Supported by Greenhaven Road Capital, finding value off the beaten path.

This is our fourth(!!) post from a Michael Mauboussin podcast. There were these; Michael Mauboussin and Michael Mauboussin from conversations with Barry Ritholtz, and one – Michael Mauboussin – from The Knowledge Project podcast.

I think what appeals to me about Mauboussin’s interviews is his clarity of explanation. In his talk with Ted Seides he draws from The Santa Fe Institute, Complex Adaptive Systems, investing research, Brian Arthur, Steve Jay Gould, Malcolm Gladwell and Joseph Stiglitz. That’s a lot of big ideas to simplify.

The whole episode is worth a listen. These notes are only about decision making. Ready?

…

Making good decisions. One thing Mauboussin referenced over and over was the reference class. “When thinking about any kind of forecast it’s incredibly important to understand the reference class from which this problem comes and to weight your own views with the evidence you have from the reference class.”

For example, data about 2017/2018 treasury notes and volatility measures are atypical. You wouldn’t expect these conditions to persist.

And when talking about Amazon, Mauboussin said that the growth rates some people expect have never occurred in a reference class of 313 examples.

Base rates and reference classes are so important to Mauboussin because good decisions come from good odds. “To me, a lot of investing decisions boil down to probabilities and outcomes and trying to be on the right side of expected values.”

Knowing what typically happens is a good starting place. It’s what Sam Hinkie and Daryl Morey used to get their General Manager jobs. When interviewing with the owners each presented what typically happens before teams win.

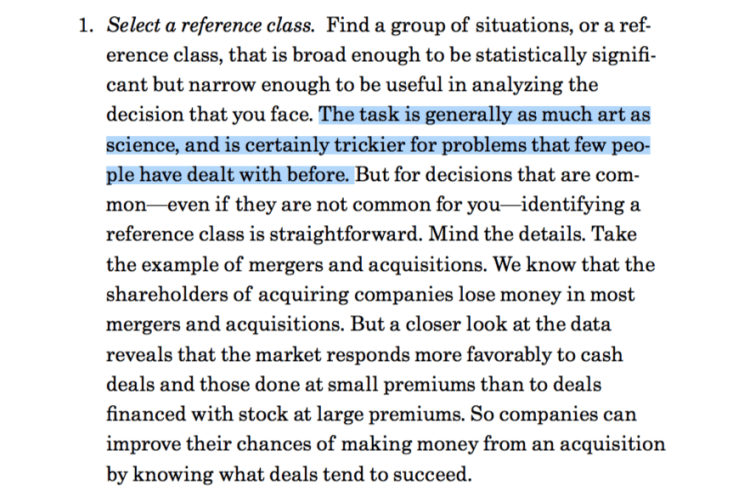

Choosing a reference class is an art and science. In Think Twice, Mauboussin wrote;

Reference classes are like Goldilocks, not too big and not too small. This is something Michael Lombardi and Bill Simmons have addressed regarding the NFL:

“Charlie Casserly was proclaiming he (Andrew Luck) was the next John Elway, they both went to Stanford but he’s not the next John Elway.” – Lombardi

“I don’t think you can compare anyone’s stats from this decade to last decade. No one gets hit anymore. The interceptions are way down. Even bad quarterbacks have good stats. I grew up with Steve Grogan and he would have years where he threw nine touchdowns and seventeen interceptions.” – Simmons

“Playing in a dome is a huge advantage.” – Lombardi

How relevant are colleges, eras, and domes for football players? That’s what you’d need to figure out.

If you can find a good reference class, compute a base rate, and then tweak your understanding based on your inside knowledge you’ve made a good start for good decisions. Now, we have to deal with biases.

“Heck, if you’re in the investment business,” said Mauboussin about the confirmation bias, “and you’ve never fallen for this one you’re not doing your job. We all do it.”

Richard Thaler warned Barry Ritholtz, “If you have a certain lens that you look at things through, then you’re gonna see everything to be consistent with your point of view.”

One way to get around this is, using Thaler’s words, more lenses. Mauboussin said this, noting that quirky backgrounds are a good diversity to have. Venture Capitalist Steve Vassallo said the same thing when he wrote that there should be a designer on the founding team to “project her weirdness onto the organization.”

Another bias is hindsight bias. Mauboussin said, “writing things down is really helpful. Be aware and say, ‘ I know that we had pros and cons for manager X but now he’s underperformed so let’s revisit the pros or vice versa.”

This is something The GMs advocated among other bias busting ideas. Biases are like bacteria. Good procedures (hand washing) can help but not eliminate.

Okay, let’s see where we are on our good decision making checklist.

- Find an accurate reference class.

- Calculate the base rate.

- Systemize how you’ll sterilize your biases.

Now we need to think about teams. A diversity of ideas is important because it allows you to Argue Well. Find, “people with different experiences and backgrounds and training and personalities that can surface different points of view.”

But you don’t want too many people. “Richard Hackman at Harvard studied teams across all different disciplines and found that the optimal size was four to six.” That’s about the right number of people for two pizzas, a Jeff Bezos heuristic.

These quirky groups will – hopefully – find new and interesting ideas. That is, they’ll come across Chesterton fences and debate the merits.

Sports are a good example knocking down Chesterton Fences. Mauboussin said that Go and Chess players are awed by AI moves. Our mental blinders, said Stanford professor Bill Burnett, block innovative solutions to Wicked problems.

“Another,” said Mauboussin, “is shifting in baseball. Baseball’s been played for a hundred and twenty-five years and all of a sudden people say, ‘we tend to know where guys hit the ball, we’re just going to put defenders in those spots.’”

Seides added that Big Data Baseball was “one of my favorite books…It’s what happens after you understand Moneyball.”

Mauboussin liked it too, “The thing that blew me away from that book was pitch framing…and simply bringing in a catcher who was good at pitch framing could lead to a substantial delta in games won.”

But it takes career capital to shift in baseball and keep your job. Mauboussin explained:

“I do think there’s an element of career risk, and this spans not just sports but also investment management. Bill Belichick goes for it on fourth down and it doesn’t work out and people give him the benefit of the doubt. But if you’re a coach who has a .500 team, it may be the correct decision but if you lose that game people don’t think about the quality of your decision-making process, they do think about the outcome, that’s a real big problem.”

Without career capital, people are incentivized to fail conventionally. I like how Tren Griffin addressed this:

“Bucking the crowd’s viewpoint in practice in the real world is not easy since the investor is fighting social proof. Robert Cialdini: “social proof is most powerful for those who feel unfamiliar or unsure in a specific situation and who, consequently, must look outside of themselves for evidence of how best to behave there.” I discussed social proof in a recent blog post on Cialdini’s book Influence. In many cases, following the crowd (social proof) makes sense. Sticking with the warmth of the crowd is a natural instinct for most people. Many people would rather fail conventionally than succeed unconventionally. But doing the reverse is easier said that done for most people.”

Seides added that Scott Malpass and David Swensen can do things that other people can’t. We heard how Jeff Luhnow approached this problem as he built the Astros into a World Series Champion. Luhnow said “I spend a large part of my job managing those stakeholders. It all comes down to communication.”

We’ve speculated – along with Ben Falk – that part of the reason Sam Hinkie was fired was that of poor communication. As Josh Brown cautioned, “If you’re just telling a client, ‘Shut up I got this,’ you’re not going to be the client’s advisor for a long period of time.”

Successful managers – of money, people, or teams – who blaze their own path must communicate with their stakeholders.

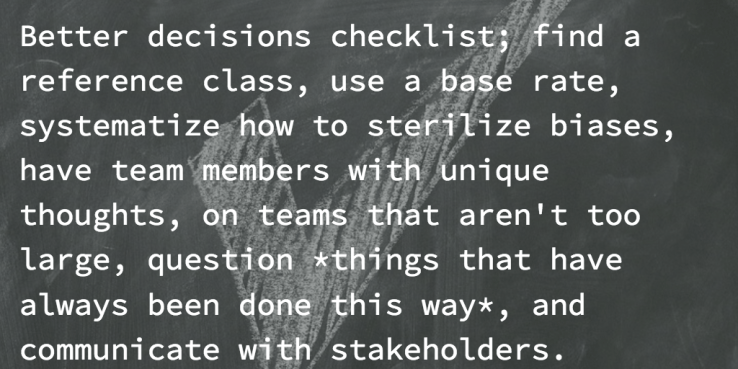

That’s about all it takes to make better decisions; find a reference class, use a base rate, systematize how to sterilize biases, have team members with unique thoughts, on teams that aren’t too large, question things that have always been done this way, and communicate with stakeholders.

Oh, and make sure you’re constantly learning. “Constant learning is such a big deal, In this industry, you can’t live without it… But recognize it’s not about shuffling papers, It’s about thinking.” This is something Guy Spier said too:

“What’s really important is that whatever you’re doing you’ve got to be thinking intelligently. When Todd Combs talked about his five hundred pages a day it stimulated a lot of people to go find five hundred pages a day to read but you gotta be intelligent about how you’re reading it.”

For Mauboussin, the ecosystem of constant learning is healthy when he’s healthy. That means eating, sleeping, and exercising. And “You can’t emphasize enough that hard work is really important. In the investment industry hard with isn’t necessarily spending sixteen hours at your desk, it is constantly thinking and reading and learning.”

What should you read? Here’s a start:

Steven Jay Gould’s Full House. Mauboussin’s The Success Equation. Brian Arthur papers. Books like Scorecasting, Scale, Adaptive Markets, or The End of Theory.

Thanks for reading this.

[…] Waiter’s Pad delves into Michael Mauboussin’s framework for better decision making. (link) Mr. Mauboussin and his team put out a Base Rate Book to help with decision making. […]

LikeLike

[…] the Eagles were undefeated when underdogs at home. However, this was a terrible reference class. As Michael Mauboussin has written, summarizing the work of Amos Tversky, good reference classes are “broad enough […]

LikeLike

[…] Michael Mauboussin is too: […]

LikeLike

[…] interest in value investors, Singh’s early venture capital investments demonstrated what Michael Mauboussin calls The Sucess […]

LikeLike

[…] Instead of just saying luck is hard to untangle from skill is there practical advice? Yes! Michael Mauboussin suggests we figure out how replicable something is. Rolling a seven with a pair of dice is pure […]

LikeLike

[…] one gets fired for IBM and not-buying IBM takes career capital. Michael Mauboussin explained it this […]

LikeLike

[…] agree with Michael Mauboussin‘s comments about luck; “There is no way to improve your luck because anything you can do to […]

LikeLike

[…] capitalists now confront Michael Mauboussin‘s Paradox of Skill. Michael Batnick simplified it as this, “Imagine a team of Lebron […]

LikeLike

[…] for his success, there’s no ‘go-for-a-walk’ equivalent for updating beliefs. Base rates suggest we stay closer to home until Mr. Minshew racks up some road […]

LikeLike