If you invested twenty dollars a week how much money would you have?

Well, it depends. When did you start?

The start is important because the sequence matters. Let’s follow the advice from Richard Zeckhauser and think in extremes.

If things were ideal, an investor’s early years would have low (or even negative) rates of return and their later years would have high ones. Would you rather double your net worth at fifteen or fifty-one?

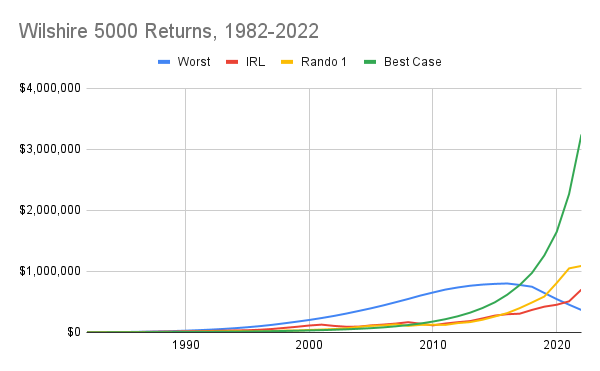

The most favorable market returns transform 30,000 into 3,200,000 after thirty years. Wild.

But the worst conditions cede only 300,000. Real-life, as often the case, is somewhere in the middle.

Each of these graphs is the actual returns of the Wilshire 5000 (16%, -5%, .01%, etc.) but arranged in different sequence. A random ordering (yellow) offers an extra 40% over real life. It’s a luck of the draw as they say.

But this isn’t a what if you invested in ___ at ___ post.

The point is to practice Maxims for Thinking Analytically. Extreme examples reframe how we understand and here we understand sequence matters.

…

We touched on this idea in the Maximizing a 401k post and considered the tradeoffs between a 401k and a 15-year mortgage too.