There’s an interesting investing idea in personal finance to be like Rip van Winkle. If investors don’t earn the market returns because they churn, maybe they would be better off setting it and forgetting it, of sleeping-on their investments.

I was reminded of this story because I forgot a password. Does invest like you forgot your password have the same flair? Eventually I logged in and checked our contribution amounts for 2020.

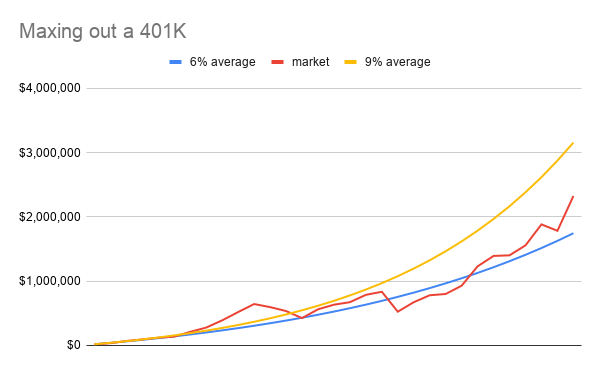

While poking around I wondered what a retirement account would look like if someone were to maximize their 401k ($19,500 in 2020) each year. Sometimes the government changes the limit of what an employee and employer can contribute to a retirement account. As someone who likes simple and effective plans I thought this was great financial advice. I could see advisors telling their clients, just aim to hit the max number each year and you’ll have this much.

I calculated the rate changes each year and found out that contribution limits change at about the same rate of inflation. Of course. The IRS calls these ‘cost of living adjustments’. Sometimes you just need to stumble on things yourself.

The S&P average over the last thirty years was 9.69%. The picture looked like this.

This doesn’t account for an employer match, social security, or other savings but it’s comforting to know that the real 4% withdraw at retirement is $93,000 annually.

Digging into this made me realize how much variation can occur in planning. Cost-of-living, family situations, businesses, multi-income families, income levels, mortgages, taxes, and so on can all swing the equation one way or another. Ditto for flexibility in needs and wants.

However, just because there is a lot to consider doesn’t mean there’s not a simple plan. Specific predictions are futile but ballpark approximations are possible, helpful, and a good way to frame potential outcomes.

[…] looked at spreadsheets for emergency funds, 401Ks, and how many touchdowns a quarterback will throw. Spreadsheets offer precision with numbers but […]

LikeLike

[…] touched on this idea in the Maximizing a 401k post and considered the tradeoffs between a 401k and a 15-year mortgage […]

LikeLike