Michael Mauboussin (@MJMauboussin) is back, this time with Barry Ritholtz (@Ritholtz) on his Masters in Business podcast to talk about luck, skill, and alternate histories. The interview occurred in 2014 when Mauboussin was promoting his book, The Success Equation: Untangling Skill and Luck in Business, Sports, and Investing

Mauboussin also spoke with Shane Parrish (more recently, 2015) and that interview was also very good.

Some of my favorite conversations that Ritholtz conducted were the Howard Marks and Richard Thaler ones.

Mauboussin is a smart guy, and we can take a lot away from his talk with Ritholtz. A few things we’ll try to answer:

– How to get lucky, in general.

– The answers to the Big Fish, Little Pond – Little Fish, Big Pond question.

– How anyone can think like a great investor.

– What does “ugh” really mean.

– Two short thoughts on better statistics.

“We’re up all night to get lucky” or Watch out for Fortuna at the club

I like to imagine a world where the goddess Fortuna comes to earth and dances at a Daft Punk show. Neil Gaiman would write it. It would be awesome.

Luck, from ancient Greece to the song of the summer (2013), is a feature of life. Mauboussin makes the case that we can think about it analytically and wisely and maybe dance to the music a little more.

There are three components of luck Mauboussin says.

- It could happen to you or your business.

- It could be good or bad, but not necessarily equally.

- Another thing could have happened.

It’s this third that we can dive into and start to think about more, because it’s a hard thing to think about. Too often we think of what happened, but the list of options is far beyond that. Nassim Taleb writes about this in Fooled by Randomness

“I start with the platitude that one cannot judge a performance in any given field (war, politics, medicine, investments) by the results, but by the cost of the alternative (i.e., if history played out in a different way). Such substitute courses of events are called alternative histories.

The classic example is that a of a cab driver who drives like a maniac. The outcome (you arriving early) isn’t how you should judge the situation. The alternative histories would be you getting into an accident and; at best being late, and at worst death.

Our problem is that we don’t see these possible outcomes, we just think that what happened once is the case for what might happen again.

In an outcome then, you need to figure out how much of what happened was luck. How do you compute what was luck? This, suggests Mauboussin, is quite easy. Figure out what was beyond your control. The weather is out of your control. The supply chain is in your control. Walmart can’t move hurricanes, but they are notoriously good at stocking stores immediately before and after a storm.

Luck is like the fog around an outcome and our job is to figure out how many outcomes we can’t see. If there are many, then the portion of luck in a decision is quite high. If there are few, then luck is low.

The paradox of skill, or why you want to be a big fish in a little pond

That comes with a certain caveat. If you want to be the best at something, it’s easier to be the best in a smaller pond. When Lewis Howes talked to James Altucher he said that he chose to take up handball because he had a chance to make the Olympics team. Howes is athletic, physically strong, and mentally tough. He’s could succeed at many sports. He chose handball to be a big fish in a small pond.

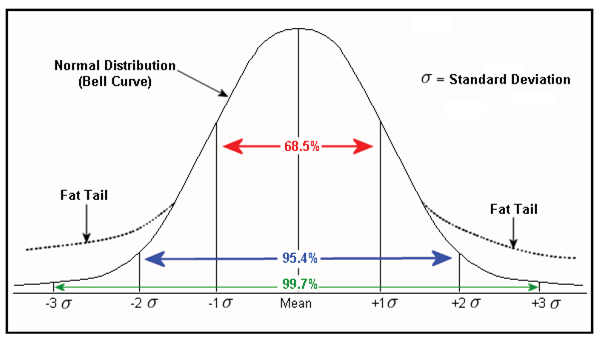

We can see this in a normal distribution graph, and then with pizza.

When we find situations where skill matters less, we have a “wider” distribution or one with “fat tails.” In these instances there are more people that are 4 standard deviations above the mean. Mauboussin gives the example of Ted Williams, the last player to hit over .400 in a season.

When we find situations where skill matters less, we have a “wider” distribution or one with “fat tails.” In these instances there are more people that are 4 standard deviations above the mean. Mauboussin gives the example of Ted Williams, the last player to hit over .400 in a season.

Why was the distribution wider/Why did it have fat tails? The reasons Mauboussin explains is that the skills was watered down. Baseball drew from a smaller pool than the population at large.

As more, and better players, entered Major League Baseball, the distribution got more narrow. More narrow meant fewer people 4 standard deviations beyond the mean.

Okay, with the statistics out of the way, let’s turn to pizza. If your town has one pizza place there’s not a lot of incentive to create better pizza or dining for your customers. No owner is willful about bad food, but a lack of competition is a lack of innovation.

This gets back to Peter Thiel’s idea in Zero to One

That’s why – in part – these blog posts are so long. There are a lot fewer sites that feature infrequent long posts, and better opportunities for success.

- Lewis Howes in handball rather than football, is a big fish in a little pond.

- Ted Williams playing in 1945 rather than 2005, is a big fish in a little pond.

- The lone pizza place in your town, is a big fish in a little pond.

Each succeeds in relative terms because the competition is less.

This effect is bemoaned each time Bill Simmons talks to anyone about soccer. His podcasts with Marc Stein – at ESPN/Grantland prior to 2014 – always included the question, what if our best athletes played soccer? The best American athletes don’t play soccer. Hence the United State is less good at soccer than other sports. If you want to succeed in relative terms, it’s better to be a big fish in a little pond.

Let us pause in a moment of silence for the deceased.

All this talk about success leaves the question, well what happens to everyone else? If Ted Williams was 4 standard deviations above the mean, what about the guy 4 below? The answer is that he dies.

Not usually literally, though sometimes this is the case, but we don’t learn from him. This is the survivorship bias, and one we should be mindful of. In the Peter Diamandis and Steven Kotler interview I noted that their list of examples is a who’s-who of internet search results. It sound great to learn from Jeff Bezos and Elon Musk, but to what extent can we mimic them?

We can learn some things, but probably not everything. Go back to Taleb’s comments about alternative histories and we can easily imagine a situation where Amazon’s lack of profitability doomed the company and Walmart filled the void.

Mauboussin’s focus in on investing and if we bring things back around to it we can see why he looks at luck. Investing has gotten more dependent on luck, but it’s not luck entirely. When we see someone like Warren Buffett or Ray Dalio do well consistently, we should recognize that they do something in their process that lets them have better results. Mauboussin has some ideas how anyone can think like them.

How anyone can think like a great investor.

Great investors, says Mauboussin, do three things especially well.

1. “Focus on process and no so much on outcome.” The best investors understand the dance with luck we just talked about says Mauboussin. They use this to frame their decision making models on process not outcomes.

We can apply this to many parts of our lives. Adam Carolla asks how you might act if you got a ticket for rolling through a stop sign. Will you question your ability to drive? Probably not. That’s a focus on process not outcome.

Carolla said there’s been 2,000+ shows rejected since his first one was declined. But, he did his best work and that’s all that matters. For Carolla the process – the work he does – is more important than the product – whether his show gets ordered or not.

2. Have some sort of an edge. A lot of great investors have some kind of edge says Mauboussin. They evaluate data better. They have a peaceful home life. They have the fortitude to examine something more than others. It may even be where they live.

Mauboussin says that successful investors live all across the country, not just in New York City or Boston. Warren Buffett’s success may be partly thanks to living in Omaha. These geographies, Mauboussin says, “don’t have the cacophony.”

Scott Adams – creator and drawer of Dilbert – says that his edge comes from leverage of his mediocre skills.

“I’m a perfect example of the power of leveraging multiple mediocre skills. I’m a rich and famous cartoonist who doesn’t draw well. At social gatherings I’m usually not the funniest person in the room. My writing skills are good, not great. But what I have that most artists and cartoonists do not have is years of corporate business experience plus an MBA from Berkeley’s Haas School of Business.”

There needs to be something different about you. Ritholtz said that he can name 20 books that 90% of Wall Street trades have read. If you read the same things and think the same way, how can you be different?

3. Have longer time horizons. Great investors think long term, something that is apparently harder and harder to do on Wall Street. It takes time to do anything worth doing the saying goes, and it’s been true for other interviewees.

“Success is something you do over time” says Jack Canfield, author the Chicken Soup series of books. Brian Koppelman said the same thing about trying to get the movie Solitary Man made, “I knew I had to do something everyday.” And it doesn’t have to be something big.

Bonus They read widely. It’s similar to what Stanley McChrystal said in his interview and it comes up time and again here. Read, and read widely.

How to avoid emotional swings.

Howard Marks had told Ritholtz, “The biggest investing errors come not from things that are factual or analytical, but from those that are psychological.” It’s us tripping over our own feet, selling on the way down and buying on the way up. Unlike clever computer programs that can terminate a function if something goes wrong, our emotions are a runaway train.

Or are they?

There are a few things we can do to tackle the emotional surges we feel without suffering negative consequences.

We can start if we know the name of the thing. This is the Rumpelstiltskin Effect and it’s apparent in many places. It’s why Elon Musk suggests people look at the semantic tree of what they are studying and it’s how Adam Savage figures out the exact item he needs.

Like a spike in the stock market could be the needle that Sleeping Beauty pricks her finger on, our knowledge of what follows is akin to the prince’s kiss that will wake us up.

- Know what’s happening. In his book, The Hour Between Dog and Wolf

, Wall Street trader turned neuroscientist John Coates, writes that our hormones may work against us. If we make a positive trade, writes Coates, we get a dose of testosterone which increases our risk taking. When we lose money we get a dose of cortisol which may make us too timid.

- “People chase a face,” Ritholtz says, and not kindly. We think that if we follow someone who knows what they are doing, we too will do well. Maybe, probably not. As Nick Murray talked about, that person may just be above the mean, thanks to in part, luck. At some point their luck will change, and if they had good luck prior to that, it won’t be so great after.

- Stick to your plan. You can’t, said Nick Murray, chase both gains and follow a plan. It just can’t be done. Instead you need to spend the time upfront with a plan and not get caught up in swells.

- “Know that your emotional tugs will be in the opposite direction of what your actions should be.” Mauboussin said this as it relates to rebalancing your portfolio. This is when you sell high and use those proceeds to buy low. Murray says this rebalancing should happen at least annually. It means selling $AAPL (Apple) high and buying $CAT (Caterpillar construction) low. It doesn’t seem like the right thing to do, but more often than not, it’s a profitable and safe way to create a better portfolio.

Let their “UGHS” show you the way

There are a lot of people who use certain signals to help guide them. Ramit Sethi has certain words he likes to see on employment applications, Barry Ritholtz has them for clients. Van Halen had no brown M&M’s, banks have questions about guard dogs, and Stephen Dubner wrote an entire chapter in a book about these ideas.

If we can create situations where certain signals mean something, we can gain a lot of information from one small question. Here’s another one we can add.

If you go around the office with a certain idea and everyone says “ugh” to it, it might be worth exploring. This goes back to the central point above, it would make you a big fish in a small pond and give you an edge.

Now this may not work, but Ritholtz has anecdotal evidence. He was pushing to buy Apple when it was at a pre-split price of $15/a share. “Every single one of the ughs,” says Ritholtz, “was giving the consensus view and emotion.” Ughs are where the small pond is. They are the front that Colonel Blotto orders you to take. They hint at Zero to One

Better statistics

Like Midas before (and companies now), if all you want is gold (data) then you too will die. Data is nothing. “Statistics are often telling you what the questions are, not the answers,” said Tyler Cowen.

But in his interview Mauboussin provides a context to grade data. “Not all data is created equally,” he tells Adam Grant in a Wharton interview, “and there are two things we want from our data.”

- Persistence. “The statistics are correlated from one period to the next.” Are sales high and then low? Do they match seasonally? There should be some idea of whether the data is consistent period to period or not.

- Predictive value. “Statistic is correlated to some result.” That is, if the data matches what happens. Sales may fluctuate, but does it match revenue?

You can see more of Mauboussin’s interview with Grant here:

–

Thanks for reading, I’m @MikeDariano on Twitter. If you couldn’t tell from the movie references, I do indeed have two young children.

[…] Michael Mauboussin II […]

LikeLike

[…] notes on Joshua Foer’s conversation with James Altucher. – I also wrote up notes from Michael Mauboussin’s 2014 talk with Barry Ritholtz. Mauboussin is always informative and this was a great hour to listen to. – Over at Medium I […]

LikeLike

[…] Michael Mauboussin #2 […]

LikeLike

[…] Michael Mauboussin #2 […]

LikeLike

[…] Michael Mauboussin looks at luck like a baker does sugar – a […]

LikeLike

[…] than blame bad luck, we can figure out how much of a role it played and make adjustments. Michael Mauboussin says that we can see how much luck and skill matter by asking if you could fail on […]

LikeLike

[…] thankful he straddled the internet and pre-internet worlds. It gave him time to learn and think. Michael Mauboussin said that living somewhere without the financial cacophony may be part of what makes someone a […]

LikeLike

[…] under other names. Peter Thiel calls it Zero to One. Lewis Howes plays handball because of this. Barry Ritholtz listens for “Ughs.” Michael Mauboussin uses game […]

LikeLike

[…] you want to succeed, be a big fish in a little pond. Michael Mauboussin explained how the numbers tell the story. The more people there are, the more skill there is and […]

LikeLike

[…] Figure out the role of luck. In everything we do there is some component of luck. Michael Mauboussin said that luck is more important when skills converge. Winning the NBA championship requires some […]

LikeLike

[…] Griffin and Michael Mauboussin speak about mental models quite a bit. So does Sanjay Bakshi and even Phil Rosenthal suggests there […]

LikeLike

[…] “stumbling,” how else does Gladwell work? In one word, comfortably. Gladwell, like Michael Mauboussin enjoys physical books because of the tactile and emotional memories in them. Gladwell says he can […]

LikeLike

[…] books. Something has to be really good, for him to read an industry book at night, Zweig says. Like Michael Mauboussin, he prefers physical […]

LikeLike

[…] “There’s a sense of geography in a printed book that’s really helpful,” August says. Michael Mauboussin said the same thing in his […]

LikeLike

[…] value of mental models has been trumpeted by many. Tren Griffin and Michael Mauboussin speak about mental models quite a bit. So does Sanjay Bakshi and Phil Rosenthal suggests there is […]

LikeLike

[…] Michael Mauboussin #2 […]

LikeLike

[…] else do you get Maghan Trainor and Michael Mauboussin in the same blog […]

LikeLike

[…] Michael Mauboussin said that he writes (and speaks) about his ideas to understand them. […]

LikeLike

[…] acting does imply accuracy. As Barry Ritholtz points out when he spoke with Michael Mauboussin, Jason Zweig, and Ken Fisher – “don’t just do something, sit there” can be […]

LikeLike

[…] would too. So would you. It’s hard to get the right level of reaction. Michael Mauboussin talks about the difficulties of updating our beliefs. Tren Griffin quotes Charlie Munger on it. […]

LikeLike

[…] well can I write this is a proxy for how well do I understand it. Michael Mauboussin, Barry Ritholtz and Maria Popova explicitly mention that writing is a form of […]

LikeLike

[…] by a fraction of people who watched Melrose Place at its height,” Gladwell says. Thanks to Michael Mauboussin, we can explain […]

LikeLike

[…] Michael Mauboussin applied it to business. […]

LikeLike

[…] spoke about being different in investing. Judah Friedlander spoke about being different in comedy. Michael Mauboussin spoke about being different in […]

LikeLike

[…] Michael Mauboussin noted that investors share this advantage too if they are away from the cacophony of Wall Street. Chris Dixon talked about the value of being where things are quiet. Tadas Viskanta and Tyler Cowen both explained why this is harder now than ever before. […]

LikeLike

[…] hard to separate luck from skill, especially in a changing landscape. Michael Mauboussin suggested to use inversion to figure it […]

LikeLike

[…] Michael Mauboussin joined Barry Ritholtz on the Masters in Business podcast and I loved every minute of it. Mauboussin is great, and I’ve taken notes on some of his other conversations; Michael Mauboussin with Shane Parish and another with Michael Mauboussin and Ritholtz. […]

LikeLike

[…] Mauboussin. I’ve written about his podcast interviews three times(!!); Michael Mauboussin, Michael Mauboussin 2, & Michael Mauboussin 3. I think my 1990’s Van Halen collection had fewer […]

LikeLike

[…] why people like Daniel Kahneman and Michael Mauboussin advocate for the outside view. Be conscious of ‘what typically happens’ – or […]

LikeLike

[…] is our fourth(!!) post from a Michael Mauboussin podcast. There were these; Michael Mauboussin and Michael Mauboussin from conversations with Barry Ritholtz, and one – Michael Mauboussin – from The […]

LikeLike