Richard Thaler (@R_Thaler) joined Barry Ritholtz (@Ritholtz) on the Bloomberg Master’s in Business podcast to talk about his new book; Misbehaving: The Making of Behavioral Economics, the story of both Thaler and BehavEcon’s paths to prominence. Thaler is also the author – with Cass Sunstein – of Nudge

Thaler noticed something odd early in his career. One day he gave an exam to students. The average score was 72, and in general the students were not happy about it. They let their professor know.

Thaler thought about the test and concluded that it was fair, but what could he do about the grousing? What if, he wondered, the total points changed. Rather than be out of 100, the exam was out of 137 points?

He implemented the new exam and the new average score was 96. Now, here’s where things get interesting. Even though it was a lower average score (70% vs. 72%) almost no one complained about the difficulty.

What gives? Standard Economic Theory says that there should have been more complaints. It’s not taught in college statistics but everyone knows that; exam scores are inversely related to exam complaints. The model didn’t work and Thaler’s career discoveries began.

Models and theories are good, but not perfect and something we should remember. In Filters Against Folly

(Technology reliability) x (Human reliability) = (System reliability)

My iPhone works only as well as the engineers who programed it. The Apple Maps hoopla in September 2012 demonstrates this. The technology to navigate existed, other apps had done it for years. My iPhone had done it with Google Maps. The problem was with the Human Reliability variable.

This set of notes will rest as much on the book as on the interview. Thaler’s talk with Ritholtz was good, but even better after I read the book. Your takeaway value will vary accordingly.

That’s not to say we won’t learn anything though. Questions we can aim to answers.

- Why are we bad at big decisions?

- Are Econs and Humans the new Odd Couple? (step aside Felix and Oscar)

- When should you buy stock in $CUBA?

- What’s the newest modern architecture? (Hint: it’s not Deco)

- Why do you love a good deal on Beats headphones?

- Why does it feel so bad to lose those headphones?

- Why should you never buy basketball tickets from someone who had to camp out to get them?

- Why does someone who drives a Lexus want to save money on gas?

- Why is Daniel Kahneman so brilliant?

Let’s learn.

Decision making – Why are we bad at big decisions?

We stink at making big decisions says Thaler. It’s not really our fault though, we don’t get much practice. I know what kind of ice cream to get (Pistachio or chocolate), but not what career to choose (freelance or higher education). The infrequent choices though are often the most important ones. If there were some way to get better at making those, then we might see some big improvements in our lives.

It’s not a short list either. Whether to take a job, whether to transfer, whether to go back to school, and whether to work when your kids are young, are all big(ish) choices just for your early career. Add in relationships, investments, and life or death moments and we get a Pandora’s box of options.

But, the good news is that we can get better at making decisions. There are many tools, one of which is to ask, does this solve the smallest possible problem?

It’s easy to get caught up in big problem because those are the ones that seem worth solving. Small problems don’t matter until they build up into big problems, and then we have a serious situation to solve. Much like unraveling a single pair of headphones is annoying, but doable. Once 10 or 100 get entwined then things get quite messy. Within any big problem are lots of small problems to untangle first.

When Mark Ford worked for a financial newsletter company he was focused on doing it right. Ford, the editor, spent about half his time to create a formatting guide for the writers to use. That way, his newsletter would be distinct, professional, and consistent. Guess what? No one cared.

Ford realized his mistake one day. The readers didn’t care what the style was. They didn’t care that there was a tone or how it was unique. Ford quit working on the style guide and began writing better articles and that’s when the publication grew. Ford was solving a big problem – what type of writing do people want to read – rather than the smaller one – what do our subscribers want to read?

Fellow writer James Manos was in a similar situation. In 1998 Manos was hired to be a writer a new television show. It was a new kind of show and it might turn into something big. Manos though didn’t worry about any of that.

For Manos the secret wasn’t to think about any big ideas around the show or its role in culture at large, he said his only focus was to write compelling characters. That’s the smallest possible problem for a television show writer, how do I make these characters ones people will watch?

Manos succeeded – along with the other writers involved. That new show was The Sopranos and the episode Manos wrote was College – one that many people think is the best episode of the show.

Gretchen Rubin was with a friend who complained about her job. “Well, what is it you don’t like?” Rubin asked. After a list of mostly inconsequential things – stuff anyone complains about – her friend focused on the real sticking point – the commute. Rubin suggested she listen to audio books and now her friend loves it. Solve the smallest possible problem first

The Odd Couple, Econ and Humans

Thaler’s experience with his student’s test results (and replies) combined with his economic understanding brought up an interesting question. Why do the models suggest one thing but life looks like another?

The models, says Thaler, assume that people operate like “Econs.” This super-rational person is one who will maximize her retirement and, Thaler’s words, “are as smart as the smartest economist.” That is not who we really are.

We don’t save enough for retirement, we don’t have hangover free weekends, we don’t make the optimal career and education choices. What gives?

These situations are “a piece of cake for econs,” says Thaler, but as humans we have bounds to what we can and do think about.

Thaler began keeping what he called, “The List.” A collection of instances where standard economic theory diverged from human behavior. The list examples began to include things like “bounded rationality” (we are rational, to a point) and “hindsight bias” (of course you knew all along that a thing would happen). At the start of his career (~1976) these were new ideas. Now we use them all the time.

Mark Cuban says that hindsight bias is something that his team sees a lot, and tries to remove from their decisions. Like a single hair can ruin your soup, a single bias can ruin a decision making system.

After one particular trade Cuban says they got “crushed” by the fans and media. The fans and media of course knew better, they were the wise ones who foresaw the debacle and knew that the team was too old (hindsight bias against the trade). While that season ended poorly, the next one didn’t as Cuban’s team won the NBA championship, thanks in part to the veteran leadership (hindsight bias in favor of the trade).

These were the sorts of things Thaler noticed 40 years ago. The trouble was, how could he prove his point. The answer was lots and lots of work into the headwinds of long head beliefs.

Efficient Market Hypothesis – $CUBA stock shenanigans

Another stone in Thaler’s academic shoe is that the stock market is efficient. This idea includes the assumptions; 1, we can’t beat market and 2, prices reflect intrinsic value. That some people do beat the market and that prices which should be the same are actually different seem like counterpoints. Let’s start with $CUBA.

In late 2014 the stock jumped from $7 to $14 in two weeks. The catalyst was President Obama’s announcement of the change in diplomatic status for the country. Hooray!

It makes sense that $CUBA would increase, the fund was created for such a situation, with holdings in companies that would benefit from this news. But, here’s where things get interesting, that jump was too high. The stock was trading 42% higher than Net Asset Value.

$CUBA fund (w/ no Cuban holdings) now trading @ 42% premium to NAV. @ReformedBroker's a seller thereformedbroker.com/2014/12/17/don… http://t.co/C3omkGaFuP—

Charlie Bilello, CMT (@MktOutperform) December 20, 2014

This would be like walking into the Gap and looking at one of their mannequins and saying to the eager teen with a headset, “how much for the outfit.” The teen – speaks into his and types on a tablet that seems a bit unnecessary – will reply that the outfit is $140 and your size is bagged and ready at the checkout. Just one thing, you can’t wear the clothes until next year.

Hmm, you say, the price is a touch high, the convenience is nice, though the timing is a bit restrictive. Wanting a good deal – you’re at the GAP after all – you ask, “how much if I just find the items myself?” To which the clerk replies, “then it’s only $100.”

This is the story of $CUBA, a closed end fund with a basket of assets you could buy on your own – and it’s an example of why markets aren’t perfectly efficient.

Another story is the one of Long Term Capital Management. In 1998 with a Russian default and communal (hedge fund) leverage predicament, LCTM was stuck in a hard spot. They wanted to sell some positions to have more cash for others but there was one problem, everyone else was in the same boat. The boat had all sellers and no buyers. Which drove prices down, which furthered LCTM’s problem.

There was nothing wrong intrinsically wrong with some of their positions. One of which was a bet that the stock prices of Royal Dutch Petroleum of the Netherlands and Shell Transport of England would converge. Why would someone think that the prices of the two companies would come together? Well, their income was from the same source. Unfortunately for LCTM, but fortunate for people who like good books

As the Keynes quote goes, “markets can remain irrational longer than you can remain solvent.”

All that said, this detective work is really hard to do. In his book, Money

So what do you do?

Warren Buffett’s advice is this; buy a low cost index fund and treasuries. This is literally what he tells Tony Robbins he would tell someone to do for his wife if he passed away. If you aren’t going to be a full time investor who dives deep, that’s the only thing to do.

James Altucher, who once ran a fund of hedge funds writes this:

“Warren Buffett, Steven Cohen, all the great investors go outside every day and they want to take your wallet, steal your diamonds, maybe slash your face for fun, and then after they’ve gotten everything they can get from you, they are going to shoot you in the head in front of your child and run off into the dark of the night. Good luck fighting that kind of competition.”

The takeaway is this: markets are not entirely efficient but you’ll need at least brains, luck – and the LCTM lesson – and humility to find those flaws.

Choice Architecture – The Modern Architecture

Thaler’s next move wasn’t to beat the market, but to think about how to get people to make better choices. If we aren’t Econs but are Humans and if the efficient market is full of bubbles, what can we do?

We can nudge people.

In his book, Nudge

Ritholtz says that he saw a nudge at a Brussels airport escalator. One one side are painted feet that mimic standing, the other side walking. This nudge helps people figure out which side to walk on and which side to stand on.

Or, think about when you order a new computer from Apple, someone there has to decide on a shipping choice. In some cases people may not want to pay extra for immediate shipping (though “the best piece of advice” below says they will) and can use their old computer for a few more days.

Other people will be there because their old computer broke and they NEED a NEW one NOW. There isn’t a shipping option fast enough. If you were the person at Apple who designed the checkout process, what would you choose as a default?

These were the situations that Thaler wanted to find and make better. His angle is that nudges are nice for things like escalators and shipping speed, but not that important. We get enough experience with ordering things from place like Amazon that we know how fast we need something. That’s small potatoes.

What we need help with, says Thaler, are with the big choices like retirement. Once he realized a way people consistently acted differently from the optimal choice, we could get people back on that course with a nudge.

The best example is Thaler’s Save More Tomorrow program. This system encourages employees not to save more for retirement today, but to invest their next raise. We like to eat dessert today and plan to exercise tomorrow, and in effect that’s what the system does.

Because it operates out of sight, (how often do you look at your check?) it works well. This out of sight, out of mind method of optimization can work for a host of reason.

Subscription services do this quite well with their recurring revenue model. Rather than have to pay each time, and see the cost, have the payment automatically withdrawn.

In his book Mindless Eating

Transaction Utility – Why we love Beats headphones.

One of my favorite ideas that Thaler explains is “transaction utility.” I’m glad it has a name. Transaction utility is the excitement you get from getting a deal. It’s why people tell you what they paid for that great vacation before they tell you about the vacation. The deal is part of the thrill.

It reminded me of the podcast between Brian Koppelman and Seth Godin where they talked about headphones. Godin said that he sees the placebo effect with regards to people and their headphones. People pay more for a brand (Beats in this case) they think are good and because they think they have a good pair, they have a better time. This is clearly the placebo effect Godin says, and there’s nothing wrong with it.

Koppelman – as an audiophile himself – uses a much better brand, but even in that Godin says there is some self trickery afoot. Godin says that Koppelman not only likes the headphones, but likes to know that he’s the kind of person who knows the difference among different kinds of headphones.

We love to think we are getting a good deal.

We use ideas like “transaction utility” as the fulcrum for our logical levers. Thaler says, drive by any Costco and count the cars worth more than fifty grand. There’s plenty of them. But do they buy in bulk to save money?

No, they buy in bulk because they like to be someone who buys in bulk to save money or who needs to buy in bulk because it’s convenient.

Another nugget of transaction utility is to have a membership or season pass. When our family goes to the zoo it feels free-ish because our annual membership (paid each Christmas, thanks Grandpa!) covers the price of parking and admission.

But the deal is really for the zoo. I have a hunch that the zoo gets a bit more money in total because these trips feel free. Anecdotally, we seem to have ice cream or souvenir treats (especially if grandparents accompany us), in part because of the “great deal” to get in.

Loss Aversion – Why we hate to lose those headphones.

Man we hate to lose things. Losing anything is worse than gaining the same thing back. Psychologist call this “loss aversion.”

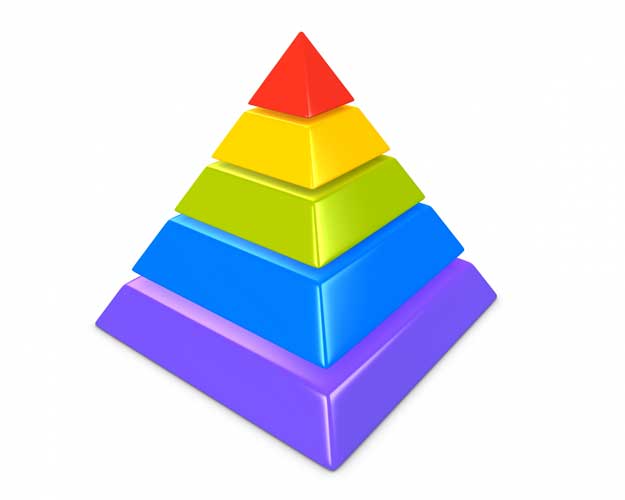

And the thing is – it hurts more than it feels good. The good vibes for finding a $20 bill are offset by a loss of only $10. Thaler says that we’ve always been wired this way. I’ve known about this theory a long time, and never had a good understanding of it until I heard the pyramid comparison.

One thing economist do agree is on that the next thing is less valuable than the previous thing (called “diminishing returns”). Your first car is great, your second one is nice to have.

One thing economist do agree is on that the next thing is less valuable than the previous thing (called “diminishing returns”). Your first car is great, your second one is nice to have.

The same can be true for dollars, chocolate cake, and vacation days. Now that we agree on this, or at least demonstrated its commonality, let’s make a pyramid.

Image that how much you value the first thing is the base of the pyramid and each subsequent (because we value it less) is smaller. This works as we go up the pyramid, each dollar/piece of cake/vacation day we add is nice though it’s niceness is smaller than the previous one. As we build our pyramid we can start to see how loss aversion might work.

Imagine you’re at the top of the pyramid and instead of being handed the next smallest dollar/piece of cake/vacation day, you’re told by someone on the ground that they want the previous one back. That previous one is bigger than the one you were about to put on, and so you give away something nicer than the next thing you would get. That’s loss aversion.

The good news is that this problem isn’t written in stone, even though our analogous pyramid might have been. Loss aversion lies in the loosey goosey world of emotions. Much like funhouse mirrors can reframe a situation, we can create conditions that make us feel better. We might not get over feeling bad about loses, but we can reframe loses into deals.

Josh Brown wrote about a trick during the 8/24/15 equity correction. According to Brown, here’s a surefire way to feel better.

Step 1: “I pick five or six of the best stocks in America that I’ve missed out on – the ones that have always bothered me. Everyone has their names. A contemporary list might include Netflix, Amazon, Facebook, Disney, Celgene, Starbucks, Chipotle, Goldman Sachs, etc.”

Okay, find the things you always wanted to invest in but were too expensive. Got it. What’s next?

Step 2: “Now I go to my quotes screen to see where they’re currently trading and I come up with utterly absurd prices at which I would buy them.”

Okay, they’re still quite high despite the correction, but we can imagine a price that’s too good to pass up. Got it.

Step 3: “I create GTC (good till cancel) Buy Limit orders for a handful of these stocks at the exact absurd prices I’ve come up with. The Buy Limit order will not allow my trade to get executed until the price I’ve specified is reached. I won’t end up with the long position unless it’s on my terms.”

Ah, so we program the computer to buy those stocks if they actually reach sale prices. If we get to buy that low we can be proud of our investing acumen. Ha, rather than lose, I win!

Just one thing, don’t get too attached to those stocks, and if you buy them get ready for your next bias, the endowment effect.

Endowment Effect – Duke basketball tickets edition

We humans are so silly. Let’s look at just one way. When Dan Ariely, a fellow misbehavior, was at Duke, he wanted to know how students really valued basketball tickets. Duke has this quirky lottery where students camp out the night before for a ticket lottery that gives them the chance to get tickets. Some win, some don’t, but anyone who camps out hopes they might.

Luckily for Ariely this provides a great natural experiment.

You see, says Ariely, we have basically two identical groups (undergraduate students at Duke University who were college basketball fans who were also willing to camp out in hopes of tickets) that received different treatments. One group received treatment “ticket,” the other treatment “no-ticket.” The question is, would these groups value tickets the same amount? If not, the only difference appeared to be whether or not they got a ticket.

At this point you probably expect a twist, and you’re right. Thaler saw this twist a long time ago when his professor would restrain from drinking or selling his expensive wines. Because he owned them, they meant more to him. The same was true for the Duke basketball tickets.

Ariely and his researchers began to call the students under the guise “we may be able to sell you a ticket.” Their average buyers prices was about $170. Then they called the students who had won tickets and their average selling prices was about $2400. Yep, a 15X difference.

Ariely writes about this study in Predictably Irrational

“What was really surprising, though, was that in all our phone calls, not a single person was willing to sell a ticket at a price that someone else was willing to pay. What did we have? We had a group of students all hungry for a basketball ticket before the lottery drawing; and then, bang— in an instant after the drawing, they were divided into two groups— ticket owners and non– ticket owners. It was an emotional chasm that was formed, between those who now imagined the glory of the game, and those who imagined what else they could buy with the price of the ticket.”

Thaler introduced the endowment idea early on in his book and writes, “although I had misgivings about some of the material presented in classes, I was never quite sure whether the problem was in the theory or in my flawed understanding of the subject matter.” It turns out it was the subject matter.

It’s partially why home owners overvalue their own homes. We tend to overvalue the things we own and the more hoops we go through to get it – like camping out the night before and making it through a lottery system – raise our value of those things.

The best piece of advice yet – Why Lexus owners want to buy cheap gas

For all the good ideas that Thaler and Ritholtz talk about, the most powerful on to me was the Weber-Fechner Law. It says that we only notice differences in proportion to the original. Simply, you’ll choose to save a dollar on a gallon of milk that cost $3.50, but won’t take any extra effort to save a dollar on a winter jacket. That dollar seems larger because of the small starting price.

Going back to our computer example, it’s also why we may choose to have the computer rushed to us. What’s another $20 on an $1100 purchase?

Robert Cialdini writes in his book, Influence

“Simply put, if the second item is fairly different from the first, we will tend to see it as more different than it actually is.”

It’s why it’s more common to sell someone a shirt after they bought a suit, rather than the opposite.

All the academic papers I’ve read on this focus on this sort of comparison, but how often do we end up in situations like that? My big purchases are infrequent and my desire to search for small savings slim. But I began to wonder, does it apply to non-monetary domains as well. So I asked Dr. Thaler

And he responded!

It matters then for our time as well. It means that on a short commute to the office, you’ll be more likely to drive fast to save thirty seconds than you will to drive fast to save thirty seconds on a long trip to the beach.

So, should we change our behavior? I don’t know.

The best course, I think, is just to be aware why we do what we do. I eat ice cream because I enjoy it, but I know what would happen if that’s all I ate. Awareness, not exploitation or efficiency or econ-thinking may be the best course.

Tren Griffin writes that Charlie Munger uses a two track system where, “the second process involves looking at subconscious influences which can cause an investor’s thought process to malfunction.” Munger doesn’t change an action because of a bias, he just checks it. Michael Mauboussin too tries to guard against these sorts of mistakes. Knowing about biases is like knowing the weather. They may not change your plans, but it’s good to have an idea about how severe they may be.

And speaking of biases, we now go to Kahneman.

Daniel Kahneman

Thaler says to Ritholtz, “I claim to have discovered Daniel Kahneman,” and while it is tongue in cheek, it’s worth noting. Kahneman’s Thinking Fast and Slow

- Michael Mauboussin is a big fan of Kahneman’s idea of base rates. This comes up in Thaler’s book too.

- Peter Thiel’s post has a section on in/out group think. This idea also comes up in Thaler’s book.

- Maria Popova’s post references Kahneman’s expression, “what you see is all there is,” about our conscious recall and the biases that stem from that.

Favorite books

The interview ends with Thaler sharing some book recommendations. “Catch-22

–

Thanks for reading, I’m @MikeDariano on Twitter. If you know the source of the pyramid analogy as it relates to loss aversion, please let me know. I have a monthly newsletter where I share the things I read – like Misbehaving or Thinking Fast and Slow. You can sign up here.

[…] Thaler interviewed with Barry Ritholtz on the Masters in Business podcast and I wrote up those notes at The Waiter’s Pad. […]

LikeLike

[…] Richard Thaler […]

LikeLike

[…] Richard Thaler […]

LikeLike

[…] psychology and neurology and it’s worth pointing out here. The psychological component is what Richard Thaler discussed in his interview with Ritholtz. It’s the idea that we respond to our environment […]

LikeLike

[…] have what Richard Thaler calls, “transaction utility.” They get enjoyment from being a type of buyer. How often have […]

LikeLike

[…] a brother from another mother, Richard Thaler had the same experiences. Thaler too was learning about rational markets. Except, Thaler thought, […]

LikeLike

[…] Evan Goldberg said writing block is just a term for a bad week, not a persmanent stoppage. Richard Thaler created his entire career on the idea that the way people frame something changes how they see it. […]

LikeLike

[…] He says, “I think of writing as very modular.” Pieces can be put together or taken apart, and it’s no big deal. Except it was for Richard Thaler. […]

LikeLike

[…] is wonderful. Richard Thaler wrote about nudging was born in Misbehaving and how it was applied in […]

LikeLike

[…] – August says that he writes by hand to avoid correcting something he’s written. It’s easier to hit the backspace key than erase. This is a good example of how small barriers can stop an action. Tiny obstacles can help us stop us from snacking or make better financial choices. […]

LikeLike

[…] people have something – or even imagine having it – they feel more strongly toward it. Richard Thaler did wonderful research on this. Thaler walked into his classroom and handed out coffee mugs to half […]

LikeLike

[…] Richard Thaler writes about the famous “beauty study” in his book Misbehaving. The aim was to make a guess that voted and weighed an idea. […]

LikeLike

[…] not just about the actions or reactions but the reactions to the reactions. Both Ken Fisher and Richard Thaler explain it in terms of the “beauty contest.” Tyler Cowen displayed the thinking in regards to […]

LikeLike

[…] to this is loss aversion, which Richard Thaler explains beatutifully with a pyramid analogy. Also in that post is how Josh Brown creates win-win […]

LikeLike

[…] aversion is a powerful emotion. The best story about loss aversion comes from professor Richard Thaler (author of the aforementioned […]

LikeLike

[…] humans are playing the game, they will do dumb stuff. When Richard Thaler began research that would form behavior economics he actually kept a list of theories title, […]

LikeLike

[…] Richard Thaler guessed that part of the reason the standard economic model has yeilded so little to the behavioral economic model is due to the sunk cost bias. People invested too much of their careers to give it up. […]

LikeLike

[…] rates. Ditto for automatic (the default) enrollment in retirement plans. Nudges are powerful. Richard Thaler knows […]

LikeLike

[…] prove a computable measuring tool, but stories (psychology) matters too. Richard Thaler built his work around the shift from numbers to stories. Our brains evolved for […]

LikeLike

[…] Even though Marks came up through the Booth School of Business in Chicago, he doesn’t believe entirely in the Efficient Market Hypothesis. “I do not believe the consensus view is necessarily correct.” (Ditto for fellow Alum Richard Thaler) […]

LikeLike

[…] on Northern Pipeline company. Judith Elsea does the same thing, only with an algorithm. Richard Thaler did it with a list of things stupid people […]

LikeLike

[…] Richard Thaler had this see-it-to-believe-it moment when he read Daniel Kahneman’s paper. Ezra Klein had this when he read Matt Yglesias. Judd Apatow had it when he saw Steve Martin. […]

LikeLike

[…] Richard Thaler had this moment when he read Value Theory. “Now I can think that,” Thaler told Michael Lewis. Oh, I can study this theory. […]

LikeLike

[…] Richard Thaler noted how this played out in his book, Misbehaving. […]

LikeLike

Have you ever considered about adding a little bit more than just your articles?

I mean, what you say is valuable and everything.

But just imagine if you added some great images

or videos to give your posts more, “pop”! Your content is excellent but

with images and videos, this site could undeniably be one of the best in its

niche. Awesome blog!

LikeLike

Thanks. Will try to do this.

LikeLike

[…] ever found. They loved that.” That is, Meyer found out about transaction utility, something Richard Thaler […]

LikeLike

[…] like Kyrie Irving – come to mind. Psychologists like Daniel Kahneman and economists like Richard Thaler wrote that because we are cognitive misers we tend to equate how easy an idea comes to mind with […]

LikeLike

[…] Richard Thaler‘s book, Misbehaving covers this period of time where Sutherland was adapting his approach, with the same sort of that’s interesting attitude. […]

LikeLike

[…] Richard Thaler kept a list of “dumb things people do” in this office. […]

LikeLike

[…] Richard Thaler pointed out that Humans and Econs are different decision-making species. As Humans we need help getting a different perspective. Sometimes this means physically changing your point of view. Jocko Willink was leading a training exercise for soldiers and one guy couldn’t participate because he was injured. Instead, he observed the situation from where Jocko sat – only a few feet away – and commented how easy everything looked from that vantage. […]

LikeLike

[…] Judd Apatow and Joe Rogan saw comedians. Alton Brown went to Tuscany. Ezra Klein read a blog. Richard Thaler read Value […]

LikeLike

[…] all start with a default choice, wrote Richard Thaler, might as well make it a good one. A Default No keeps us out of things. Pat Dorsey told Patrick to […]

LikeLike

[…] Seides on Capital Allocators. I can’t get enough of these behavioral economics folks. From Richard Thaler to Rory Sutherland – if you have some favorites let me […]

LikeLike

[…] Sunstein. “A tremendous book.” “I’m a big fan.” I’ve written a post about Richard Thaler and also enjoyed his book/biography […]

LikeLike

[…] Richard Thaler warned Barry Ritholtz, “If you have a certain lens that you look at things through, then you’re gonna see everything to be consistent with your point of view.” […]

LikeLike

[…] a 2005 paper, Overconfidence vs. Market Efficiency in the National Football League authored with Richard Thaler. Massey now consults with teams because, “They want fresh eyes looking at things but they also […]

LikeLike

[…] is probably the best application of the behavioral economics work done by Kahneman, Tversky, and Thaler. Halpern reflected, “We’re not very good at estimating the absolute value or price of […]

LikeLike

[…] invasion of Ukraine the availability is even greater. And that’s not all! Thanks to our mental accounting we perceive pain at the […]

LikeLike