“We use quantitative methods to put together diversified portfolios that don’t blow up over time. We have technical guys who are very sophisticated, one guy was the MIT chess champion. We need these guys to balance our portfolios, but they’re not picking stocks. I pick those guys because they have no idea how to pick stocks and I don’t want to know what they think about picking stocks, that’s for our researchers.”

– Joel Greenblatt, Capital Allocators.

The JTBD of diversity within an organization is uncorrelated decisions. If we’re all thinking the same way, the expression goes, nobody is thinking.

Early in the episode with Ted Seides, Greenblatt cautioned that there’s always more correlation in a portfolio than someone expects. This is consistent with the idea that most financial issues are liquidity issues.

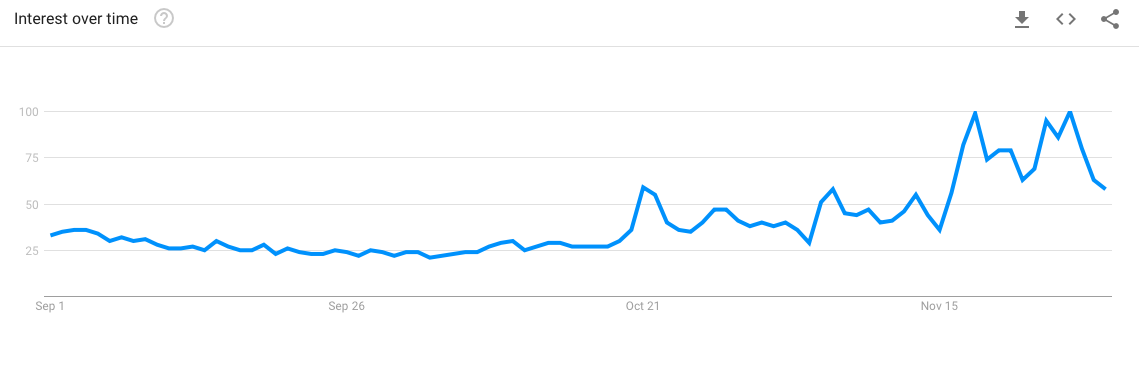

If there are 3 ways to spend your day then we should be wary about the feed, the search, and the trends. For instance, the September 1 – December 1 BTC search trends. When Coinbase emailed me “Why Bitcoin is in the News.” I thought, this might be a good time to sell.

Trends, searches, and feeds aren’t bad, but they are correlated.

The best solution to uncorrelated decision making is to use a bit of decision making advice from Rory Sutherland. When we select one at a time, we choose the average item. When we choose multiple things at a time, we choose a variety.

Rather than consider a best option then, we can consider a basket of options. With finite resources it’s hard (impossible?) not to prioritize but it does lead to new ideas.

It’s neat to hear that Greenblatt’s operation is like a newsroom: editorial and news, research and technical. Division is balance. The worst outcomes aren’t when something goes against us but when everything does.