It’s 2004. Will Guidara is working at the Museum of Modern Art. Not in the esteemed gallery or adored restaurant. Will is in charge of the cafe: coffee, sandwiches, and snacks.

And he wants to create a gelato cart for the Sculpture Garden.

But first, he needs gelato worthy of the museum and his group, Union Square Hospitality. He finds Jon Snyder who sells it at a discount. He also convinces Synder to pay for the cart. It’s a nice cart.

Things are looking promising.

And then Guidara goes crazy.

He wants Italian spoons. “How amazing could a plastic spoon possibly be?” Will writes, “You’re going to have to trust me on this: they were paddle-shaped, extraordinarily well designed, and completely unique.”

But they’re expensive. His boss sees the cost and says “we’ll talk about this later.” But Guidara loves them. He gets them. He creates The 95/5 Rule.

“Manage 95% of your business down to the penny; spend the last 5 percent ‘foolishly’.”

This idea manifested later when Guidara was at Eleven Madison Park. While traditional wine flights had average wines, Will and his winos wander wider. Most of the samples were good, diverse, and less expensive. But one, the last one, was excellent. “The Rule of 95/5 gave us the ability to surprise and delight everyone that ordered those pairings, making it an experience they would never forget.”

It’s a good rule because averages are not good measures. Save where you can but splurge on one thing. That’s helpful. That gets past average thinking.

There’s a financial advisor axiom that the best plan is the one you’ll stick with. For trainers, it is exercises done through a full range of motion. The best endocrinologists find an achievable plan, not an ideal one. There should be one for education too. With that in mind, here’s a list of Russian resources optimized for consumption rather than comprehensiveness.

The Rest is History (podcast). Some podcasts are better than books because the host(s) add context. Dan Carlin is great at this. Tom and Dominic do too, and their series on Vladimir Putin is excellent.

Red Notice. A finance thriller? Yep. Bill Browder spent decades opening, running, and closing a fund in Russia during the switch from communism to oligarchy.

Exporting Raymond. We love Phil Rosenthal’s Netflix travel/food show Somebody Feed Phil. This is the story of taking the show Everybody Loves Raymond to Russia.

Koylma Tales via Agustin Lebron called it “a collection of stories of people who lived in the Gulag, possibly the most revealing book on human nature I’ve ever read.” Takes place through the 1930s and 40s.

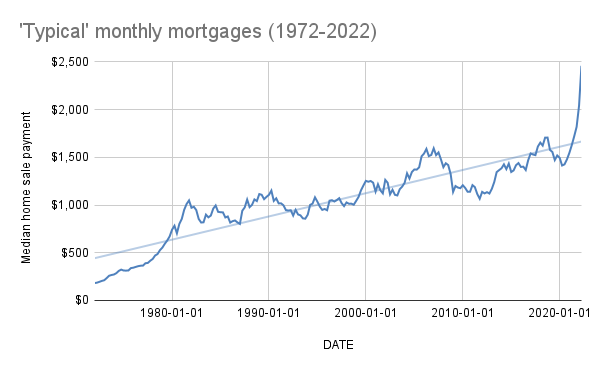

If my parents had bought when I was born they paid $982. But if they bought when my brother was born, it would be almost two-hundred dollars less each month. A huge difference for a young family.

The sweet spot for modern buyers was October 2011 when payments flirted with $1,000.

The Covid-19 drop and surge can be seen toward the right. It wasn’t until August of 2021 that payments crossed the trend line into wild heights.

What difference does it make for someone now? Since the end of 2020, the ‘typical’ payment increased seven-hundred dollars a month.

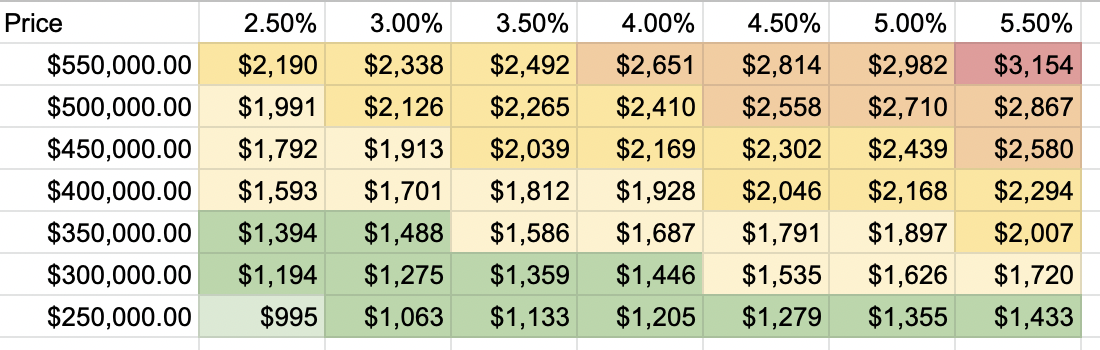

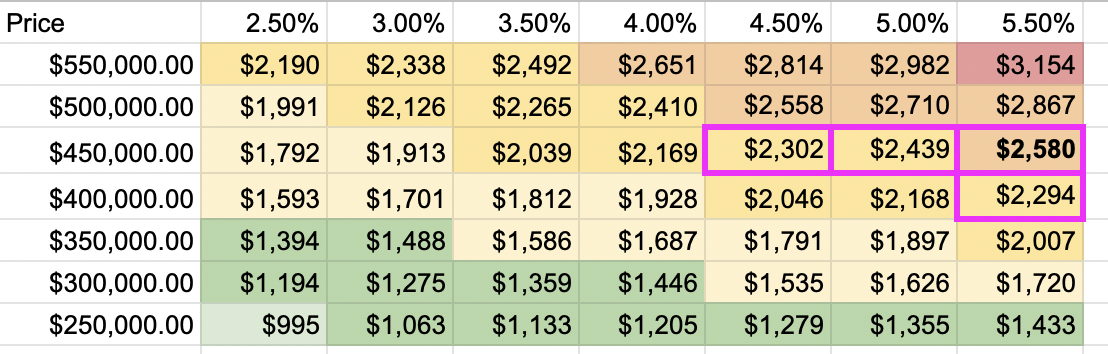

Interest rates are a headline metric, but are not the most important thing for buyers. The fall 2022 ‘typical’ monthly payment is: $2,580. A $50,000 decline on the purchase price is equivalent to 1% lower interest payments. Not only that, home prices have a .9 correlation with monthly payments whereas interest rates have a -.55 score.

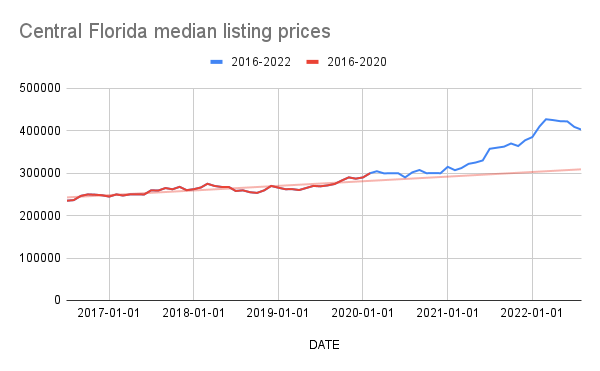

Housing is easy news to consume. The bad is about rising prices and rates. The good is about remodels, flips, and luxury. The truth is somewhere in the middle, here it’s in color.

How “off track” are housing prices? The red line is the 2016- March 2020 trend line relative to the graph of median listing prices. Currently prices are a 33% premium to what the historical growth suggests.

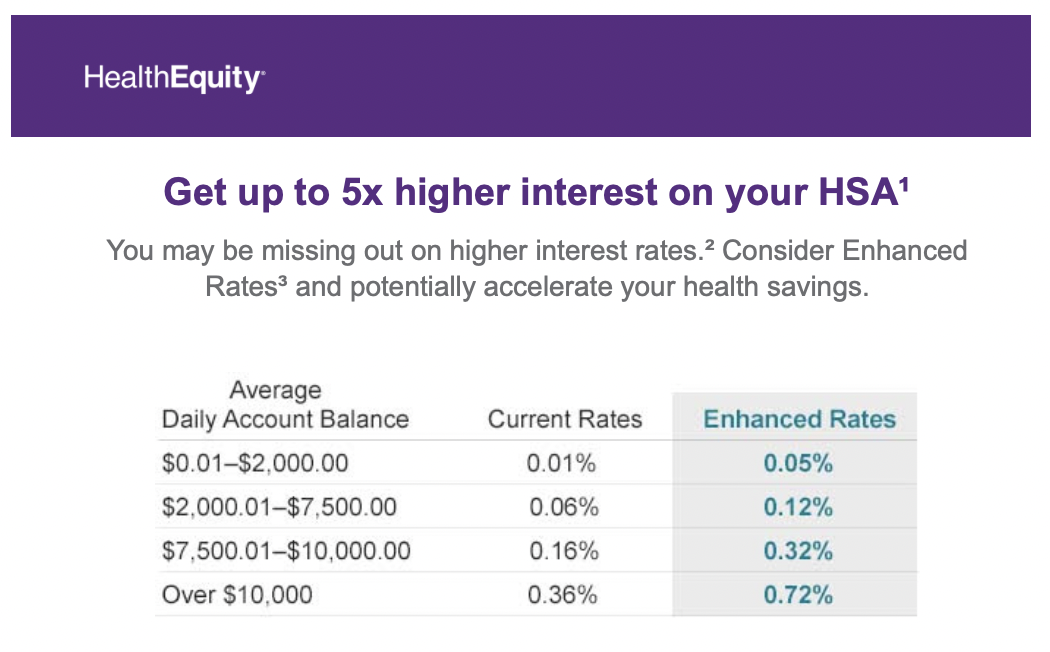

This is from our HSA. It’s good copywriting. ‘5X’ is easy to understand. ‘You may be missing out’ is great too.

The chart excels as well. It’s easy to understand and those Enhanced Rates do look bigger. They look bigger because of level one numeracy.

We level one think all the time. It’s knee jerk and first blush. We see something and some combination of evolution and experience fit what we see with what we know. Big red ‘Sale’ signs are examples. We first compare the sale price with the previous price rather than the item’s intrinsic value. This makes sense as our first reaction is immediate, requires no additional effort, and is something we are used to doing because it mostly works just fine.

The posts here, about average, focus on this idea too. Average is easy to compute and conveys certainty about an uncertain (often heterogeneous) world. Average is level one numeracy but we can do better.

A fast fix comes from Sir David Spiegelhalter. Don’t look at relative comparisons, look at absolutes. Rather than the relative rate, look at the dollar difference.

That’s what I did.

If someone saves the $2,000 in an ‘enhanced’ HSA account they have sixteen more dollars after twenty years. A lot of years for not a lot of money. For accounts of ten-thousand dollars, the difference is almost eight hundred dollars ($11,543 vs $10,745). Fine, a Series I Savings Bond accrued that same dollar value in six months.

The don’t look at relative comparisons, look at absolutes is a good starting place – but there are further levels.

First is to think about the costs. The enhanced HSA rates are an annuity, likely with some new terms. There’s the switching costs too. That’s a potential headache and unwanted contract in exchange for not much money. We will pass.

Actual health rather than health savings is different.

For people 25-34, their chance of dying from Covid-19 is about the same as pulling the ace of spades from a shuffled deck – twice in a row.

For people 55-64, their chance of dying from Covid-19 is about the same as flipping heads eight times in a row.

For people 75-84, their chance of dying from Covid-19 is about the same as pulling any heart from a random deck of cards – three times in a row.

Those are low absolute risks but seriously consequential.

The world is complicated and messy. Not only that, but it changes too. Numbers are helpful, but we have to ask the right questions to start.

–

The Covid-19 odds are rough estimates. There are about forty million people in any ten year age group. The number of deaths in the 25-34 group is 11,451. I divided the deaths by size of the group to get the percent chance of death. Odds are multiplicative, three heads in a row are 12.5%, 0.5*0.5*05. Two ace of spaces are one in fifty-two times one in fifty two, or about 0.04%.

In his podcast with Jocko Willink, Joe Piersante talks about his time working in Arizona and dealing with hundreds of meth labs. If I told you I was in 500 labs, Joe says, it would be an understatement. Meth was the drug of choice in Joe’s region and between the cost to create, the large rural area, and proximity with Mexico it was difficult to police.

“It was bad at first because there was so many,” Joe says. It was too easy. What “put a dent into it,” was the 2005 Combat Methamphetamine Epidemic Act, which restricted access to pseudoephedrine, a precursor chemical to meth.

The COGS increase changed the business model.

…

Later in his career and the episode Joe talks about his time in Afghanistan. “We would not go after the poppy farmers because they were made to grow the opium,” Joe said, “The Taliban came in and they had the biggest stick at the time. It was a case of ‘you’re going to grow this or you’re going to get killed.'”

There were no better incentives to offer this group of laborers. “We knew they weren’t reaping the benefits so we tried to find the people getting the money.”

…

A lotta problems are multi-dimensional. Think about the field of addiction, said David Nutt, it’s about the drug, the person, and the society. Each of those is a lever. Profession problem solving is too. How would an economist solve this? How would a marketer? How would a coder? Each leads to a different island in the archipelago of thought. DEA agents think a bit like business owners, and we can add this approach to the set.

When a low probability event occurs (say an underdog wins a sports championship), we tend to come up with reasons why we might have expected it. This phenomenon is often referred to as hindsight bias, a tendency to perceive past events as having been more predictable than they actually were. But if we consider that many events occur in a year, we should expect at least some to be low-probability events. For example, there are many championships in a given year, so we should not be surprised that every year there is a championship outcome in some sport (say tennis, golf, football, etc.) that no one expected.Dan Levy, Maxims for Thinking

Something is always happening because with enough parts, something happens. The odds that one low-probability event, a 100:1 long shot wins an event, occurs is low. But the odds that any low probability event occurs is fair. Tonight many people will go to many bars. To bet that Your Friend will meet their spouse is ridiculous. To bet that Anyone’s Friend will meet their spouse is a no-brainer.

The bar points out the mechanism we use everyday: a filter. Not everyone at the bar will be there to meet a spouse and those that are there for that will very likely leave without doing so, but being at-the-bar is the filtering mechanism. It’s the same mechanism the Nigerian Prince uses.

It’s well noted that scamming emails contain misspellings, outlandish claims, and hard-to-swallow facts as a filter. A scammer, like a dater, only wants to draw from an eligible pool. And the scammer and the dater both have the same reason: resources. A scam email has minimal costs. A visit to the bar has minimal costs. These filters have to exist because the follow up is expensive.

Something is always happening, but we often don’t want ‘something’. We want ‘this thing’. One tool is to increase the probability (p) it occurs. Go to the coffee bar. Send the email with mistakes. Another tool is to increase the number (N). Will Michigan ever lose again as a thirty-point favorite? Maybe. Will a division one football team lose as a thirty point favorite? Probably. Will any football team lose as a thirty point favorite? Definitely.

Low probability events will always occur and the mechanism of a large Number or rising probability influence how often. Maxim 5 is “the world is much more uncertain than you think.” Levy, writing about Richard Zeckhauser notes, “so the next time you find yourself thinking that some event will happen for sure or that some other event has no chance of happening, pause to remind yourself of this maxim.”

–

Thanks to Eric Bradlow on the Wharton Moneyball podcast for articulating the idea “large N small p”.