Tren Griffin (@TrenGriffin) was interviewed on the a16z podcast to promote his new book: Charlie Munger; The Complete Investor

– Remove the bad before you seize the good.

– Inversion.

– Mental models.

– 2 types of people, moat finders and moat builders.

– How to apply these ideas.

Remove the bad before you seize the good.

Sometimes, says Griffin, we get tripped up with prediction. Rather than choose something, it’s helpful to eliminate something first. “Knowing what you don’t know is really valuable too,” he says. If you don’t know what escargot is, you may want to avoid eating it at a restaurant. Similarly, if you don’t know how a business earns its money, you may want to avoid investing in that business.

This is the big idea of his book, Griffin says, be smart by not being dumb. One way to do this is to remove the bad before you seize the good.

Right now (Autumn, 2015) there are a lot of NFL suicide pools. A suicide pool is one where each week contestants pick the winner of one game. The catch is that no one pick the same team twice. If you choose the Packers in week 1, you can’t pick them again later in the year.

Most people approach the pool by ruling out some games before making a prediction. They’ll consider 4 or 5 games to be too close, and choose from the remaining options. They won’t make a prediction until they have avoided the worst options.

We can do this in our own lives. Griffin says Charlie Munger uses an approach like this. Munger will first think of an answer, then try to rule out why it doesn’t work. Munger will shine different logical mistakes on a situation to see any apply. Others have suggested this too.

- Jason Zweig says to follow contrarians on Twitter to derail your confirmation bias.

- Michael Lombardi says that they remove NFL players that don’t fit rather than choose ones that do.

- Chris Sacca has knockout questions that if an entrepreneur doesn’t get right, he doesn’t get funded.

- Mark Cuban sees hindsight bias in fans when they look at past trades.

If we can apply classic mistakes to potential situations we can start to make better decisions.

Sometimes the mistakes are difficult to see and we need to look at the problem a new way. We need to invert.

Inversion

This is one of my favorite ideas from Charlie Munger, and Griffin explains it this way. “We can look forward and backward at a problem.” Giffin gives the examples from our lives. If you want to have a good spouse, be a good spouse. If you want to have good kids, be someone who deserves good kids. If you want to be happy, avoid what makes you miserable.

Inversion works in business too and it’s what revealed the answer In Michael Lewis’s book Flash Boys

The problem in that in 2008 High Frequency Traders were outrunning orders to other exchanges and driving up prices. We don’t need to dive into the market nuances to explain this, let’s plan a party instead instead.

Imagine that you want to have a party for your parents 30th wedding anniversary. You go to buy flowers and pick some arrangements to be delivered that weekend. While there, you ask where you might rent some tables. The florist tells you that the store across town has what you need.

But while you’re there, Harry Franklin Thomas overhears this, races across town ahead of you and rents the very last tables.

Soon you show up and Harry Franklin Thomas offers to rent his table to you. For a bit more than he paid, but you don’t know that. None the wiser you get the tables.

That was the problem, (simply put) of the stock market. Oh, and one more thing, no one knew it.

Until in 2008 a group of bankers discovered what was going on. They wondered, how can we outwit Harry Franklin Thomas? The secret wasn’t to drive across town faster than him. That was an arms race they couldn’t win.

No, the secret was a head start. If Harry Franklin Thomas heard your conversation with the florist, but delayed, he couldn’t outrun you. Once he hear the message it it would be too late because you had a head start across town.

The question wasn’t, “how do we get faster?” The question was inverted, “How do we make them slower?” Lewis writes:

“Allen wrote a program—this one took him a couple of days—that built delays into the orders Brad sent to exchanges that were faster to get to, so that they arrived at exactly the same time as they did at the exchanges that were slower to get to. “It was counterintuitive,” says Park. ‘Because everyone was telling us it was all about faster. We had to go faster. And we were slowing it down.’”

Inversion isn’t easy to figure out how to do. On the podcast Michael Copeland (@MVC) compares it to being “Spock like.” Griffin says that while that might be true for individuals, diverse teams can invert more easily. Diversity of interests, skills, opinions, and experiences all lead to something where the whole is greater than the sum of its parts. It’s why, Giffin says, that Silicon Valley is so interesting.

Individuals aren’t out of luck though. Mental models can be the diversity of thought we need.

What is a mental model?

“A mental model,” says Griffin, “is a way of looking at the world.” It’s applying the ideas of mathematics, physics, psychology, biology, architecture, philosophy, or literature to a problem. But they don’t need to be complicated. “I only bet on two things,” Gary Vaynerchuk says, “do I personally believe in this or do I believe so much in the entrepreneur?” Vaynerchuk favors investments understands or entrepreneurs who have had success before. That’s his mental model.

It’s the multiple model approach a problem, says Giffin, that will lead to answers you otherwise wouldn’t find. But these answers are uncommon.

An early inspiration for Warren Buffett and Charlie Munger was Benjamin Graham’s book, The Intelligent Investor

Graham is saying that we should first “remove the bad before you seize the good.” This doesn’t seem all that helpful though. You need to find something and act on it. Maybe. As Barry Ritholtz likes to say, “don’t just do something, sit there.”

What Graham advocates, Munger applies, and Griffin summarizes is the need to wait until the moment is right. You don’t want to chase opportunities unless they are very good. Griffin says this happened in Harvard Square when Bill Gates and Paul Allen realized Gates had to drop out of school to start Microsoft.

Okay, then how do we create a mental model?

How do you build a mental model?

Read. Read. Read. All of the successful people he’s met, says Griffin, “are inquiring and they read.”

We’ve heard this many times but successful people read a lot. If you want to get started reading there are two consistent strategies that hyper readers share.

- Don’t be afraid to stop a book. “We’re brought up believing that books are sacred,” Naval Ravikant told Tim Ferriss. But sometimes you just need to stop reading them. Tyler Cowen suggests this too, noting that life’s too short to read something you don’t enjoy.

- Read widely. Find a topic that interests you and dive into that. David Heinemeier Hansson has said that he will stop working on a project that doesn’t interest him in favor for another. Why? He figures that the productivity boost he’ll get from working on something he enjoys will pay off. In reading we can do the same thing.

The goal, says Giffin, is to create many positions from which you can understand a problem. You want to be able to recognize patterns as they arrive. One problem of education, he says, is the specialization and focus on formulas.

Formulas are good, but are only one of many models. In his book, Filters Against Folly, Hardin suggests we look at situations through three filters (models): numerate, literate, and ecolate. Hardin writes:

“In summary, the three filters operate through these particular questions: Literacy:what are the words? Numeracy:What are the numbers? Ecolacy: And then what? No one filter by itself is adequate for understanding the world and predicting the consequences of our actions. We must learn to use all three.”

Formulas are one part of the picture and like other models have weaknesses. Here are two:

- You focus on the trees and forget about the forest.

Formulas can be too specific and lead to the wrong focus. When Michael Lombardi talked about a team being able to “play right or left handed,” this is what he was spoke to. The whole needs to be greater than the sum of the parts, as a forest is greater than the sum of the trees.

Formulas can also be too reductionist in nature. We can call see in multivitamins. Why doesn’t a perfect little capsule provide the nutrients we need? Why don’t we eat food like The Jetsons?

Michael Pollan writes that to study things we need to reduce them, but in actually eating them, we need to wait a moment.

So if you’re a nutritional scientist, you do the only thing you can do, given the tools at your disposal: break the thing down into its component parts and study those one by one, even if that means ignoring complex interactions and contexts, as well as the fact that the whole may be more than, or just different from, the sum of its parts. This is what we mean by reductionist science.

Scientific reductionism is an undeniably powerful tool, but it can mislead us too, especially when applied to something as complex as, on the one side, a food, and on the other, a human eater.

This the “multivitamin” or “Lollapalooza” effect. Good situations, says Griffin, are like the music festival, greater than the sum of their parts.

- Models can have tail risks.

Tail risks are those extreme situations where something happens that we don’t expect. When Long Term Capital Management made their convergence bets, they ignored the tail risks. From When Genius Failed

“But Black-Scholes (the formula the traders built their theory on) makes a very key assumption: that the volatility of a security is constant. To say that the value of an option to buy IBM depends on its volatility is meaningless unless you can agree on what its volatility is. Therefore, the professors treated the volatility of a security like an inherent, unchanging trait. You have blue eyes; IMB has a volatility of X.”

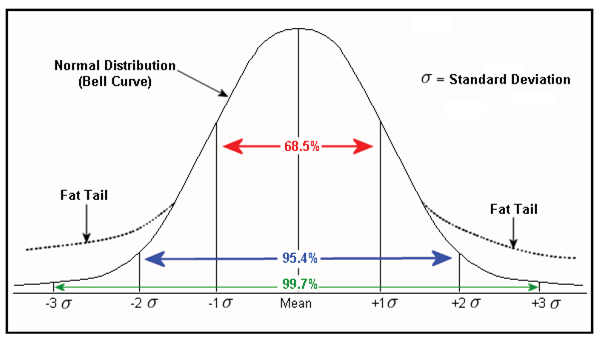

In a normal bell curve (non-dotted line) we can see that the tails thin out. That’s what LTCM thought they were investing in. Height follows a bell curve. Blood pressure follows a bell curve. The stock market follows a bell curve, kinda.

Bell curves work best over time and when things are random – but markets don’t perpetually satisfy those criteria. “Markets can remain irrational longer than you can remain solvent” (Keynes) and markets aren’t always random.

Markets have things like High Frequency Traders or activist investors or government intercessions. These things disrupt random models to create sticky situations for precarious predictions. LTCM got caught in one of those. Russian bonds declined in prices and hedge funds lost money. Those funds sold other holdings to limit their losses, which caused LTCM’s position in those holdings to decline in value. Other firms sold too, LTCM’s position worsened even more.

How then do we avoid all this? If formulas are one form of a mental model, but even it is fallible what do we do?

Read widely. If we know about formulas, that’s good. If we know about formulas and the history of the stock market that’s even better. If we know about formulas, the history of the stock market, and the biological foundations of greed that’s even better yet.

Giffin says that Munger’s hero was Franklin and that he loves the independence to read widely. Part of this reading has brought about a humility. “The more you know,” says Griffin, “the more humble you should be.” That may be the most important model of all.

Two types of people: moat builders and moat finders

“One of the great contrasts in life,” says Giffin, “is between people who know a moat when they see it and people who know how build one out of nothing.”

Munger and Buffett are the former, they know how to find a valuable moat. Bill Gates and Mark Zuckerberg are the latter, they know how to create one out of nothing.

The important part is to know which type of person you are. Gretchen Rubin tried to figure this out when she began her book about habits. Some she articulates include; are you an abstainer or moderator, a sprinter or marathoner, a starter or a finisher. If you know yourself, Rubin reasons, you’ll be your best self.

So, are you a moat builder or moat finder?

What is a moat?

A moat is a competitive advantage. It’s also interesting that Munger calls it a “moat” rather than “competitive advantage.” Sanjay Bakshi said that he thinks the reason is because quips like this call to mind more than the just technical definition. Bakshi says that Munger likes to have these names to explain things. We used “boiling frog syndrome” here to talk about the change in jobs.

Rather than explain something I don’t know, go to Griffin’s page to understand moats. We’ll look at just one kind of moat; brands.

Scott Galloway spoke about brands and identified five things that constitute a good brand;

- Truly differentiated products and intellectual property. You can open another frozen yogurt store but, you can’t create a Google competitor.

- Visionary capital. It costs them less to borrow.

- Control of the end user (vertical integration). No one else messes things up in the last mile.

- Vanity. People want to be seen with the product.

- Maternal. These places are all great places to work.

Both Griffin and Galloway conclude that they think Nike is a good brand, in part because it does these things well. But brands are a squisher type of moat.

In a blind taste test people don’t prefer Coke to Pepsi, but their buying habits do. What gives?

People have what Richard Thaler calls, “transaction utility.” They get enjoyment from being a type of buyer. How often have you heard of someone “getting a deal”? That person liked the item and “getting a deal.” Both were parts of the transaction for them.

Seth Godin says that you can see the same thing with headphones. People like to be seen wearing a certain pair of headphones, in his example Beats. But that’s not all. When he talks to Brian Koppelman he notes that Koppelman doesn’t wear Beats. He wears Sennheiser. Godin proposes that people also like to think of themselves as the type of person who knows why to buy Sennheiser rather than Beats.

If you’re keeping score at home we have three aspects that can be part of a brand’s moat.

- The “I like a good deal” sort who find transaction utility.

- The “I like to be seen with this” sort. I’ve always suspected this is why Apple their headphones white.

- The “I like you to notice that I’m smart/cool/wealthy enough to differentiate” and choose this brand. Godin’s hypothesize about Koppelman’s headphones.

Brands, as a moat, are kind of squishy. People change, and this moat is built on people not changing.

How to apply these ideas

Step 1: for the things you don’t, won’t, or can’t invest time in, make the chances of failure as minimal as possible. “If you can’t read the sections on moats (in his book),” says Griffin, you should just buy an index fund for your retirement.

Step 1: for the things you don’t, won’t, or can’t invest time in, make the chances of failure as minimal as possible. “If you can’t read the sections on moats (in his book),” says Griffin, you should just buy an index fund for your retirement.

Learning about moats is like an end-of-level boss that you need to defeat to move on. If you can’t get past level 1 (read and understand about moats) then you can’t go on to level 2.

Step 2: for the things you do care about, keep learning. Realize that knowledge isn’t perfect and everyone makes mistakes. Daniel Kahneman won the nobel prize for his work on ideas like the planning fallacy (that we underestimate the time needed and results from a project) yet he still fell for the planning fallacy. (See the Jason Zweig post for the full story).

Let’s finish then with the advice of Nassim Taleb, writing in Fooled by Randomness

“My lesson from (George) Soros is to start every meeting at my boutique by convincing everyone that we are a bunch of idiots who know nothing and are mistake-prone, but happen to be endowed with the rare privilege of knowing it.

–

Thanks for reading, I’m @MikeDariano if you’d like to connect on Twitter. If you like these posts and think this sort of synthesizing, thinking, or summarizing is a good fit for your business, get in touch.

I also send out a monthly email with the books I’m reading.

//

Updates: The first version of this article misspelled “Hasson” as “Hason”.

[…] Tren Griffin […]

LikeLike

[…] Tren Griffin […]

LikeLike

[…] Tren Griffin […]

LikeLike

[…] Tren Griffin […]

LikeLike

[…] or directing class,” Rosenthal says, “you want to come at the problem from every angle.” Like Tren Griffin suggests mental models for business, Rosenthal suggests them for writing. The more filters, ideas, […]

LikeLike

[…] Tren Griffin […]

LikeLike

[…] Tren Griffin […]

LikeLike

[…] Tren Griffin […]

LikeLike

[…] Tren Griffin […]

LikeLike

[…] note: This is Part 1 of 2, and the format of this post is inspired by the posts Tren Griffin does at […]

LikeLike

[…] value of mental models has been trumpeted by many. Tren Griffin and Michael Mauboussin speak about mental models quite a bit. So does Sanjay Bakshi and Phil […]

LikeLike

[…] meta point is to understand that we have biases in our understanding. Tren Griffin pointed out that at least knowing our biases can be helpful. One of which is how we view […]

LikeLike

[…] 1: What do you believe that’s false? It’s not an easy question to answer. Tren Griffin points to the Charlie Munger quote that it’s a wasted year if we don’t change our minds about […]

LikeLike

[…] right level of reaction. Michael Mauboussin talks about the difficulties of updating our beliefs. Tren Griffin quotes Charlie Munger on it. Maria Popova notes that changing our mind (updating our beliefs, […]

LikeLike

[…] can use Twitter to get balanced conclusions. Jason Zweig, Tadas Viskanta, and Tren Griffin all suggested to generate conclusions from multiple perspectives. Twitter can be one where we […]

LikeLike

[…] been on the blog before, when he spoke on the a16z podcast about the […]

LikeLike

[…] Tren Griffin writes in his book about Munger, “Effective (Benjamin) Graham value investors are like great detectives. They are constantly looking for bottom-up clues about what has happened in the past, and more importantly, what is happening now. Graham value investors like Munger stay away from making predictions…What Munger looks for is a business that has a significant track record.” […]

LikeLike

[…] at dead startups is form of thinking called inversion that Tren Griffin and Charlie Munger both use. Rather than […]

LikeLike

[…] Charlie Munger (via Tren Griffin ) pointed us to the spectrum of things that can be counted and things that can’t be counted. […]

LikeLike

[…] Tren Griffin said that Charlie Munger gets this, choosing to invest in companies rather than start them. Naval Ravikant has taken the physical and philosophical health rather than career angles to know himself. […]

LikeLike

[…] Tren Griffin said that Charlie Munger thinks, “business school should be taught from more of a historical case format, that you learn from pattern recognition and in order to learn from pattern recognition you have to see a lot of examples.” […]

LikeLike

[…] Tren Griffin wrote that “what (Charlie) Munger looks for is a business that has a significant track record.” […]

LikeLike

[…] Tren Griffin pointed out the advantage of pattern recognition, stories, and history. “Business school should be taught from more of a historical case format,” Charlie Munger believes, Griffin pointed out, “that you learn from pattern recognition and in order to learn from pattern recognition you have to see a lot of examples.” […]

LikeLike

[…] Tren Griffin wrote about pattern recognition: […]

LikeLike

[…] Butterfly Effect is a non-predictive model. That’s helpful too, said, Tren Griffin. Knowing what we don’t know can create limits on what we try to […]

LikeLike

[…] works at many levels too. Tren Griffin said, want to have a good spouse? Then be a good […]

LikeLike

[…] layer between the c-suite and the customer is a layer where filters naturally happen. As Tren Griffin wrote, “as a manger you can’t review everything.” The fact that you have middle managers is […]

LikeLike

[…] Find the source. Tren Griffin writes the wonderful 251q.com blog had a post about Grove. Some of the quotes sounded interesting […]

LikeLike

[…] Tren Griffin wrote, “One trick related to passion is that you are not likely to be passionate about something you do not understand…the more you know about some topics, the more passionate you will get.” […]

LikeLike

[…] Tren Griffin said; “one of the great contrasts in life is between people who know a moat when they see it and people who know how build one out of nothing.” Weissman recognizes this too, “we don’t run these companies…if we were good at operating companies we would operate these companies, but we’re not.” […]

LikeLike

[…] is no substitute for investing, since most mistake in investing are psychological.” wrote Tren Griffin. It’s not […]

LikeLike

[…] Tren Griffin said that Charlie Munger thinks we should teach this way in school. […]

LikeLike

[…] Tren Griffin‘s post about The Success Equation I knew it was time to finally read Mauboussin’s […]

LikeLike

[…] so much was Kandanchatha’s idea about understanding something deeply by revisiting it. When Tren Griffin launced 25iqbooks.com I was kind of disappointed becuase there weren’t surprises. Patrick […]

LikeLike

[…] the beginning of Charlie Munger: The Complete Investor, Tren Griffin […]

LikeLike

[…] Rogen and Evan Goldberg say they are best at writing, so they write. Tren Griffin asks if you are a moat builder or identifier. David Chang started Momofuku because that what his […]

LikeLike

[…] and Patrick agree that people probably don’t design moats as much as they stumble into them. Tren Griffin reminds us that some build a moat (Bill Gates) and that some find a moat (Warren Buffett). In […]

LikeLike

[…] thinking is efficient and fun! Tren Griffin wrote, “looking for models that can reveal and explain mistakes so one can accumulate worldly […]

LikeLike

[…] Parrish has a great email newsletter that comes out Sunday mornings. Tren Griffin‘s comes out Friday. Patrick O’Shaughnessy‘s podcast comes out Wednesdays. The […]

LikeLike

[…] do. You need to be able to see things from another point of view. In his book about Charlie Munger, Tren Griffin comes back to the idea of detachment again and again. Munger has succeeded because he’s able […]

LikeLike

[…] is our fourth post highlighting Griffin; Tren and Munger, Tren on a16z, and Tren and his book. Thanks for […]

LikeLike

[…] to Tren Griffin for repeating the ideas of CAC and LTV so many times they’re a well-worn mental […]

LikeLike