“So we’re all forced to make stuff up, whether it’s being a scientist or being a doctor or being an Olympic athlete or climbing Mount Everest. And people really vary in their need for friction. And some people need a lot more than others.

And if they don’t have it, they’re really, really unhappy. And I do think that a lot of the people that I see with addiction and other forms of mental illness are people who need more friction.”

I (finally) bought Thinking in Systems: A Primer in June 2025. It was an early summer read and focused a lot of summer thinking (before back to school gears up) on systems thinking.

But maybe it plays a more central role in the system.

Maybe friction is akin to vanilla in baked goods: Gotta have it, but just the right amount.

A fellow teacher told me she’s ready for her students. Summer break (we get seven weeks) is too long. We had a similar feeling. One night everyone at cereal the kitchen was a mess. This is what degenerates look like, I explained. The current patterns of summer don’t have enough frictions. It’s what people crave with schedules. It’s why people run races. Competition is friction. Constraints are frictions.

We’ll end in the spirit of Tyler Cowen: Friction is underrated.

“But today I think about it as my mission in life is to get as many people as possible into positive feedback loops,” Graham Duncan told Tim Ferriss.

It’s why he spends so much time interviewing, talking with, and hanging out with people. “So I like getting the design right up front…I don’t wanna put something into somebody. I wanna have them do the thing that they wanna do anyway.”

Or as someone else said recently: don’tbe trying to run up a down escalator.

One joy of YouTube is the rabbit hole. Find a niche and let the algorithm pump your feed full of whatever randomness.

One of my trips was the Toyota Sienna. One reviewer noted: it just doesn’t fight you. It’s not the top categorically – but there are no weaknesses. It’s a “floor-raiser”.

Positive feedback loops. Running up a down escalator. It just doesn’t fight you.

Alignment matters. It doesn’t make the knots less tangled but it makes untying them a lot easier.

There’s something mentally stabilizing, even encouraging, to know what’s going to happen.

Not precisely. Not like a crystal ball. Just generally, like a heads up.

At a parent meeting, my daughter’s volleyball coach said, the season is long and the work is hard, at some point your kid will want to quit, don’t let them.

That was good. It prepared the parents.

We don’t always get this information

Sometimes we get the “Instagram” life. That’s unhelpful.

…

In 1987, Ben & Jerry’s had their best summer ever: a year-over-year sales increase of 60% to 32 million dollars.

Financially things were good.

Functionally things were a mess.

At their brand-new plant, the freezer doors didn’t have “tolerance”. The sliding doors were only just large enough for a forklift to perfectly pass through. Sometimes it didn’t. The result was that after enough banging on the freezer frame, the staff left the doors open and relied on the plastic strips to insulate the ice cream as best it could.

“The term freezer door,” wrote CEO Fred Lager, “became a metaphor within the company for anything that wasn’t working and was being ignored despite a painfully obvious need for attention.”

Human resources, processes, and candy chutes were all freezer doors.

They had to address these growing pains.

At an all-hands meeting after the busy summer season wound down, Ben Cohen gathered everyone and gave a state of the company. To address the freezer doors he asked everyone to form groups and create a list.

There were a lot of complaints, but Ben took them all in stride. “It’s only an indictment of management if you think that a well-managed organization doesn’t have problems,” Fred recalled Ben’s comments, “This was just telling us what we had to work on and letting the employees know that we knew about it.”

It was a heads-up.

…

These wrap-ups that lead to heads-ups are post-mortem reviews. At the Rewired Group, they are a mandatory part of the process. But they don’t just successfully happen.

Our egos can get in the way. Post-mortems are NOT to assign blame. Howard Marks called this book, “a very interesting book on self-justification” – aka somebody f’d up and it wasn’t me.

What works better is a culture of extreme ownership. This starts at the top. Ben Cohen wasn’t a perfect leader. No one is. In Lager’s book, he comes off as demanding and not fully aligned with the rest of the ice cream crew. But what he does do is avoid the ego trappings of the top position.

“Eighty-five percent of all problems,” wrote Deming, “are system problems not people problems.”

Be wary of the ego. Address the system. Fix the freezer door.

Ethics aside, there are no bad businesses – only the wrong business model. Successful organizations have the right people interacting in the right way given the conditions. Outcomes are a mix of who and how with a sprinkling (or deluge) of randomness.

One ‘condition’ is the relationships with customers. Amazon sellers interact through Amazon, and whatever information the everything store deems important is what the who needs to figure out how to do. As a result those stores compete on price and stars.

Another ‘condition’ is fickle investors. Money managers prefer clients who aren’t depositing and withdrawing money constantly. So they write letters, go on podcasts, and pitch what they do in an effort to get the right clients. Organizations with a low CAC have figured out the current how.

A ‘how’ we’ve advocated is to always fix your weaknesses. Eric Eager explains an NFL example.

“The Chiefs just got done with negotiations with Orlando Brown, who wanted to be the highest paid left tackle in football. The Chiefs balked, and it’s a great decision. If you pay for a guy to go from an 85% win rate to a 95% win rate, that doesn’t matter nearly as much as taking your weakest guy from an 80% win rate to 87%.”

For NFL offensive lines the conditions are such to fix your weaknesses.

A lot of times we look at the who and the how. It’s the nouns and verbs that are most salient. ‘Hire a new salesperson to make more calls.’ Instead should we start with the system conditions?

Average measurements are overrated because they are easy to compute, give a number which implies certainty, and convey ideas about as well as a bunny ears black and white television.

Fixing weaknesses is a good default option. But so is asking about the system. It’s a non-obvious and valuable way to figure out how the who can do their best work. And maybe that means fixing weaknesses.

And I probably ruined your parents’ life And your childhood too ‘Cause if I’m the music that y’all grew up on I’m responsible for you retarded fools I’m the super villain Dad and Mom was losin’ their marbles to You marvel that? Eddie Brock is you And I’m the suit, so call me—

Eminem, 2021, Venom

In complex systems you can’t do one thing. When he was chief economist of Uber, John List and his team ran an experiment to see how tips affected drivers. They rolled out the option to tip in four cities and collected the data. Tips, List wrote, work. When drivers earned more they drove more. But you can’t do just one thing. When tipping expanded to other markets other drivers drove more too. With the increase supply of drivers but the same demand, total earnings with tips were about the same as before. But the drivers ended up working more. It was more per ride but fewer rides.

As a teen I remember big concerns about what music teens listened to. In 1990 the parental advisory label started to appear on CDs. In 1997 Eminem release The Slim Shady LP. That music was for my car only, not the house. Eminem gets this. “I’m the super villain Dad and Mom was losin’ their marbles to”. It was NOT GOOD that we were listening to this.

Maybe?

List’s Uber experiment explains an externality. Do one thing and this other thing happens too. Eminem’s other thing is health. Venom is my favorite workout song and Eminem is the 13th most popular artist on Spotify with fifty-three million plays. A month! That’s 100k hours a day. If one-fourth of those hours are someone exercising, that’s 14,000 pounds lost each month.

…

Behavior change starts with easily understood stories. Tell someone a story they agree with, or understand, or can tell to others (which raises their status). Eminem’s explicit lyrics are something to warn against. But telling a positive story through some Fermi thinking sounds good too.

It was October 2000 or thereabouts and Jacob Lund Fisker wanted to know if someone could live a sustainable and rich life.

“I did a little back of the envelope math. We physicist restrict ourselves to post it notes typically. I took the global GDP, divided it by the global population, and took our ecological footprint number and divided by it as well. If everyone did what I was setting out to do, the maximum each person could spend was six thousand dollars per person per year.” – Jacob Lund Fisker, Through Conversations, November 2021

There’s a few things going on with FIRE. One is attention grabbing, everyone has a means to share their story and the atypical gets attention. Another is the financial conditions, it’s easier (though not easy) than ever to make a large amount of money, in a short amount of time, and invest in a mostly up market. The last and staying part of FIRE is the intentionality. It is impossible to FIRE without prioritizing one’s life.

Fisker’s philosophy is my favorite because he’s a system thinker. Early Retirement Extreme is a book that starts with systems and ends with personal finance. Saving half of one’s income is the act but you can’t do just one thing.

We’ve looked at spreadsheets for emergency funds, 401Ks, and how many touchdowns a quarterback will throw. Spreadsheets offer precision with numbers but don’t address our systems. Basic math is fine if the system is great but it doesn’t matter how great the math if the system is shit.

There are (at least!) two ways to consider the flower. One is that the flower is the sum of its parts: bud, leaf, pistil etc. Each part does a job, which sustains the flower. Sunlight, rain, earth are all inputs to the production of “flower”.

Another way is that the sun, the rain, and the earth are part of the flower too. Sunlight then is as much part of the flower as the bud.

“Someone who read an advanced copy of the book said it had a real Buddhist flavor. That delighted me. What comes through is this idea that we are not bounded, fixed, sealed-off, separate individuals. We are part of a whole ecology. We separate our brain not only from the world around us, but also from our own bodies, and that’s a mistake.” – Annie Murphy Paul, June 2021

Thinking in systems helps explain the world. For example, movie economics changed as the entire system changed: nationwide advertising led to event movies, DVD economics led to more movies, international markets led to franchises. Framed this way, was Hollywood separate like the flower? Or, was it the second, where social, governmental, and economic trends were part of the system?

Annie thinks this second view, the sun is the flower too, explains the world better. One contrast she notes is between a computer and a person. The computer works the same regardless of the place, a person does not. This is the reason we get good ideas on a walk – we think different. “The history of innovation,” wrote Stephen Johnson, “is replete with stories of good ideas that occurred to people while they were out on a stroll.”

– The Extended Mind is Paul’s book though she has many good podcast interviews. A book full of walking, and other, inspiration is Daily Habits.

Mike Maples Jr. worked for a software company that enabled telecom companies to offer broadband service. Mike’s job was sales.For many telcos it wasn’t even a buy or build? question because they were in the hardware business: driving tucks, laying cable, and climbing telephone poles.

But not every company was a potential client. “I started” each pitch, Maples said, “by saying, ‘This many not be a good use of your time.'”

“I would start to make body language like I was going to leave because my goal was to have them reach out, pull me back, and go, ‘No, I’m screwed I’ve got to have three million subscribers in the next eighteen months, my CEO just committed to that on their last Wall Street call.” – Mike Maples Jr., Founder’s Field Guide August 2021

It wasn’t just customers Maples wanted, but the right customers. In high-cadence systems, the wrong customers slow a business’s innovation cycle. “They’re going to ask me for requirements that don’t matter for building a different future” Maples said, “because they’re conventional thinkers who live in the present.”

Traditionally we think of CAC as customers per dollar spent, but customers are heterogeneous, that’s a two-dollar word we learned during Covid. Maples is a venture capitalist so he wants to invest in things that are small now but will be huge later. In the current circumstances that means technology. So Maples restricted his customers because the product he sold (or, wanted to sell in the future) was very specific.

The opposite case can work too: expanding a customer base by offering a more generic product. This is the American Picker case. People browsed the antiques but bought the t-shirts.

A business model is not static. It’s more like a philosophy combined with a Bayesian formula. It has to change with the conditions, but that starts with an awareness of one’s system.

–

Systems and CAC are two of my favorite ideas. Read them all in a daily email drip on Gumroad. Find it on Amazon too.

The top five S&P companies account for 22% of the index’s earnings and a similar percent of the market cap.

“To me that is an interesting market question right now. If you were a betting man would you take the other 495? Would you take the field or would you take the Lakers with LeBron, a healthy Anthony Davis, James Harden and Kevin Durant on the team too?” – Carl Kawaja, Invest Like the Best, July 2021

One way to improve decision making is to understand the mechanics of a system. The physics system for example is relatively stable and that’s why, with great work, engineers can land the Perseverance rover in a Martian area twice as wide and one-third as long as Manhattan. Other systems, like social systems, follow the rules of network effects like the friendship paradox.

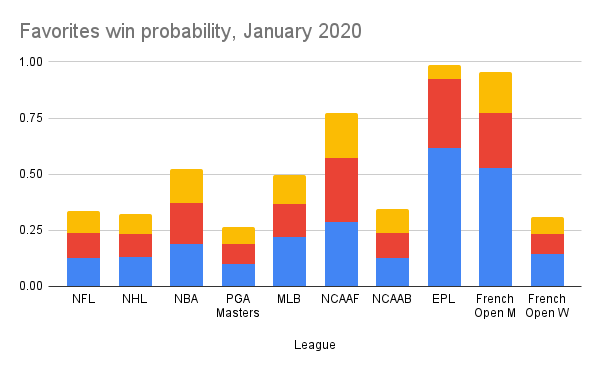

Sometimes analogies help to understand the type of system. One sporting analogy is to take the favorites or the field. When Kawaja’s episode was released, the Chiefs and Bucs had a cumulative 33% chance to win the NFL big game. Sports vary though. In January 2020, three NFL favorites had cumulative odds of about 30%. Meanwhile the top three NCAAF football favorites had odds of about 75%. Three tennis players at the French Open get a bettor to better than ninety-five percent. Want to bet the PGA Master favorites? The top seven golfers only get you better than a coin flip.

One reason to take the field is that more can go wrong than go right. Something is always happening and it’s more likely to be a “negative tail” event than a positive one. During the 2020-21 NFL season we guessed that Tom Brady would not hit the over on passing yards (he did) by guessing that injury, Covid, and new teammates had a much larger downside area. Kawaja recognizes this too, noting “guys get injured”.

It’s not that the field or the favorite is better, but which is cheaper relative to the expected returns. During the Big Game for instance, things happening (safety, two-point conversation, etc.) are priced higher because people like to bet more on something happening. Successful betting and investing isn’t about finding the best, but finding the best odds. Yes, the Chiefs and Apple are great teams but is there value in the high prices?

–

Physics systems or social systems are wonderfully illuminated in Nassim Taleb’s book Antifragile.

Michael Covel (@Covel) joined Barry Ritholtz (@Ritholtz) to talk about trading, trending, and Thailand. Okay, not just Thailand,but it starts with ‘T’ and I’m a simple writer.

Covel – and Ritholtz – fall into the category of “good talkers” and I listen to at least part of all of their podcasts. Get them together and you get two solid hours of conversation.

This podcast wasn’t as into the weeds I know about but provided lots of superficial anecdotes about things I don’t know like the experiences of working in Japan, what it was like to see economic ideas change, and how capital is like Gap t-shirts.

One final personal note, Covel challenges my ideas on his podcast. Whether it’s something I don’t understand or something I’m not interested in – but I try to listen anyway. One of the ways to use Twitter for good is to bust your biases. That’s something true for podcasts as well.

Ready?

Greats are made, not born.

Covel was influenenced by Richard Dennis(wiki) and the Turtle traders. The story goes, and Covel says he has no reason to doubt this, that Dennis and fellow trader William Eckhardt saw Trading Spaces (Eddie Murphy). Eckhardt said that could never happen. Dennis said it could, and he’d prove it. A bet was made.

Dennis recruited a group of – mostly average – applicants how to trade on a trend-following strategy that he created. This group of ‘Turtles’ turned out to be widely successful.

The application is true with regards to the podcast itself. Covel made himself into a great trader, writer, and podcaster. Ritholtz admits this too, that radio didn’t come naturally to him and that there was a learning curve. He’s gotten pretty good at it.

This is true for so many people, especially comedians.

Comedians are – sometimes sadly – not very good at anything. A lot of the art from people like Phil Rosenthal or Judd Apatow comes from places of pain or darkness.

In his interview with Rithotz, Ken Fisher noted that even though his dad was a great writer, he wasn’t.

Ritholtz compliments Fisher’s work and says, “you’ve obviously inherited your dad’s writing skills.”

“Not true,” replies Fisher, “because if I had inherited them they would have come to me very naturally, but I worked hard to learn how to write.”

Except in rare, physical domains like sports, you can be good (or great) with some work.

Jack Canfield cautioned Tim Ferriss about pegging “being great” on only one thing. He tells the story of a family friend who wanted to be in the NBA. Of course, the guy wasn’t good enough to play professional basketball, so he took another route. He worked to get in the front office. He’s in the NBA, just in a different form than he first imagined.

It’s trend-following, not trend predicting.

As a simpleton (n00b), I didn’t really know what “trend-following” was. Covel set me straight when he said:

“If you’re a trend following trader you don’t have a mindset or prediction where any particular market is going to go. So when it starts to move, you’re just following the crowd.”

Later in the interview he adds, “nothing can be predicted.”

I was thankful to hear this because predication is hard. Like, really, really, really hard. It seems to me that Covel (trend-following) champions non-prediction. This is paramount for complex systems (trading, ecosystems, a college classroom). There will be some outcome, but not any particular one. Mathematicians explain it regarding birthdays, so I will too.

Imagine you’re in a room with 25 other people. Mostly strangers, none who you know well. One of them is me, and I approach you with a bet.

“Would you wager $100 that two people in this room share a birthday?” I ask. Note, this is much easier on the internet because my poker face is terrible (and so is this bet).

“Hmm,” you think to yourself, “this seems like a good bet.” There are only 25 people in the room, and there are 365 days in a year. Chances are definitely against it. Right? “Sure,” you say, “I’ll take the bet.”

So you and I go around the room (with a paper plate) and write down birthdays until we get a match, and chances are that we will.

This birthdays bet (explained very well by John Allen Paulos in Innumeracy, and Clay Shirky in Here Comes Everybody) demonstrates the something will happen ethos that trend-following subscribes to. We can’t predict what birthday will match, only that one probably will. The math, very briefly, looks like this.

Trend-following lives in this same cul-de-sac of knowledge. There will be something that happens, and you can profit by acting when it does. (And now you have a bet for the next in-law family reunion)

Would you rather have a chance of 80% of yes or 20% of no?

Covel and Ritholtz touch a bit on Kahneman’s work on framing and loss aversion.

Look at the question above, it seems like they would be the same but Kahneman found that the responses people give are quite different.

If people are given a 40% chance on winning $100 or just to take $20, they’ll often favor the latter. The saying could go, $20 in hand is better than any psychology mumbo jumbo and rewards in the bush.

That’s well and good and unremarkable, except that people switch their choices around when the outcome is reversed. If people are given the chance to a 40% chance on losing $100 or just to lose $20, they’ll often favor the former. People are risk seeking to avoid losses. This matters in trading because if you’re trying to get back to zero, psychology suggests you’ll take more risks.

Related to this is loss aversion, which Richard Thaler explains beatutifully with a pyramid analogy. Also in that post is how Josh Brown creates win-win situations from down markets.

The prostate test test.

Covel says that he and Ritholtz are at the age for getting a prostate test, but should think twice about it. The side effects may be higher than advertised and the payoffs lower. (Note above we just mentioned our tendency to seek risks – have the test and side effects – to avoid a loss).

Covel says that reading Gerd Gigerenzer has changed his view on this. Gigerenzer has been on this blog before. When Scott Galloway spoke with Rithotz he outlined his five aspects of great companies. His model is simple and we noted that that’s good because we don’t want models that fit too well. In Gut Feelings Gigerenzer writes, “In an uncertain world, a complex strategy can fail exactly because it explains too much in hindsight.” That could be part of Cove’s apprehension of prostate exams. The other part is bad math, which Covel also got from Gigerenzer.

Let’s explain.

Pretend that 14% of a population has a disease, and a screening tool exists that is 98% effective. If we have 1,000 people, how many will be correctly diagnosed? Much like our birthday bet, things are not as they first appear.

Let’s do the easy math first. If 14% of 1,000 people are sick, then we have a chart that looks like this:

Has disease

Does not have disease

Total people: 1,000

140

860

Not so hard, and if we had a test with perfect prediction, then that would be the end of it. But our test is only 98% accurate.

Of our 140 sick people, we will correctly identify 98% of them, 137. Our chart gets updated.

Has disease (140)

Does not have disease (860)

Tested positive

137 (98% of 140)

Tested negative

3

Then we do the same to the ‘does not have disease’ group.

Of our 860 not sick people, we will correctly identify 98% of them, 843.

Has disease (140)

Does not have disease (860)

Tested positive

137 (98% of 140)

17

Tested negative

3

843 (98% of 860)

We see then that 20 (3+17) of our original 1,000 people will get the wrong diagnosis – 5% of the general population.

Now if you thought this was a bit murky math, you aren’t alone. Doctors miss this too.

Successful people have systems, and follow the rules.

“This is not a day to day guessing game,” Covel says. There’s not single point in the interview where I noted the emphasis on systems, but by the end it was clear. Covel is a systems advocate. When Dennis taught people, he taught them a system.

When Covel speaks about trend-following he explains it as a system with rules:

1- What’s the portfolio?

2- What will force you in?

3- How much will you be in for?

4- When will you exit for a loss?

5- When will you exit for a win?

Those questions are easy in hindsight, but hard in application. In part because it takes time and temperament.

Systems don’t have to be complicated either. Ritholtz says “never ask a room full of people what they want for dinner.” That’s a system too. Like a basic computer code or logic statement; if more than 8 people, then do not ask what people want for dinner.

Covel’s rule #4 (When will you exit for a loss?) is easy to state, but hard to act on. Ritholtz says that when he was a trader it was “okay to be wrong, but not okay to stay wrong.” You can’t reach and try to get back to even because you’ll take more risks getting there.

Some problems are too hard for any system. In his book The Hard Thing About Hard Things, Ben Horowitz notes that for hard problems there’s no prescription.

“The problem with these books (about business) is that they attempt to provide a recipe for challenges that have no recipes. There’s no recipe for really complicated, dynamic situations.”

The best systems are ones where the big mistakes are eliminated (as best they can be, but never absolutely) and wiggle room is given for the small choices.

, and Clay Shirky in

, and Clay Shirky in  ) demonstrates the something will happen ethos that trend-following subscribes to. We can’t predict what birthday will match, only that one probably will. The math, very briefly, looks like this.

) demonstrates the something will happen ethos that trend-following subscribes to. We can’t predict what birthday will match, only that one probably will. The math, very briefly, looks like this.  , Covel suggests

, Covel suggests  ,

,  ,

,  ,

,  , and

, and