Nick Murray joined Barry Ritholtz (@Ritholtz) on the Bloomberg Masters in Business podcast to talk about financial advising, psychology, and the single best thing an advisor can do. Though the conversation focused on finances – like many other domain specific examples we’ve featured like Andy Weir on writing or Amanda Palmer on performing – there is much for anyone to learn.

Murray is the author of numerous books including Simple Wealth, Inevitable Wealth and runs a newsletter at his site NickMurray.com. At “cocktail parties” he refers to himself as “an advisor to other financial advisors” and has decades of experience in financial services. Murray is smart. Ritholtz is too. Let’s see what we can learn.

#1 The mutual exclusivity of gains and plans.

You cannot, Murray says, chase both gains and follow an investment plan. “The best and easiest way an investor can blow himself up is chasing Alpha,” Murray says. Alpha in this case is the idea that you can compare one investment with some volatility to another with similar volatility, and have the former beat the latter. If this were sports, Alpha is being 3 wins better than another team that made a similar number of player trades.

You can chase Alpha if you want, Murray says, but you can’t do that and follow a retirement plan. You’d better pick one because we follow what we track. Seth Godin for example, does not track his book sales. He doesn’t look at his rank on Amazon or website traffic. Those metrics don’t matter to Godin so he doesn’t look at them. But Godin also admits that if he did look at them, he would want to improve them.

Where we look matters both professionally and personally. When Gretchen Rubin was trying to change her habits, she realized that if she paid attention to something, she did better with it. When she tracked her steps, she walked more. When she tracked her time, she paid closer attention to how she spent it.

If we turn things back to the financial realm, we can see that daily, weekly, and monthly numbers should be ignored. For most investors, Murray says, three steps is all they need.

- Figure out how much capital you need at retirement.

- Figure out the dates and dollar specific benchmarks to hit along the way.

- Figure out an asset allocation model that follows from number 2.

That’s it. But do we do this, no we do not.

We look at people like Warren Buffett, Howard Marks, or Ray Dalio and think hey, I could do that. Those guys know a lot, but there’s something we can learn from them too. They all read like crazy.

#2 Be a reader.

If you want to do well, you have to be a reader. Murray says that financial books are especially good about reminding us about the lessons of history. Curl up with a book like Rainbows End during the next financial crisis and you’ll see.

The power of reading, says Murray, is that it creates “adult memories” for us. He talks about going through different crashes, booms, and cycles and says that the people who were least prepared where the ones without an adult memory.

And this idea has been around for thousands of years. Seneca, wrote:

“Men who have made these discoveries before us are not our masters, but our guides…By other men’s labors we are led to the sight of things most beautiful that have been wrested from darkness and brought into light; from no age are we shut out, we have access to all ages.”

The value, says Murray, is that we can start to see the patterns of human nature. We see when people want to survive, want to conquer, or want more. We can see how men want to win big, and if we read we can see how.

Murray is certainly not the only one who advocates reading. Michael Mauboussin and Maria Popova both said that their deep understandings are not just from reading, but from speaking and writing about those things. Charlie Munger – oft-quoted wisdom – said, “In my whole life, I have known no wise people (over a broad subject matter area) who didn’t read all the time – none, zero.”

#3 How to win and win big.

The best investment option, says Murray, is be in the game with a plan. “The dominate determinate to long term financial outcomes is not investor performance, it’s investor behavior.” If you cash out at the bottom and buy in at the top you will never win. Of course you don’t do that, except maybe you do. Research shows that over ten year cycles, mutual funds have 10% returns but investors only realize 5%. Why?

We have those numbers because we sell too low and buy too high. “I’m absolutely convinced that turnover is correlated negatively to return,” Murray says. Instead we need to wait and slow down. “Don’t just do something,” Murray says, “sit there.”

Brad Feld say this axiom play out when he stopped flying around the country to put out fires at his investments. Nassim Taleb writes

If we do want to make a change, we can focus on small infrequent actions rather than big sequential scenes. Howard Marks told Ritholtz that the best investors he met were the ones who were consistently above average but never “blew up” (see #1). It’s not just investors, but anyone can apply this thinking. Steven Kotler said that the best athletes he observed improved 4% with a hyper focus on their fields. Not an extreme athlete, but Charlie Munger uses the same approach.

From Tren Griffin.

“As a “know-something” investor, Munger is what he calls a “focus investor”—buying very few stocks relative to the size of his portfolio. In other words, he does not follow wide diversification. In fact, he believes that for a “know-something” investor, portfolio concentration decreases risk if it raises both the intensity with which an investor thinks about a business and the level of comfort he or she has with its economic characteristics. It is important to point out that Munger defines “risk” as a permanent loss of capital and not volatility, as it is often defined in today’s markets.

Focus and make small improvements daily are two key steps toward a big win. If also helps to know a bit about psychology.

#4 How have a great restaurant meal (have a bad one first).

The expression “buy low and sell high” makes logical sense. Our emotions though are not logical. Our emotions want the stock that’s going up and not the one going down. But as the prospectus says, past performance doesn’t not indicate future returns – and often it never will.

What we’ve found here is mean reversion, “something the average investor is not thinking about,” says Ritholtz.

What is it and what can we do? Let’s think about food first.

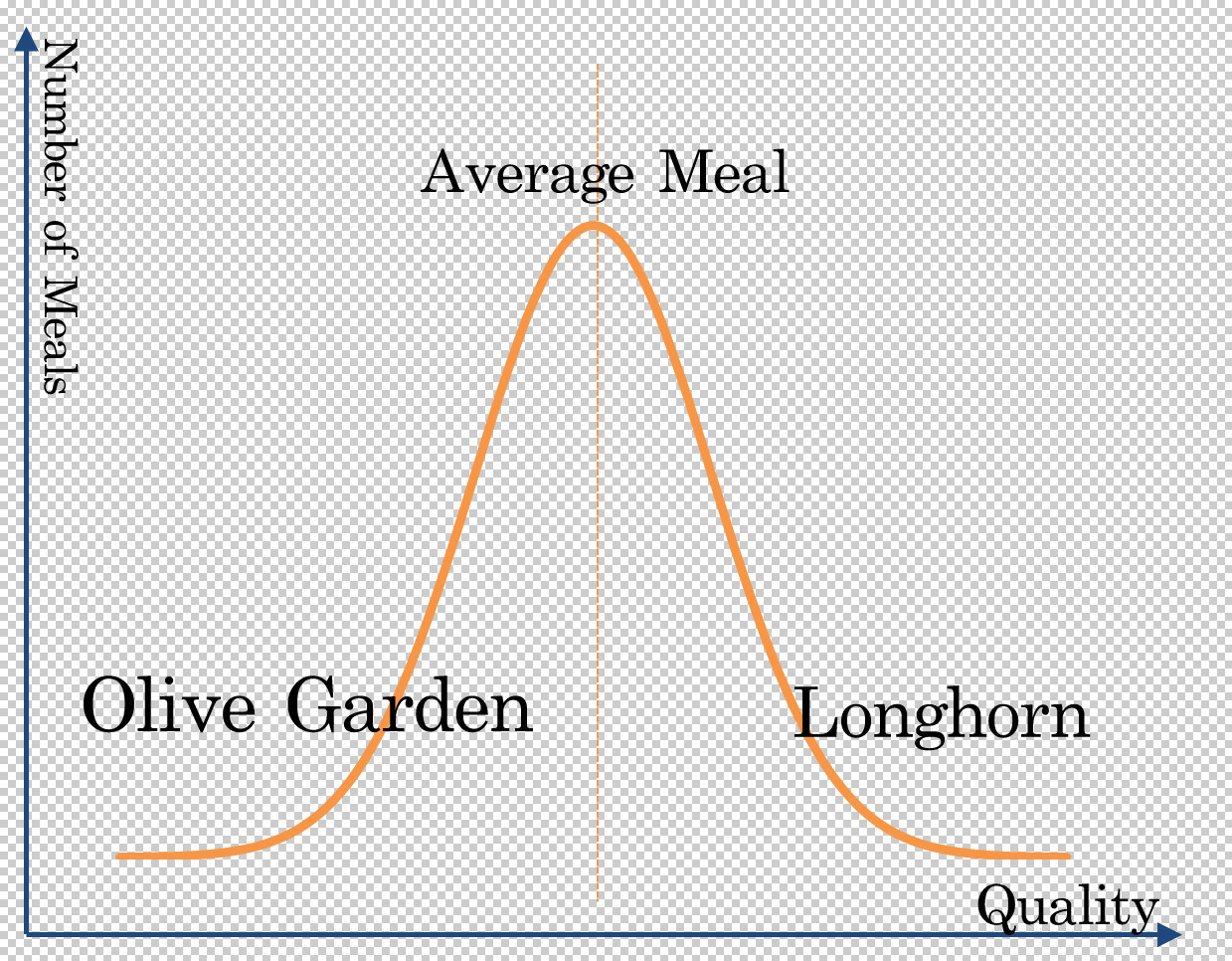

Imagine you go out to eat at Olive Garden. You walk in and the wait is long, the food is tepid, and the staff is unfriendly. The next week – having learned your lesson at Olive Garden – you go to Longhorn Steakhouse where the wait is short, the food is fantastic, and everybody knows your name.

Which restaurant is better?

In the scope of places to eat, those two restaurants are essentially the same (the same company owns them) but you had notably different experiences. What gives?

Reversion to the mean is an explanation that there are scattering of experiences (the orange line) you could have at a restaurant. Some will be good (Longhorn), some will be bad (Olive Garden).

You could theoretically have a lot of above average experiences (more on the Longhorn side of the hump). Eventually though, your good meals will balance out with the bad and most of your meals will be about average.

Okay, but beyond a restaurant how does this apply to our lives?

If your investments do better than average, you are probably having what’s equivalent to a good experience at Longhorn Steakhouse. But you should know that your next experience (next quarter, next year) with that investment will be like the Olive Garden one. That’s how you average out.

We can avoid this, Murray says, by getting out of the hot experiences once we have them. Annually rebalancing is “a total no-brainer,” he says. If we continue our restaurant metaphor it’s like switching to a new class of restaurants, maybe the local Mexican and Mediterranean places. Even if we switch and have a bad experience there, that’s fine. We can keep eating there knowing it will improve back to the mean.

Reversion to the mean is a powerful construct and if you see it once you’ll start to see it everywhere. Thinking this way is one way to avoid chasing options that have already one and have no place to go but down. Another way to insulate yourself is start thinking like a dog.

#5 The benefits of being a Pavlovian dog.

Pavlov is the famous physiologist who trained his dog to salivate at a tone he rang a bell rather than the actual presentation of food. Besides helping his research on saliva, it’s also a good filter we can install in our lives. If we can arrange for automatic actions to prevent us from doing dumb things, then we’ll do dumb things less often.

A personal example of this is the extended warranty. My rule is to never get the extended warranty. Over time I know that never getting one will mean more dollars in my pocket than always getting one or sometimes getting one. Beyond just washing machines warranties, we can create other automatic response too.

Ritholtz says that his wealth management group’s survey questions have an aspect of this.

“We have a couple of CFPs in our office and they have a list of knockout indicators. When people start asking questions about sharpe ratios and things like that, they really want a hedge fund more than a long term plan. You want a whole lot more juice, a whole lot more cocktail party chatter and that’s not what we do. We’re boring.”

Ritholtz has, in the words of Stephen Dubner “taught his garden to weed itself.” He’s not the only one.

When marijuana was legalized in Washington there were a lot more business with cash to deposit. Banks though were in a difficult spot because marijuana was legalized statewide but not nationwide. Some banks saw an opportunity, but wanted to proceed with caution. How could they deal with only the most scrupulous and legally aligned growers? The bank created their own “knockout indicators.” As one bank manager explains:

“We want to know if their company location has any of the following security access, security cameras, security alarms, 24 hour surveillance. The answers to those questions should all be yes. Armed guards or guard dogs? The answers to those two questions should be no.

Getting those answers correct isn’t crystal clear to someone running a marijuana dispensary and those questions weeded out – pun intended – the wrong people.

Ramit Sethi has done the same thing in his hiring process and Van Halen did it to ensure their lighting rigs were set up correctly.

Financial advisors though have another challenge. Not only do they need to educate their clients (teach them to think one way when the bell rings) but they have to combat all the other bells that are ringing. Those bells sounds like gold coins during the Facebook IPO and it’s one of the two biggest financial risks anyone can take.

#6 What are the two biggest financial risks?

There are two big financial risks says Murray. Outlive your money and watch too much television. Let’s get the easier problem out of the way first.

Television is a mess, says Murray, “you can never get truth from media, you can only get news.” And news as a long term investor is not what you want. The daily or monthly market movements are, “of no long term importance,” says Murray, “they are only distractions.”

The problem is a race to the edge of crazy. There are so many voices that want your attention that each voice tries to be louder and more outlandish than the next.

This leads to a crazy mess where you don’t know what to believe. So, like a cluttered restaurant menu at a place you’ve never been before, you pick something that sounds familiar. In the crazy world of news we do the same thing.

This creates a positive feedback loop for what we eat. I don’t recognize anything -> I’ll order the sweet and sour chicken -> (the next time) I don’t recognize anything -> I’ll order the sweet and sour chicken….

We’ve entered the trap of the availability bias. Now, this isn’t a blog focused on psychology per se, but knowing where you are likely to mess up is a big help for not messing up. Counterintuitive thinking is a skill that anyone can hone and be helped by. It’s why Howard Marks says that you can’t beat the crowd if you follow the crowd and is the essence of Peter Thiel’s book Zero to One

To get out of the positive feedback rut, we need to find opinions that are different than ours. Charlie Munger does this with his two track thinking. Nassim Taleb writes about it in Antifragile. Garrett Hardin gives filters in Filters Against Folly

The harder problem is a much bigger one, that you will outlive your money. We already answered this problem in #1.

#7 Whatever you do, do not confuse volatility with risk.

As this is a post with many analogies, let’s add more. Imagine you enjoy watching tennis. The strategy of the player’s factors into each shot. It’s a display of human stamina, skill, and endurance. It brings you to the edge of your seat as the match progresses.

Now imagine you are riding in an airplane in heavy turbulence. The pilots also use their stamina, skill, and endurance to safely fly the plane, but do you enjoy it? Why not?

It’s more or less the same thing. You observe a situation where a person must exhibit some skills to avoid some consequences.

Sure, you may die on a plane, but the odds of that are small. Only 761 commercial airline deaths occurred worldwide in 2014. You were 50X more likely to die from the flu, in the United States alone. Flying, is not dangerous, but may be volatile.

Risk is the chance of a blow up, risk is the flu.

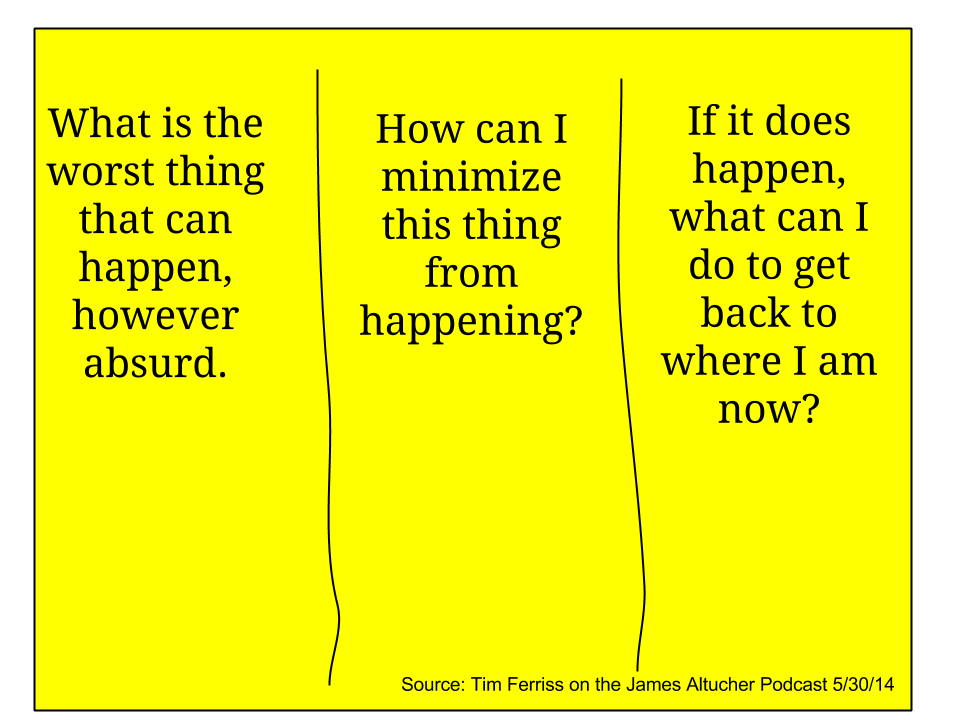

As Tim Ferriss said, “we have a nebulous fear of risk.” Very few things will zero-out our balance and we can often afford more volatility in our lives. If you want to try, here’s Ferriss’s framework.

Other miscellaneous points

- Technology is fallible. I was reminded of this when a simple zip-top bag with convenient “slider” failed to work. How does a zip-top bag fail to work when it doesn’t have a puncture? Murray has the same thinking if you replace “zip-top baggie” with “robo advisors.” Like we should be wary of action for the sake of action, so too technology for the sake of technology.

- The largest positive change in financial advising has been the increased role of women. In true econ-speak, this “untapped resource,” has been a boon to the industry. Women, Tyler Cowen has written

, face the biggest upside for employment in the future. Their ability to learn, empathize, and remain emotionally balanced are perfect fits for the new economic landscape.

- Avoid vogue and du jour items and options. It’s partly explained when Murray talks about churning, but any switches have some costs. Vogue options – more than others – may have great costs because they may be a straw man.

- Two books have had core philosophical influences on Murray. The Road to Serfdom by F.A. Hayek and Stocks for the Long Run by Jeremy Siegel. I’ve added both to my growing piles.

[…] Nick Murray […]

LikeLike

[…] Notes from Nick Murray’s conversation with Barry Ritholtz (where I shared decision making summaries) […]

LikeLike

[…] Nick Murray […]

LikeLike

[…] Nick Murray […]

LikeLike

[…] Barry Ritholtz says that when he hears “Sharpe ratio,” it’s a signal people want a hedge fund. When he hears […]

LikeLike

[…] from harming themselves. “The dominate determinate to long term financial outcomes,” said Nick Murray, “is not investor performance, it’s investor […]

LikeLike

[…] happy. It’s difficult to chase both happiness and success says Naval. It’s analogous to to what Nick Murray said about plans and gains. Your financial goals need to be one or the other. You can’t have a […]

LikeLike

[…] Nick Murray said this too, “the dominant determinant to long term financial outcomes is not investor performance, it’s investor behavior.” It’s more about how you act rather than what stocks you pick. But how do we act in a logical way when our reptilian brain does so much without us even noticing? We have two options. […]

LikeLike

[…] is up to you to define. The key is to define it clearly. In the same way that Nick Murray said you can’t chase financial plans and financial gains, your terms of success can’t be […]

LikeLike

[…] boss firing me if I have a hundred bosses,” Adams says. Diverse options make Adams less stressed. Nick Murray said that too much financial television (lack of diversification in news) is one of the biggest […]

LikeLike

[…] last year. The Hawks might have overachieved, and them being a bit worse (mean reversion, see this Nick Murray post for more ) makes sense. That’s an easier case than figuring out if the Knicks will be better […]

LikeLike

[…] In the Nick Murray post we used the 3 questions to explain Murray’s investment […]

LikeLike

[…] Nick Murray […]

LikeLike

[…] Disney said, “doing nothing can be a very powerful action unto itself.” Barry Ritholtz and Nick Murray suggested the don’t just do something, sit there […]

LikeLike

[…] Nick Murray said the easiest way for investors to blow up is to chase big gains. […]

LikeLike

[…] term success and short-term success often have different actions. Nick Murray said, “I don’t know how anybody who’s a counselor to advisors who are trying to get their […]

LikeLike

[…] “Confirmation bias is the most insidious because you don’t even realize it is happening,” says Morey. “The normal mind takes out of the noise what it wanted to hear all along,” said Nick Murray. […]

LikeLike

[…] talk to customers. It’s one-way startups fail. “The normal mind,” said Nick Murray, “takes out of the noise what it wanted to hear all […]

LikeLike

[…] wrote for tennis what Calacanis wrote for angel investing. Ray Dalio explained this to Tim Ferriss. Nick Murray warned, “The best and most easiest way he can blow himself up is chasing […]

LikeLike