Supported by Greenhaven Road Capital, finding value off the beaten path.

Chris Douvos spoke with Patrick O’Shaughnessy, Ted Seides, and gave a pair of presentations at Stanford (2016 & 2017) that we will use for these notes on venture capital investing.

Douvos’s investing career began with some choice teachers; David Swensen at Yale, experience at Princeton, David Salem at TIFF. Douvos learned to be a BLT investor – beyond the long-term. Swensen told him:

“Investing is about optimizing discomfort. If you’re feeling too comfortable you’re not taking enough risk. Risk is not itself a dirty word. There are two kinds of risk, there are risks you can mitigate and there are risks that you can’t. The ones you can mitigate you want to spend all your time mitigating and diversifying them and the risks you can’t mitigate you want to make sure you get compensated adequately for.”

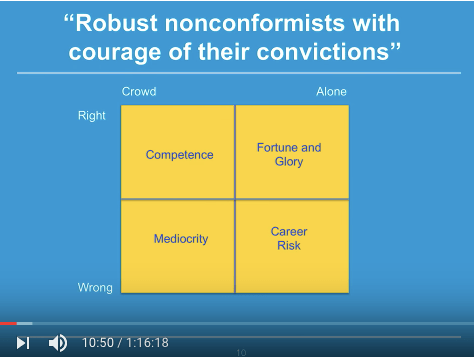

From David Salem he learned to invest heroically, as a robust nonconformist with courage in his convictions. Douvos presents it this way:

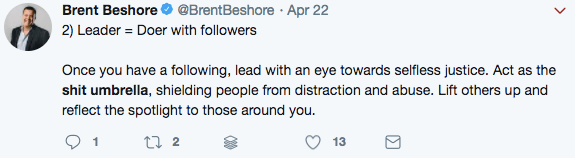

Howard Marks has a similar matrix that inspired Andy Rachleff to start Wealthfront. David Salem explained to O’Shaughnessy in their podcast that to be right and alone you need degrees of freedom. Or as Brent Beshore puts it, you need a shit umbrella above your head.

Besides support from the top, Douvos warned Patrick that investors shouldn’t choose venture if they have the wrong timeline. “The biggest drive of venture success is a willingness to have a long horizon.”

High tolerance for risk, illiquidity, and a distant horizon, Douvos said, “is a rare trio.” Yale is the canonical example. “But Yale has a comfort envelop dynamic. They have an accommodative committee that will stick with them through thick and thin. They have a time horizon that is much longer than most folks.” This was a point Salem made too; someone can’t imitate the Yale strategy without imitating the Yale people and processes too.

But imitating Yale is comforting. Those folks are doing it. Being different takes career risk. Jeremy Grantham told Douvos, “Over ninety percent of decisions as an asset manager first take into account the career risk associated with those decisions.”

No one gets fired for IBM and not-buying IBM takes career capital. Michael Mauboussin explained it this way:

“I do think there’s an element of career risk, and this spans not just sports but also investment management. Bill Belichick goes for it on fourth down and it doesn’t work out and people give him the benefit of the doubt. But if you’re a coach who has a .500 team, it may be the correct decision but if you lose that game people don’t think about the quality of your decision-making process, they do think about the outcome, that’s a real big problem.”

Rory Sutherland said that this comes from our willingness to signal competence.

“If I pretend everything is logical, it may not be a really good decision but if things go wrong no one can blame me. This is an extraordinary form of corporate insurance.”

“The Venn Diagram of the people who can do and have the courage to do it is,” said Douvos, “that interaction is actually pretty small.”

…

The Venture Captial Model. According to Douvos, there’s no great model. As he says in a presentation at Stanford; “you don’t have winners repeating.” But, he tells O’Shaughnessy, it’s not as extreme as monkey’s throwing darts. That said, factors may not be the best approach. “If you found four factors, I’m not sure they would correlate with success, but they would certainly correlate with volatility.”

His best guess for a venture capital model with quantifiable inputs would be; concentration, scientific processes, early-ness, and size discipline. Like he says, it’s not easy.

One thing he wouldn’t include is performance. “I actually think track record is a lagging indicator, not a leading indicator.” Part of the reason is the time it takes for venture investments. The average investment, Douvos explains, lasts longer than the average marriage. Also, size isn’t a perfect indicator. “Someone once told me, it’s harder than you ever dreamed it would be to raise fund one, but far easier than you ever thought it would be to raise fund two.” O’Shaughnessy adds, “I call this assets vs alpha.”

Venture capital hasn’t always been so difficult and messy. Douvos admits in talks that he does a kind of “voodoo.” But it wasn’t always voodoo. No, this problem began with David Swensen.

“After Swensen placed all his chess pieces on the board he wrote a book and when I pitched non-profits I would sit down and say, ‘Now a reading from the book of David.'” That book, Pioneering Portfolio Management, became an investment tome. Swensen wrote for so much of an allocation in venture capital and groups invested so much in venture capital.

Money flowed west and the landscape bloomed. “All these things led to a flowering of entrepreneurship.” But opportunity withered. Douvos is electrified in his chats and likes to quote Buffett; Opportunity = Value – Perception, though he’s not sure Buffett ever said such a thing.

“A thousand flowers are blooming and the vast majority of those will die off but the few that survive with thrive and be transformative.”

And that’s the stage venture capital is today. The innovators were followed by the imitators who are followed by the idiots – and “sometimes I feel like we’re in the idiot phase.” Things are feverish. “I think a lot of people in this zip code think about sexiness as a proxy for an opportunity but it’s the exact opposite.”

Douvos recalled his time as a “Henry McCance barnacle.” Following McCance around he recalled, “He told me, ‘When an asset class works well, capital is expensive and time is cheap. What we saw in the bubble was that capital got cheap and time got expensive.'”

Today, Douvos repackages a Gatsby line for the Valley.

“The tempo of the city had changed sharply. The uncertainties of 1920 were drowned in a steady golden roar and many of our friends had grown wealthy. But the restlessness of Palo Alto in the 2000’s approaches hysteria. The parties were bigger. The shows were broader. The buildings were taller. The morals were looser.”

Perception isn’t value. Indexing isn’t value either. “If you were to index venture you would waste your time.” Venture capital returns are like average income when Bill Gates is in your sample. “Skewness can drive sadness,” said Douvos when he presented that the mean return for a vintage of funds was 45% higher than the median return.

This doesn’t mean good ideas, good companies, and good people aren’t out there. They are. The world is getting better. But investors have to work harder to find them.

Douvos is perplexed when he reads articles about another app. Come hang out at his portfolio companies “and you’ll see smart, domain focused people doing amazing world-changing stuff.”

Douvos looks on college campuses. “If I could make a pairs trade I would go long Berkeley and short Stanford.” That’s nothing against Stanford, where Douvos has given presentations, but more for Berkely. It’s a Moneyball approach, find value where others aren’t looking.

Douvos models himself after Herodotus. After an early visit to California he reflected, “I thought I needed to be in the land of the start-up-ians.” Walt Wittman’s Song of the Redwood Trees also inspired Douvos. “Populous cities—the latest inventions—the steamers on the rivers—the railroads—with many a thrifty farm, with machinery,”

West, young man, go west.

He knew from his days at TIFF and Princeton that running up and down Sand Hill Road, “You just get his warmed over conventional wisdom and sometimes a healthy dose of politics on the side…Historians prize primary sources and the primary sources were the entrepreneurs.” So he moved west and starting showing up at companies with a case of beer on a Friday afternoon. “People are thrilled to talk about what they’re up to.”

“I asked Mike Maples, ‘How is your success so repeatable?’ and he said, ‘I’m looking to meet with ten people a week that are really smart that no one else is meeting with.”

“I set a rule for myself to be like Herodotus. For every hour I sit with a VC I’m going to sit with an entrepreneur.”

“Creativity doesn’t come from within the community of consensus.”

Though different in words, the spirit is the same as How Brian Koppelman made Billions. If you have genuine interest people will talk.

But not necessarily believe. Douvos told a group of students, “(To do this job) you have to be a professional skeptic, everyone is a fantastic salesman. You can sit there all day and get pitches from people and every opportunity is as exciting as the last.” He wears many hats; investigative journalist, counselor, teacher.

Douvos raises money then gives it away, then (hopefully) gets more back. The model works, for now.

Patrick O’Shaughnessy asks if he’s worried about Initial Coin Offerings but Douvos isn’t perturbed. “You created a more effective vehicle in a sense – but you still need help. So much has to go right in building a company that you want more people in your squad than you ever dreamed possible.” He points to a 2014 blog post that Josh Kopelman titled Domino Rally Business Models. In that post, Kopelman notes that you need a lot of things to go right for a business to succeed. Douvos said, “taking a company from 10M to 100M in revenue is an amazing challenge…It’s like riding a tiger whose fur is on fire running through an oil field.”

Help comes as doing something, making connections, offering insight. “One of my views is that active management will look like catalytic management.”

…

Douvos, again and again, lays out what he looks for. He’s teaching not obstructing, he wants to educate not confusticate. His process?

1/ The people. Do they have an edge somewhere? They must be “people who are reflective, opinionated, and have humility.”

“Every great partnership is a well-rounded whole of jagged pieces that fit together nicely.”

2/ The strategy. “Is there a resonance between the strategy and the people?” It’s like Christensen’s Disruption Theory, only instead of the firm, it’s applied to the individual.

“It’s amazing how often I meet middle managers from Proctor and Gamble who all of a sudden want to run a micro-cap buyout firm. They say they can bring operational experience but, no, you had a staff of thirty people for all these years in Cincinnati. What do you know about being in the weeds and deploying all these other plays in the playbook?”

3/ The portfolio. “These are fragile.” How does someone diversify the risk when “Bob the VP of sales sleeps with Jane the wife of Bill the VP of engineering.”?

Then we get into PE math “I tell entrepreneurs, once you take venture capital the venture capitalist’s business model is your business model.” Douvos wrote:

“Here’s where it gets dicey for the masses, though (and I’ll make some gross simplifying assumptions): if you’re an LP and investing in an run-of-the-mill $500 million fund hoping to get a 3x net return, that fund has to generate $1.75 billion in returns ($1.25B in profit less 20% carry equals two turns of profit). Of course, that’s just the capital that accrues to the firm’s ownership stake. Since a lot of firms end up owning only 10-15% of their companies at exit, you’ve typically got to gross the $1.75 billion up by a factor of between 6.67 and 10. That suggests that those firms need to create between $12 and $17 billion of market cap just to get a 3x fund-level net return to their LPs. Caliente!”

4/ The performance. It takes seven years and by the time you see results, it’s like looking through a telescope at life in the past. “The challenge is that performance is easy to measure,” but it may not be the right metric.

“People focus on a few metrics because they are easy to extrapolate but if you’re doing this job well it’s crazy time intensive.” It’s getting a beer with people, it’s walking tours, it’s visiting. It’s “building the mosaic and that takes time. It’s why people take shortcuts and that’s why you default to brand.”

So what makes Douvos work?

When asked about his day, Douvos explained his average week; meeting with a manager about their portfolio with mental notes about cross-references to check, meeting with investors, a Palo Alto walking tour and history of the electronics industry, meeting with entrepreneur, “hopefully I’ll have a neuron fire from a conversation from a few days earlier.”

After that, he’ll drive to a robotics or AI lab and talk with the teams there.

Douvos got to this point by standing out. He visited campuses before others. He started blogging before others. He wore a red t-shirt before others, actually, the t-shirt is a good story. He realized, “ I can educate people.” When you’re the first voice, you get to choose the conversation.

…

“Venture Capital,” Douvos said, “has more units of ego per dollar of return than any other asset class.” But Douvos tries to build partnerships and community. He tries to manifest what Mr. McCance at Greylock told him. “If we ever have to go into the bottom drawer to pull out our documents we lost. We should have a partnership with a capital ‘P’ where we do right by you and you do right by us.”

Thanks for reading.

[…] “When there’s a deal that’s fair for everyone, just do it.” Chris Douvos was encouraged to be a Partner, to be fair, and never have to go into the bottom drawer to pull out […]

LikeLike

[…] are tricky, performance figures are easy. But as Chris Douvos noted, performance is often a lagging indicator. It sounds like Chanos agrees, “What most […]

LikeLike

[…] require patient capital but restless capital can walk away. Chris Douvos noted about long-term investing, that “The Venn Diagram of the people who can do it and have […]

LikeLike

[…] people out there telling us now nice it is. Investors and investigators sniff through the hot air. Chris Douvos said that to be an investor, “you have to be a professional skeptic, everyone is a fantastic […]

LikeLike

[…] Chris Douvos got this advice, “But David Salem said to me, ‘I want you to be unafraid of being wrong and alone because if you’re unafraid of being wrong and alone every now and then you’re going to be right and alone and that’s the box where fortune and glory reside.'” […]

LikeLike