Supported by Greenhaven Road Capital, finding value off the beaten path.

Ed Thorpe joined Barry Ritholtz on Masters in Business to talk about his life – via book form. What an interview this one was.

…

1/ Two-jar model. Thrope has a TJM view of life. He wrote, “Chance can be thought of as the cards you are dealt in life choice is how you play them,” and explained to Ritholtz:

“And then there are things you can’t control like; who your parents were, what kind of economics circumstances you were brought up in, where you started, did you start twenty yards behind the start line or twenty yards ahead of it or right on it. People start in different places, those are card they’re dealt.”

Good decision making, noted Chris Blattman, requires good data. It’s why Judd Apatow and Joe Rogan focus on writing good jokes (how they play the cards) and not how the tickets are selling (the cards they are dealt).

Good data increases the relative weight of the skill jar scores. These data repeat. Joe Peta found that strikeouts, base on balls, and home run rates were skill jar scores for major league pitchers.

…

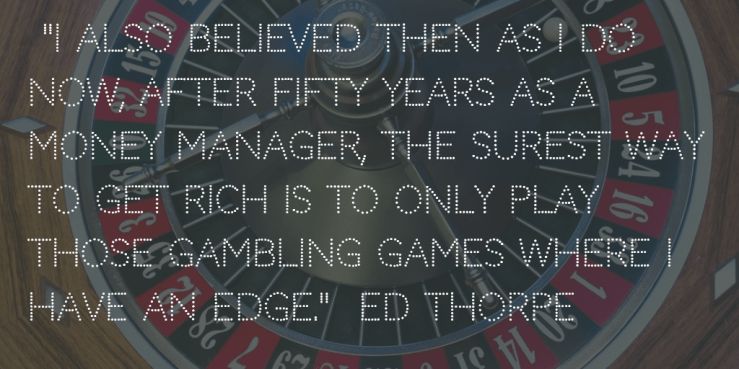

2/ Choose games with good odds (both ways). “I also believed then as I do now, after fifty years as a money manager, the surest way to get rich is to only play those gambling games where I have an edge.” Andy Rachleff started Wealthfront because he read Howard Marks and thought, how can I be non-consensus and be right. Charley Ellis said about his early work, “It was not very skillful work but compared to the competition it was fine.” For Jeremy Liew it was realizing his odds were worse as an operator than an investor.

Sometimes games can have good odds because you’re the only one playing. Thorpe said that overpriced warrants, “someone eluded the market.” Rishi Ganti told Patrick O’Shaughnessy that a market needs two buyers. If there aren’t two buyers, there is no market, if there isn’t a market there isn’t a pricing mechanism.

Whether it’s the NBA finals or investing like Charlie Munger playing in the better areas is better than not.

Then you have to figure out how much to bet. It’s hard said Thorpe:

“That was one of the early things that I learned, fortunately, how much to bet on good situations. If you bet too much you could be wiped out. If you bet too little it takes forever to make any money. There’s a happy medium in there and that was one of the things I came across quite early.”

Matt Patricia said about coaching for the Patriots, “We talk a lot that before you win you have to learn not to lose.” Seymour Schulich asked whether decision missteps would be painful or fatal.

Wilbur Wright wrote, “The man who wishes to keep at the problem long enough to really learn anything positively must not take dangerous risks. Carelessness and overconfidence are usually more dangerous than deliberately accepted risks.”

…

3/ Serendipity. Thrope found himself in Las Vegas with his wife for a “cheap vacation” and to see the roulette wheel in action. He wanted to beat roulette and needed experience in the casinos.

“I wanted to verify by close up observation that what I was doing would work. On the way I heard about a blackjack paper some statistician as written so I thought, I’ll get a little casino experience if I’m playing roulette, so I sat down at the blackjack table and played for forty minutes and I learned enough in that forty minutes that I could probably beat black jack and I went to work doing that.”

One deck blackjack was solvable! If you tracked the cards and knew if the deck was heavy (or light) in tens then there would be better odds. Not only that, but the payouts were favorable (#2).

Thorpe wrote his book – Beat the Dealer – and the advantage eroded away. Casinos changed the rules and began to deal “what they called – professor stoppers; two, four, six, or eight decks and deal them out of shoes because it’s hard to hold eight decks in your hand.”

…

4/ Rapid fire.

“Every edge has a scale limit and can only get so big.” Microcap investors like Sean Iddings and baseball bettors like Joe Peta see this too.

Thrope has a “let’s see if I can figure it out,” attitude. He has what David Salem calls “intellectual integrity.” Probably Grit too.

“Any edge in the market is limited, small, temporary, and quickly captured by the smartest or best-informed investors.” Daryl Morey had this happen with player evaluation. His alpha has eroded.

And these last two quotes were my favorites.

“Success on Wall Street was getting the most money, success for us was having the best life.”

Ritholtz asked, “How do you keep your ego in check?” after all these accomplishments. Thrope said, “All you have to do is look at all the other things people do.”

Thanks for reading, I’m mikedariano. If you don’t want to miss out on these posts, sign up for a weekly email here, http://eepurl.com/cYiwTP.