb founders wrote a script to post rentals on Craigslist too. At some point Airbnb became “less likely to be terrible” than Craigslist listings.

“Once you understand the perfectly sensible evolutionary instinct to satisfice, then the preference for brands is not irrational at all: I will pay a premium as a form of insurance for the reduced likelihood that this product is appalling.”

Satisficing and maximizing are domain dependent. My wife maximizes family vacation plans while she satisfices family dinner plans. I’ll maximize my writing but satisfice the online hosting.

“If you are an expert in a field, you are a maximiser. Your car is Teutonic. You listen to relatively obscure Indie music. You wear niche clothes brands, like those funny jeans with a wiggle on them. You eat at restaurants you have learned about through recommendation or reviews. And go on holiday somewhere other than Spain, France or the USA. The maximiser seeks to find the very best of everything, and uses his consumption choices to define himself or herself apart from other people.”

Great brands are built around satisficers.

“To be great you need a few rich folks and a few poor folks; a few oldies and some young people. Nike’s extension of their brand belief to all sexes and ages is not a cop-out. It is proof of the brand’s greatness. As Andy Warhol said of Coca-Cola: ‘The great thing about Coke is that the president of the US drinks the same Coke as the bum on the street.’”

“Is Red Bull an energy drink or a mixer? What is the user-imagery of Amazon? Who is the typical Google user? What makes Google better? The fact that we cannot answer these questions simply would typically be considered a flaw.”

We use clues for decision making. They can be internal – I recognize that. They can be external – let’s follow the crowd. They can be aspiring – I’ll maximize. They can be avoiding – I’ll satisfice. Sutherland’s goal is to get people to think in these terms.

Rationalizing.

Satisficing and maximizing is not how most people see themselves. We’re wiser, less whimsical. This is the story we tell ourselves. In his conversation with Rory, Danny Kahneman said:

“When you need information that you don’t have you usually aren’t aware that you need it. If you have partial information about something you will make the best story possible out of the information you have. And your confidence will be determined by the coherence of that story.”

What Kahneman has found in research, Sutherland has found in people’s minds and mouths. Take toothpaste for example:

“Why do we prefer stripy toothpaste? When you think about it, once you put the toothpaste in your mouth, you mix it all up. Why does it need to be stripy?

“The strangest thing on the web is, there are hundreds of articles saying how they make the stripes in toothpaste but there’s no article saying why. All those materials, the red, and the blue, and the white get mixed up in your mouth. It’s completely pointless.

“Why do you do it? Something about the human brain just thinks if there are three different colors, it’s easier to believe that that toothpaste is doing three different things: banishes plaque, freshens breath, eliminates cavities. Because there are three colors, I find it easier to believe that this thing is doing three totally different things.”

That’s one way we rationalize. Google, Sutherland thinks, does another. Because they began offering a single search bar on a simple web page, people assumed they were better at search.

“People believe something that only does one thing is better at that one thing than something that does that thing and something else. It’s called goal dilution.”

In his presentations, Sutherland often includes these lyrics from Bob Dylan’s Brownsville Girl.

We can rationalize almost anything – and have done so for hundreds of years. Benjamin Franklin praised our reasonability, “since it enables one to find or make a reason for everything one has a mind to do.” Kahneman took this thinking, researched it, and wrote a book about how we think fast and slow. He told Sutherland.

“If I say two plus two a number comes to mind. You didn’t ask for it, it just came. The capital of France, a word comes to mind. If I say a nasty word like ‘crime’ you have an emotion. You didn’t ask for it, nothing deliberate, it just happens.

…

“Most beliefs come from childhood but we build arguments. We pretend that we got to our conclusions from arguments when in many cases it isn’t true.”

Sutherland also likes the quote from George Loewenstein, “just as we have a sex drive and a food drive, we have a sense-making drive.” Academic researchers (and business marketers) study (and exploit) this gap. They know it’s there because if you change small things a behavior changes.

Here’s an example. Once upon a time, there was a very nice hotel. To celebrate the season, the hotel commissioned an ice sculpture for their lobby. It would be the cherry on the sundae of a great stay. Only things didn’t work that way.

What really mattered for the guests was check-in. If guests had a great check-in experience; a short line, kind staff, ready room – then they rated their entire stay as better. The music sounded better, the room was cleaner, the ice sculpture was more beautiful. However, if the check-in experience was bad then the entire trip was shit.

“Everything we judge is based on our prior expectation…the idea that there is just this thing called ‘Utility’ which is produced in a factory and is completely disassociated from the context in which the thing is consumed is not happening.”

“The price of things is not an absolute. We don’t have an internal measure of pleasure against which we measure our expenditure – it’s completely relative.”

We rationalize. If check-in is disorganized then the room can’t be that nice. Stories color in details and smell of certainty. This is part of the reason Uber succeeded. The app created a chance for stories (and certainty).

“The nature of a wait is not just dependent on its numerical quality – it’s duration – but the level of uncertainty you experience during that wait…The human brain doesn’t care so much about duration as about certainty…Uber let us make stories about where our cab was.

“What makes Uber different is that when you phone for a taxi, in between that phone call and the taxi arriving, you enter the Twilight Zone of uncertainty. ‘Where is he? Why isn’t he here yet? They said five minutes. I can’t see him. Maybe he’s outside. Should we go outside and have a look? What if he’s left?’

“With Uber you watch the cab approach in real time on your map. And you go ‘Oh, look, he’s stuck at those traffic lights. I’ll make myself a cup of tea while I’m waiting.’ And you’re both happier, you make better use of the time but you’re also vastly less stressed in that period. Now, simply knowing that is really, really important. We don’t like uncertainty.”

Jason Calacanis agrees. He said that live maps is why Uber worked and previously similar services didn’t.

Companies with cheaper products need to account for this storytelling. One of our simple-and-useful-but-not-perfect heuristics is that expensive is better. That’s not always true. Sutherland jokes that a king of yore would give you half his land for a flat screen television. Things get better and cheaper. Homo-economicus celebrates this. We do not. Instead, we think:

“There must be something wrong here. Even though that product seems better, if it’s cheaper that must mean it’s shit in some dimensions I don’t currently understand.”

“Marketing is much more complicated than people realize. It’s not only justifying a higher price but it may also be about de-stigmatizing a lower price.”

Sutherland praises the way low-cost airlines have approached this. They fill in the story for us. It’s cheaper because there’s less.

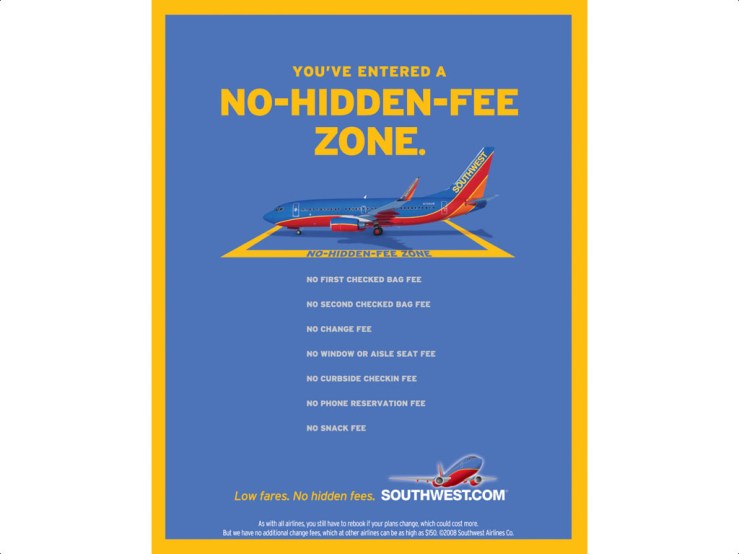

Look at this Southwest Airlines advertisement. The “no-hidden-fee zone” is the explanation for the price. The implication is that the other airlines are more expensive because they have hidden fees whereas Southwest is upfront about it. They tell you a story.

This isn’t just about dollars, it’s about sense too. Sutherland recalls taking a flight and, rather than unloading at the gate, they unload via stairs and take a bus into the terminal.

“Every single passenger on a plane, in those conditions, generally goes, ‘Aw shit. I’ve been shortchanged here. I kind of paid you for that service. The least you can do is at least connect me to a proper gate with a tube. Now you just dump me on the tarmac and putting me on a bloody bus.’ Partly because ‘bus’ automatically creates the assumption of second best-ness in our mind.”

However, Sutherland had an insightful pilot. After announcing the change, he said that the bus would take the passengers straight to the passport control so they wouldn’t have to walk far with their bags.

“Hold on. That’s always true isn’t it? When you get a bus, it takes you right next to passport control so you don’t have to schlep passed 700 yards of duty-free shops in order to actually get to your luggage and then get to the arrival zone.”

The facts are the same but the rationalizing is what makes an experience great – or not.

“Here’s a case where you can take something that’s bad, redirect our attention to the good bit of it, and we now think it’s good.”

One other example is the Nespresso machine. How do people rationalize using this machine?

“Objectively they are insanely expensive. If you had to buy Nespresso coffee in a jar like Nescafe, per equivalent dosage of caffeine, a jar of Nespresso would cost about sixty pounds. You’d look at that on the shelf and you’d go, ‘That’s insane!’ I could buy Nescafe for only five or six euros.

“But it doesn’t come in a jar. It comes in little a pod. So the frame of reference isn’t Nescafe, it’s a coffee shop. You think, ‘In the coffee shop I’d be paying one pound twenty. This little pod cost me twenty-eight cents. This machine is practically making me money!’ Our perception of things is relative. What you compare something to matters much more than whether the thing is expensive or not.”

We aren’t rational but we don’t need to be. Rules of thumb work for a lot of things. For other decisions, we satisfice to avoid downsides and rationalize after the fact. Producers can use this information to help people tell themselves these stories. This is done by framing (coming tomorrow).

Thanks for reading.

{kind=link}