Mohnish Pabrai was on “The Investor’s Podcast” with Preston Pysh and Stig Brodersen. There were two parts (part1 & part 2 ) and they were fantastic.

My first post about Pabrai were notes from a talk he gave at UC Irvine ( mostly about Coca-Cola). This podcast covered new ground.

Before we jump in. The ~12:00 of part 2 had some ideas related to our thoughts on Moats and Podcasts.

Ready?

1/ Deep understanding. Pabrai said that many of his business classes were interesting but easy for him because he had spent his teenagers years working for his father. He and his brother “were like my father’s board of directors.” Pabrai had already studied the problem, made mistakes, and learned from experience.

“I very accidentally got an introduction to business,” Pabrai said, “during a period of time when my brain was optimized to pick it up.”

This was a theme of the interview, the formative years of brain development. I’ve heard about this as it relates to learning how to play instruments and speak languages but never thought of it in terms of business acumen (domain blindness on my part).

Gary Vaynerchuk may be our proto-contemporary example of this. Vaynerchuk spent his teenage years working in his father’s liquor store. There Vaynerchuk learned to sell, add-on, and study wine.

Pabrai mentions Warren Buffett as someone who did this too. Buffett would buy a six-pack of Coke for a quarter and sell each bottle for a nickel.

You and I are no longer teens (biologically), but we can still appreciate the value in a deep understanding.

…

2/ Just do it. When should you think and plan and when should you do and act? I don’t know. Pabrai though has two suggestions for when to just do it.

a) If an interesting opportunity arises,“Take the plunge, you can always come back, so take the plunge.” “Life is a very random journey. I’m here talking to you because I picked up a book at Heathrow airport, and it could have been a book on a number of different subjects.” “No one is going to put up a headline that says, ‘take the left fork.'”

b) If someone wise tells you to do something. Pabrai said he “lucked out,” because he was exposed to Buffett’s letters early on. Pabrai was a blank slate, so he imitated Buffett and Munger. It’s worked out.

Yeah, but… NO! No ‘yeah, buts.’

“Some of these I understood when I was starting my own partnership. Other I did not understand the reason but I still just owned it because there was no other model available to me. What I discovered several years later was that every single one of the rules they followed were rules that had been very intensely thought through by these very smart guys. They weren’t random chance.”

“(Munger) told me that it’s very important for an investor to have people to talk to….(and)…When god tells you to do something, you do it.”

Just do it when you come to an interesting fork in the road or when you trust someone completely.

…

3/ Do your own work. Pabrai doesn’t have an analyst, advice he got from, you guessed it, Buffett and Munger.

“It is a huge advantage not to have an investment team,” Pabrai said, “Investing is not a team sport, it should never be a team sport.”

Why doesn’t it work? In part, because other people’s ideas fall outside your circle of competence. Pabrai explains that an analyst could come up with the best idea in the world, but if you don’t understand it, you won’t act on it. Analysts can also get boxed into an industry. That doesn’t work either says Pabrai. The ideal question is “where should we put our money in the entire universe of possibilities.”

…

4/ Argue well. You don’t have to argue; quarreling, disagreeing, and squabbling all work too. They key is a pursuit of the truth. “What you do by talking to people not on your payroll,” says Pabrai, “is you get rid of vested interest and conflicts.” Norms, politics, and individual incentives are gone.

Bill Belichick has worked hard to create an environment like this. His assistant coaches are actually graded on coming up with good new ideas. Belichick also listens to his players, assistant coaches, and (what does he do here again?) Ernie Adams.

Good arguments “help round the corners,” said Wilbur Wright. Geniuses argue too.

…

5/ See it to believe it. Pabrai thought he was dumb. Well, actually, he said he was 67th out of 70 in his third grade and there were probably three carrots in the group. Pabrai needed a catalyst. Lucky for him, one was coming.

Pabrai moved to a new and better school (no carrots there). He took an intelligence test and scored at the top.

This created some cognitive dissonance. How does someone not smart get a smart score? Pabrai went to the test administrators, and was like, ‘umm, you know I’m not smart, right?’ They said to him, ‘no, actually you’re very smart, maybe brilliant.’

This was a big moment. “I felt like after that two-minute conversation in ninth grade I was like Seabiscuit. I just took off.”

Richard Thaler had this see-it-to-believe-it moment when he read Daniel Kahneman’s paper. Ezra Klein had this when he read Matt Yglesias. Judd Apatow had it when he saw Steve Martin.

A recent example – to me – is told in the book The Song of the Dodo where David Quammen writes that Charles Lyell, Charles Darwin, and Alfred Russell Wallace were having this see-it-to-believe-it moment together. They were peeking at evolution by natural selection. A notion that, Quammen writes, “was going to incite a shitstorm of resentment in Victoria’s England.”

We all could use a nudge where we go ‘holy shit, I didn’t know this was possible.’ In fact, it might be necessary.

…

6/ Does the glove fit? Okay. You’re excited. You’d never heard of Pabrai, but this sounds like someone you’d like to emulate. What’s next?

“The first question investor need to ask themselves is ‘Does the glove fit?’… after you read an annual report you have to ask yourself, ‘you know, I spent two hours reading that, would I have preferred doing that or watching a Star Wars movie?’…you have to ask what type of activities give you the greatest satisfaction.”

If something takes a long time there better be good rewards for it. Steven Johnson talked with James Altucher and said that he has high motivation to play music, but no ambition. That’s what it feels like when the glove fits.

Pabrai has – if I’m reading the tea leaves correctly – a very philosophical approach. If you’re going to spend your life doing something and you have some autonomy over what that thing is, choose something you enjoy.

We’ve seen this before, it goes by different names. Love the grind like Gary Vaynerchuk. Be relentless like Bezos, Belichick, and Buffett. Tinker like Phil Knight and Peter Thiel.

Warning: Tangent ahead.

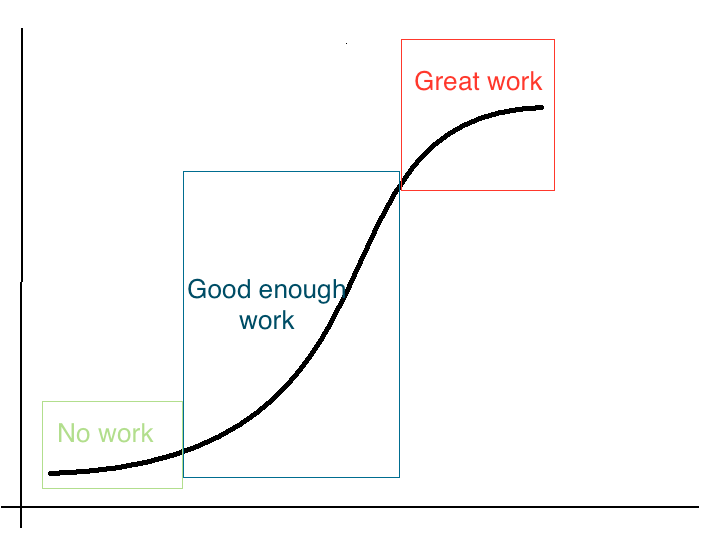

I’ve been thinking about this as; no work, good enough work, and great work.

My theory is that many “good enough” skills are achievable. Take cooking. Buy Mark Bittman’s cookbook and learn the basics. That’s good enough and it’s not that difficult. If you want to move to great work, well then, it’s off to culinary school and years of hard work.

Good enough is attainable. Guitar? Four chords. Fitness? Walk more, sit less. Investing? Index, minimize costs.

Great work is hard. We get off the s-curve ascent and face the slog known as “diminishing returns.” This is roll-up-our-sleeves, put-our-heads-down, and dig in for the long-term territory because that’s the only point where results show up. Delta only shows up over time. This is why Pabrai wants to know if the glove fits. To get to great work requires a lot of energy, effort, and time. Great work has a high opportunity cost.

It’s why we say here that you can actively invest/be an entrepreneur, but you can’t do either of those things AND have a hobby, be a soccer coach for your kids, and show up to dinner. A lot of things in life are worth a little work for big returns. The great work though, those pursuits are more limited.

[/Tangent end]

…

7/ Decentralized command. Berkshire Hathaway owns stock in Southwest Airlines. This makes total sense. Here’s the CNBC synopsis of how Buffett feels about airline stocks:

He called the US Airways investment a mistake in almost every annual letter from 1989 to 1996…. ‘if a farsighted capitalist had been present at Kitty Hawk, he would have done his successors a huge favor by shooting Orville down.'”

Wait, this makes no sense. How did this Berkshire end up invested in airlines?

The answer is decentralized command. “I think this is a good example of how Warren only selects the manager and does not interfere with what they do,” says Pabrai. Buffett knows he can’t make every decision, so he creates smaller units that can make better decisions.

Jocko Willink has articulated how the military is organized like this. Amazon calls them “two pizza teams.” Andy Grove wrote about it too. Need more?

“Perot later told Fortune magazine, “I come from an environment where if you see a snake, you kill it. At GM, if you see a snake, the first thing you do is go hire a consultant on snakes. Then you get a committee on snakes, and then you discuss it for a couple of years. The most likely course of action is—nothing. You figure, the snake hasn’t bitten anybody yet, so you just let him crawl around on the factory floor. We need to build an environment where the first guy who sees the snake kills it.” – Jeff Gramm

“Hire the best people you can and leave them alone.” Tom Murphy

“One reason, I think, is that most other companies don’t really understand the concept or its scope and limitations, while many others are loath to grant the freedom and independence from management control that really are necessary ingredients for running a successful Skunk Works enterprise.” – Ben Rich

…

8/ How to learn from mistakes. “First of all, mistakes are a blessing. Adversity is a blessing.” Pabrai goes on to paraphrase Marcus Aurelius, noting that to have misfortune and prevail is good fortune. “We don’t learn when we do well.”

It’s football season, so in that spirit:

Pabrai points out that this is nice to say, hard to do. “The lessons don’t sink in very well if they are other people’s mistakes. It’s unfortunate. This is one of Munger’s and Buffett’s great strengths, they are really good at learning from others mistakes, so they try to avoid most of them…Learning from other people’s mistakes is so much cheaper.”

Okay, learn from others, got it. What else?

Don’t learn too much from others.

…

9/ Alternatives to school. When asked about books, Pabrai says that Poor Charlie’s Almanac, “(is) a book that I try to re-read every year and every year when I re-read it, I find brand new things that I swear were never in the book before, someone just put them in there…That one book, in my opinion, is better than a college degree.”

Better than a college degree! Why!? Because college has a huge opportunity cost (but also a potentially huge payout).

I could have been more efficient in my time and money budget in college. sigh (and graduate school)

College – and especially graduate school – isn’t always a better option. Failed start-up founders consistently pointed out that they learned a hell of a lot. David Chang eschewed graduate school in favor of opening a restaurant. Elizabeth Gilbert, Tim Ferriss, and Seth Klarman (“I learned an enormous amount there (Mutual Shares), probably more than in my subsequent two years of business school.”) note the value in non-college learning.

What college does well is provide a structure for learning. Patrick O’Shaughnessy said, “Almost everything I learned in college you can go read and do it for ten cents at the library.” Joel Greenblatt said to mix in the WSJ and you’ll be okay. The question is, will you?

…

Thanks for reading. Despite the length there were some things I left out so if you made it this far you’ll like the podcast.

[…] listen, read, and pay attention to what is going on but you must “do your own work.” Mohnish Pabrai said this […]

LikeLike

[…] Mohnish Pabrai said that Buffett is excellent at learning from others. That’s what Jackson and Belichick try to do. Sam Hinkie addressed this in his resignation letter. How do you balance being different with doing what works? You have to have a deep understanding. Hinkie wrote: […]

LikeLike

[…] you get to do the thing you want doesn’t mean that thing will be easy, said Brent Beshore. Mohnish Pabrai said to find something you’d do instead of watching a […]

LikeLike

[…] Mohnish Pabrai asks, what do you choose to do instead of watching a movie? We can expand it and ask, what do you choose to do? What do you engage in? Munger says, “I recommend that you engage life. If you spend all your time on how some politician wants it this way or that way and you’re sure you know what’s right – you’re on the wrong track. You want to do something every day where you’re coping with reality.” […]

LikeLike

[…] But the glove fit for Grossman. He felt for brewing like Bill Gates felt for computers or Mohnish Pabrai felt for investing. Grosman doesn’t know if this will apply to his kids. “I knew all […]

LikeLike

[…] Mohnish Pabrai said to find something you’d like to do more than going to the movies. Manoj Bhargava said to find something you like to do more than following sports. Ken Grossman put it this way: […]

LikeLike

[…] I would go in and pull the shades down because I didn’t want to work with people there.” As Mohnish Pabrai and Brian Scudamore noted, if you aren’t excited to go to work something is […]

LikeLike

[…] we combine the ideas of Mohnish Pabrai, Charlie Munger, and Cal Newport we get […]

LikeLike

[…] too. Often the revelation is, ‘Wait! That’s possible?!?!’, Both Ken Grossman and Mohnish Pabrai had moments as kids that changed the direction of their […]

LikeLike

[…] Mohnish Pabrai said that Charlie Munger suggested he do this in their first meeting. “He told me that it’s very important for an investor to have people to talk to,” and “When God tells you to do something, you do it. What you do by talking to people, not on your payroll is you get rid of vested interest and conflicts.” […]

LikeLike

[…] better than us so that we can become more like them.” That meant more time with people like Mohnish Pabrai, Warren Buffett, and Charlie […]

LikeLike

[…] Mohnish Pabrai said something similar about Southwest, “I go on a Southwest aircraft and I’m in coach and I usually find I’m happy. I’m in a happier state of mind in coach in Southwest versus business in American. Why is that? I don’t know.” […]

LikeLike