Charlie Munger is ninety-five years old and when asked for advice his answers circle around one thing, honesty.

Honesty in education.

“My definition of being properly educated is being right when the professor is wrong. Anybody can spit back what the professor tells you, the trick is to know when he’s right and when he’s wrong.”

…

Honesty in problem-solving.

“Denial is a very stupid way to handle a problem.”

…

Honesty about limitations.

“We never had the illusion that we could just hire a bunch of bright young people and they would know more than anybody about canned soup and aerospace.”

In mapmaking, there’s always lost details. A perfect 1:1 map of France is France. So maps are scaled down to balance detail and convenience. Munger, and Warren Buffett, seek terrain they understand.

Like their famous ‘too hard pile’ – “Part of our secret is that we don’t attempt to know a lot of things.” – is full of subway maps, transit maps, museum maps and so on. They’re looking for maps where they understand what’s on the page and what’s not.

“We never thought we could get really useful information on all subjects like Jim Cramer pretends to have.”

When the right map crosses Munger’s desk he wanted to seize it.

“The whole idea of diversification when you’re looking for excellence is totally ridiculous.”

How, for example, does someone read the map of China. We have books on China but that’s only a start. We can’t ask Charlie either.

“I can’t help you, I solved my problem you’ll have to solve yours.”

“Partly because he’s (Li Lu) fishing in China and not in this over searched, overpopulated, highly competitive American market.”

…

Honesty about money. Munger said that his family’s net worth would be double if not for one mistake of omission. So what. There are more important things than money.

“We all know people that are out married, what a good decision that was for them, way important than money.”

And maybe in another life, Charlie Munger would be Mr. Charlie Munger Mustache (McMM).

“Controlling cost and living simply is the secret.”

If there’s one financial tip he’d like to pass along it’s probably to pay less.

“We handled those hands (department store, textile factor, trading stamp company) pretty well and we bought in very cheaply and success came from chaining our ways and getting into the better businesses. It isn’t that we were so good at doing things that were difficult, we were avoiding the things that were difficult.”

…

Honesty with others. Two people that came up multiple times during the two-hours were Abraham Lincoln and Li Lu, “Li Lu is the Chinese Warren Buffett. He’s very talented.” Munger admires both, in part, because of the sacrificial nature of their success. Lincoln’s stepmother taught him to read. Lu’s older brother gave up everything for him. And it’s those that might be the greatest investments we can make.

“There are a lot of ways to make money in this world,” said Brent Beshore, “but you ultimately get one life.” Venture capital is a small slice of the investment pie and VC is over-represented in the media but Jerry Neumann is a venture capitalist and one we can learn from.

Neumann likes to invest early. “I try to be the first money in and be very involved for the first couple of years. One of the ways I can be involved is helping raise the next round of capital.”

And got a fortunate start. “I started in 1997 and made a ton of money even though I didn’t know what I was doing.”

Circle round to 2019 and Neumann’s landscape of experience is worth driving through and these notes are from his 2017 podcast with Patrick O’Shaughnessy, his 2015 talk at Percolate, and his 2014 podcast with Nick Moran.

“In the past, venture capitalists would win because they would see the deals nobody else would see.”

“People have been saying deal flow is no longer a competitive advantage and that’s not entirely true but it certainly is becoming true.”

One area this advantage remains is in niches. Paul Graham noted this years ago, “our m.o. is to create new deal flow by encouraging hackers who would have gotten jobs to start their own startups instead.” Brent Beshore has done the same for ‘boring businesses’.

Inbound requests initiate because of bequests. It’s ain’t all about the Benjamins, baby. People want a something else. Expertise, experience, and connections can decrease the price and increase returns. Neumann said, “If you look at the best performing seed-stage venture funds you will find they started investing where the market price indicated a discounted price.”

Rishi Ganti said markets set prices and, “In order to get real alpha you have to avoid a price mechanism and to avoid a price mechanism you have to avoid a market.”

Neumann faces this challenge too. “So how do you win, how can you make money if the dumbest guy in the room is the one setting the price?”

Deal flow.

…

Default ‘No’.

When missing out is more important than getting in, a default answer of ‘No’ is often the best course of action.

“I can’t possibly evaluate ten pitches a day. I do respond to all of them and 80% are an immediate ‘No’. My default is ‘No’…for the 20% I read the pitch deck for, 80% of those are ‘No’.”

Neumann said he might entertain a pitch a week and always sleeps on a pitch. “If I made snap decisions I’d always say yes.” Meb Faber noted this about early-stage investing too, “At my core, I’m an optimist so everything sounds like a yes to me. Where in that world you need to start at no and get to a yes.”

…

How does Neumann invest if he mostly says ‘No’, wants to be early, and has only okay deal flow? Using his experience and the Technological Revolutions and Financial Capital theory he looks for things that kinda-sorta-mostly fit the market now but will fit wonderfully later.

Neumann said, “If people already know what they want then you’re in an existing market and selling against solutions they already have.” That’s tough. It’s like being a Jimmy Buffett wannabe in Key West.

This is why Susan Tynan got out of transportation and into displays. “When I got to Taxi Magic I thought, ‘So many smart people are competing in the category and I’ve got this category I’m so eager to make better and nobody is thinking about it.”

But it’s not enough to be different, you also have to be different and be right. Howard Marks noted, “You must learn to see thing others don’t, see things differently or do a better job of analyzing them – ideally all three.”

It’s not just having the faith and taking the step but the bridge has to be there.

This is I think where Carlotta Perez’s theory enters. The financial, cultural, and economic backdrop matters a lot. Neumann said that metallurgy, steam power, and the LLC “together meant you could build a railroad.” And, “Until the US government came in and invested a ton of money building the interstate highway system you didn’t have the society changing aspects of the automobile.”

The automobile waterfall is clear in the stories of Ray Kroc and Rich Snyder. But there’s a Facebook and iPhone example too said Brian McCullough, “I think the reason mobile didn’t take off for so many years was that there wasn’t anything for normal people to do with it. The iPhone comes out in 2007 and six months later Facebook opens registration to everybody.”

“A technological revolution starts,” explained Neumann, “when you have a bunch of innovations that come together to form a technological system.” No one articulated burgers and milkshake franchises. No one demanded Facebook. “Steve Jobs couldn’t do customer development. You can’t do customer development with markets that don’t exist.”

Circa 2018 this is/was platform businesses. GPS devices with cameras and payments are perfect for solving the transaction cost problem, and everything boils down to transaction costs said Michael Munger.

eBay happened because people had home computers, internet connections, and Beanie Babies.

Apple and Facebook coevolved, wrote McCullough, thanks “Maybe you had to have Facebook to go mainstream for the iPhone to go mainstream and vice-versa.”

But these co-evolutions are hard to pin down. Ben Horowitz said that no one ever predicts the killer app. Avi Goldfarb said the same thing about AI, we just don’t know what it’s going to do well.

What we know is that it takes different things coming together like metallurgy, steam, and the LLC! Independently they’re good, together they change the world.

But what happens once the world changes? “The goal for production capital is to fund innovations customers want.”

This is a drum we beat again and again, because (maybe) we’re in what Perez calls the “deployment age.”

Talk to your customers. Talk to your customers. Talk to your customers.

When Peter Rahal started selling homemade (RX)bars at Crossfit no one there knew they wanted a paleo friendly bar. But once they did he started collecting feedback, tweaking and trying again. “You should learn (the Lean Startup methodology) because these tools are meant for the deployment age,” said Neumann.

Ideally, a founder wants to be somewhere the competition is not. They need to be somewhere their competition isn’t, do something their competition can’t, or know something their competition doesn’t – ideally all three.

You can also invert the question. If I were in a big company, what would prevent me from competing? “In a big company, you can’t walk into your bosses office and say, ‘I don’t know what the expected value is, I don’t know how big the market is going to be.’ Nobody in their right mind would do that.”

“It’s the same thing Porter says in Five Forces if a supplier has more power than you they can abstract more of the value.” “So how do you do something where they’re not going to copy? You either have complementary assets where you have some control or you have something that’s hard to replicate.”

But everything good gets copied. Alpha erodes. Albert Wenger noted, “lots of people caught up with us and started talking about network effects, and then we started talking about finding network effects in less obvious places.” Annie Duke said poker’s been like this. And it’s why investors like Pat Dorsey look for moats.

We started noting there are many ways to make money, but also some consistencies around strategy, decision making, and markets that apply beyond venture capital. There’s also an attitude of ambition, curiosity, and wonder at the world.

In his book, A Curious Mind, Brian Grazer wrote that there are two parts to curiosity; asking the question and following up with the answer. Neumann does that too.

“What you find out when you start teaching is if you don’t understand something you can’t explain it to someone else. You read a book and you’re like, ‘I get it’ but then go and explain it to someone else and then it’s ‘I don’t get this at all.'”

Bruce Greenwald spoke in 2005 about value investing. He noted, “There is overwhelming statistical evidence that markets are not efficient.”

But finding inefficiencies is tricky. Ask, said Greenwald, “Why has God been so kind – or whoever it is who does this – as to make this opportunity available only to you?”

This is something a lot of analysts, value investors or otherwise, miss said Sonkin and Johnson. They said there are four questions investment pitches must answer; how much can I make, how much can I lose, why haven’t others grabbed this, and when will others get it?

Josh Wolfe puts it this way, we hope others agree with us, just later.

Greenwald, Sonkin and Johnson, and Wofle all want something that costs less now and more later. Usually that means it smells funky, is complicated, or unloved. “Ideally, you want to be the only one seriously studying a particular security.”

And there could be lots of reasons you get first crack at something. It could be too small. It could be the wrong category. It could have a catalyst. “Boring is your friend…people like exciting but that is not where you want to be.”

This approach works if it has support.

“But as any professional investor knows, they run up the score whether you swing or not because you’re being compared to indices.”

The organizations stakeholders are important. For investors it’s LPs. For parents it’s kids. We all have them.

“You get in trouble as an institutional money manager by significantly deviating from the performance of other institutional money managers.”

Ideally, you self select as Brent Beshore told Ted Seides, “We like to get in situations where people have educated themselves on us, people know who we are, there’s already trust built through our writings, through what we’ve talked about and they want us to buy the business. They’re coming out and seeking us.”

Once everyone is aligned, Greenwald warns investors to focus on what they know. Want to forecast returns ten years out? Good luck, said Greenwald.

“It’s about developing a circle of competence, and if their circle of competence is every industry in every country, lots of luck.”

“You want an approach to valuation that uses all the information as effectively as possible.”

That means putting more value on some things, the tangible and immediate, and less on others, the distant and intangible. Greenwald said to start with assets and current earnings and then cautiously expand from there. Pat Dorsey went to India to see what he could see and realized consumer brands were beyond his scope, noting that “We didn’t know if it was diligence-able.”

If it’s different (ideally with few eyeballs), if everyone’s aligned and if there were no big assumptions we may have a great investment.

Just hopefully not too great.

Annie Duke said the returns to poker have gone down the longer it’s been on TV. Jeff Luhnow said the moneyball advantage has dissipated. Dan Rasmussen said this happened in PE. Albert Wenger saw it in network effect businesses.

Alpha erodes.

Unless…

“Unless there is something to interfere with the process of entry, this market and earnings power value is sooner or later going to be driven to the reproduction value of the assets.”

“If you have earnings power in excess of the reproduction value of the assets, there had better be something to interfere with the process of entry.”

Can you raise prices like Harley Davidson, asked Eddy Elfenbein. Can you raise switching costs like in B2B software, asked Michael Porter. Do you have a Network effect, asked Tren Griffin.

There’s a lot in Greenwald’s presentation about DCF models (models in general). Thanks to this thread for the nudge.

I don’t think I saw any mentions in the replies to Greenwald’s “Competition Demystified”.

I disliked business books like Blue Ocean Strategy (& Shift). I thought they were baloney sandwiches between platitudes of bread. I was wrong. These kinds of books are thesauruses and dictionaries. These kinds of books give us words to talk about specific things.

Sonkin and Johnson noted that not getting ideas accepted by your boss is the equivalent of having no good ideas. Sometimes we need a thesaurus or dictionary to communicate our point.

Renée Mauborgne’s Entreleadership conversation is a communication cornicopia.

Mauborgne’s big idea is to come sail away, come sail away, sail away from thee. Like Zero to One and Howard Marks implore, we need to find hidden truths.

First, realize conditions vary and are variable.

“Industry conditions are created by firms, they don’t exist in nature, they are products of the mind.”

“Don’t focus on benchmarking the competition because the more you look to the competition the more you end up looking like the competition.”

Conditions matter but they’re malleable. Daniel Crosby said, “People tend to under-guess how much the environment impacts performance.” Podcasts and talk radio are good examples. This American Life was both a radio success and podcast success but that didn’t mean that one necessitated the other. Shows like Serial, The Daily, and Bill Simmons are all alternative models for success. Successful podcasters understand that the median’s conditions are different than those for radio.

How might an organization find hidden truths? Latent needs.

“Users can’t tell you what they need,” said Bill Burnett of Stanford, “but they can show you what they’re frustrated with.”

Modern Monopolies exist because of latent needs like selling Ty Warner‘s Beanie Babies. Twitter, eBay, and YouTube succeed because they let the customers shape the product.

“Don’t look to existing customers for insight, they’re gonna echo back, ‘Just give me more of what you’re doing for less.'”

Sam Altman advised, “You should not put anyone between the founders and the users for as long as possible.” Tiffany Zhong said, “Anyone who does stuff in product, design, engineering, or wants to start their own company should know how to talk to and interview users or potential users.”

When Paul English traveled, he kept a notebook in which he tracked what other passengers told him about their experiences. He then used those suggestions for Kayak.

Mauborgne has some helpful tools in her book like a buyer utility map that lists categories of questions. It’s all about making verbs easier to do. Running, writing, and cooking are all easier with the right tools, preparation, and knowledge. Ditto for businesses.

“Across this buyer’s experience cycle,” asked Mauborgne, “‘What’s the biggest block to simplicity for our users?'”

Often this requires a beginner’s mind.

“You want to look for people who have the ability to ask uneducated questions.”

Or a dissenters’ mind.

“A lot of companies hate the complainer but we find that the complainer is really good because if there’s anyone looking for what’s wrong in your company it’s them.”

Or someone who doesn’t see the world the same way you do. None of us think we are right about everything but few of us can say what we are wrong about.

Jerry Neuman has his IEOR 4998 students read part 1 of Psychology of Intelligence Analysis from the CIA. One section is about our sequential construction of the world. We are path dependent thinkers.

Start with the upper left image in this Gerald Fisher sequence and you see one thing past the midway point.

Start with the lower right image and you see a different version of the image past the midway point. Annie Duke cautioned, “The future we imagine is a novel reassembling of our past experiences.”

Hence the dissenters, the novices, the customers.

Mistakes accrue when we sell instead of serve.

“I think a lot of organizations are not as much in touch with their market as they think they are. They always approach it from a selling or supply point of view.”

Rob Fitzpatrick has done some excellent work on how to entrepreneur and notes that you don’t want to talk about a product’s features, you want to talk about a user’s needs. That’s the starting place. What do people need and can you serve them?

I think that’s what Renée Mauborgne wants too. Find a need yet to be met.

Once again, How I Built this with Guy Raz delivers a compelling and concrete startup story, this time with Jerry Murrell, founder of Five Guys burgers.

Patrick Doyle of Domino’s and Dave Chang embody and execute the barbelling of dining. Domino’s optimizes while Chang innovates and both demonstrate there’s more than one way to succeed in the restaurant business.

Five Guys is fast, easy, and inexpensive, all relative terms. The burger joint succeeds in a niche because it knows what job the customer hires it for. Let’s see how.

…

Murrell didn’t like school. “I was a terrible student. I didn’t like school. The nuns used to say, ‘You’re gonna end up selling hamburgers someday.'”

Entrepreneurship is for the odd duck. Marc Andreessen said about the startup founders he sees, “The kinds of people who start these companies are not normal.” Schools are linear, traditional, and mass market systems optimized for average like broadcast television at 8 p.m. on a Thursday. Murrell wanted something different.

But it took time. He sold insurance. He was a consultant. He was a financial planner. He dabbled in real estate. “My wife and I were experts at buying real high then waiting till it crashed and trying to get rid of it…I really didn’t know what I was doing. I’m just lucky that I got in the hamburger business.”

“I find it helpful to see the world as a slot machine that doesn’t ask you to put money in. All it asks is your time, focus, and energy to pull the handle over and over. A normal slot machine that requires money will bankrupt any player in the long run. But the machine that has rare yet certain payoffs, and asks for no money up front, is a guaranteed winner if you have what it takes to keep yanking until you get lucky.”

Murrell got lucky. His hometown had a great hamburger place. “Then in Ocean City Maryland, there was a place called Thrashers selling boardwalk fries. There must have been 20 places selling boardwalk fries but only one place had a long line.”

If he kept it simple this might work.

Murrell’s wife thought he was nuts. She was right. The base rates for restaurants are terrible, but then, base rates depend on what you’re optimizing for. As financial investments they’re not great, but what about experiential ones? Murrell asked his kids if they wanted to go to college with the money he’d saved for them, “They pretty much said they’d rather do something else.”

This was Dave Chang’s motive too, whose first restaurant cost $250,000, “this will be my business school,” Chang reflected. This experiential learning held for Mike Ovitz too, who wrote, “Collaborating with Pete (Peterson) and Steve (Schwarzman) and Herb Allen beat going to Harvard Business School; they taught me how to be an investment banker.” Ted Sarandos, Michael Lombardi, and Alice Waters are XMBA alumni too, choosing the curriculum of experiences.

“We said, ‘Let’s not put a lot of money into it, let’s find a place where the rent is really low, out of the way. We thought if we put it somewhere it was hard to find but if people got there we’d know we had something.” In 1986 Murrell validated his idea.

That first restaurant had a handful of part-time employees and was mostly operated by Murrell and his kids. They tinkered and kept it simple. For the fries,

“We went to Thrashers in Ocean City and looked at the potato bags. We found out they came from Rigby Idaho, a guy named Rick Miles, a small potato dealer out there and asked him.”

For the toppings, “We would not tell the kids how much we were paying for the product. We said, ‘Whatever pickles you want to put on the hamburgers.’…We were paying seven times what McDonald’s was for a hamburger bun, we were selling for four times what McDonald’s was…the thinking was the kids would pick the best product…at the end of the month, we’d look at sales, look at what we paid for the food, and raise prices to cover food costs at 30%.”

Word of mouth brought people in. Quality ingredients brought people back. Decades later RXBar would operate similarly; keeping costs low to validate an idea and then expanding selectively and limiting the stakeholders.

As the business grew, the children and Jerry’s wife all stepped up. “If it wasn’t for my wife and kids there would be no Five Guys, I didn’t build Five Guys.” Murrell had to hire for his weaknesses. One of Doyle’s lessons at Domino’s was the importance of culture and promoting from within. That doesn’t come up in Murrell’s interview but the same may be true for Five Guys. Was it better as a family business? Probably.

The company gradually grew. With time to focus, profitability from day one, and a family-business culture they were ready when it came time to sell franchises. “We had figured out the nuts and bolts of the business by then. Most franchisers start off to franchise. We started off to build a family business and we figured out how to do it right so when it came time to franchise we had a perfect system.”

Murrell and his family own approximately 75% of the business. “We took a fairly big investor when we first started franchising. They don’t interfere in our business at all. They gave us a big chunk of money. They’re entrepreneurs too and they saw something in Five Guys.” It sounds like they’re a family member, with aligned incentives. They were great stakeholders.

And of course, Murrell was lucky. “I couldn’t have done this on my own. Without my kids and wife, I’d have done nothing. We were lucky, real real lucky.”

Creative Artists Agency succeeded for all the normal reasons; they worked hard to deliver a product people valued. Their culture fit their strategy and they grew during a ‘bull market’ for movies. Specifically…

…

RON MEYER: I made myself available twenty-four hours a day, seven days a week—and this was before cell phones, e-mails, and texts. I never took a vacation where I wasn’t reachable. I didn’t love anybody more than my family, but I did give more attention to my clients.

Marcus Lemonis noted this too, “To be a business owner it’s not a glamorous job. It requires you to make a lot of personal sacrifices. If you want to meet a business owner with a great home life and a great life balance — they’re probably bs-ing you a little bit.”

People with good balance understand their tradeoffs. People with poor balance don’t know there are tradeoffs to be made.

…

SANDY CLIMAN: The entertainment industry is full of complex characters who have tremendously strong qualities as well as humongous flaws. For me, the goal has always been to study good qualities in order to learn what to do, and equally important, to study negative qualities to learn what not to do.

Inversion, said Charlie Munger, is “unbelievably useful.” Sam Hinkie suggested inverting the hiring question, instead of asking if they should work for you, ask if you should work for them. Stewart Butterfield said he learned a lot at Yahoo, some of which was what not to do.

…

The most persuasive ideas are the ones we – think we – come up with on our own. Jocko Willink calls this the ‘indirect approach’ and it was common at CAA.

PAULA WAGNER: I said, “I think it should be Tom Cruise,” and everybody went, “Whaaaaaaaaat?” Except Mike. He looked at me and said, “You do, do you? Hmm . . . interesting.” Then Dustin wanted to meet with Tom, so I said to Tom, “I have this crazy idea.” Others will probably say Tom was their idea and it probably “was,” because the art of agenting is to let clients have the great idea.

Phil Jackson wrote, “One thing I’ve learned as a coach is that you can’t force your will on people. If you want them to act differently, you need to inspire them to change themselves.” At CAA this wasn’t infrequent and led to some interesting what-ifs, like if it wasn’t Cruise and Hoffman in Rain Man. Another was that Bad Boys was written for Jon Lovitz and Dana Carvey.

…

Mohnish Pabrai asked a group of college students if they were willing to read 10Ks instead of seeing a new movie over the weekend. If they were, he said, they might end up as good investors. Michael Ovitz had a similar conversation with Magic Johnson.

MAGIC JOHNSON: Then he asked me, “Do you read the newspaper every day?” I said, “Yes.” He said, “What section do you read first?” I told him the sports section, and he said, “Wrong answer. It’s gotta be the business section.” He said, “This is what I’m going to do. I’m going to test you to see if you really want to be a businessman, I’m going to give you all of these business journals to read, and after you do, we’ll discuss them. Then I’ll know whether I want to represent you or not.” So he gave me a hard homework assignment, I came back and he asked me questions, and I answered them. After that, he decided to represent me.

Josh Wolfe told Shane Parrish, “On Sundays when my peers were watching American football I would be reading and learning something.” When Tyler Cowen was asked how many hours a day he devotes to reading and writing he replied, “All of them.”

…

JIM COULTER: One of the challenges in the investment business is what I’ll call uncommon wisdom. Common wisdom is what people think about a situation; it’s usually not that valuable because it’s something everybody sees. What is valuable is if you find uncommon wisdom, which is where you see something that the rest of the world sees one way and you see a different way.

This is why Peter Thiel believes competition is idiotic. This is why analytics has risen in sports, and why people like Andrew McAfee warn against HiPPOs.

Something about today will be different tomorrow and the rewards go to the people who dance to that delta.

…

Another reason CAA succeed was the culture. In 2014 Ron Meyer said, “I always think it’s about people first. You have to have the right people in place and if you have the right people in place you have to have the right culture in place and that means making it a place people want to come to work.”

Bill Belichick agrees that culture starts with hiring the right types of people, “A big part is the selection process. If you select people that aren’t going to be able to adjust to the culture you’re going to be swimming upstream.” Richard Lovett recalled this interview with Meyer.

“Look, here’s what’s going to happen. You are going to be dying to go out with a girl. You’ve been after her and trying to convince her to go out with you, and she’s going to finally agree to go out with you. Then ten minutes before you leave for the date, I’m going to call you and tell you you’ve got to pick up a script for me or do something else, and you’re going to have to call her and cancel the date. That’s this job.”

…

In the podcast tour for his book, The Messy Marketplace, Brent Beshore said his company looks for ongoing concerns, not hustles where “if that person gets hit by a bus, I mean the entire company implodes within a short period of time.”

BILL HABER: For any agent, the minute you become more important than your client, your company is finished, because an agent is never himself or herself—there’s no such thing as Ron Meyer; there is only Farrah Fawcett. The minute it becomes Ron Meyer and not Farrah Fawcett, it’s not a company anymore. The nature of the agency business is you represent other people. It is never about you.

Cash flow, marketing, branding, sales, culture, communications, strategy, and more. It takes a lot to run a successful business. CAA did that and did it well. Thanks for reading.

Jerry Neumann uses Rob Fitzpatrick’s book, The Mom Test in his Spring 2019 class. Spring from there, we’ll work our way through a number of talks and interviews Fitzpatrick has given about his 2013 book.

“It’s an incredible time to be a learner, I remember when I was young and it was very good, but I always felt like ‘I gotta get into this more, I want to understand it better.’ Today, the videos and courses that are online with the very best professors is phenomenal.”

…

I was excited to learn from Fitzpatrick because one of the lessons of failed startups is poor feedback. Founders would scratch their own itch or eat their own dog food to no avail. Scott Norton did not and said, about their first tasting session for a new line of ketchup, “We knew if we had one and invited all our friends they would be ‘this is amazing.'”

Fitzpatrick said, “The reason I call it the mom test is because you ask questions where even your mom couldn’t lie to you.”

Fitzpatrick’s idea boils down to asking before building. Once we have A THING and present it to A PERSON all of our social NORMS kick in. Fitzpatrick said about his mistakes, “I was essentially asking for compliments and opinions rather than getting real data, real evidence, and real commitments to purchase.”

Instead, he preaches an iterative approach with limited stakeholders. This, he said, is why college students are entrepreneurship cockroaches, “They can keep trying dumb stuff until something works.” College students don’t have mortgages or families or reputations to maintain. They have few stakeholders.

Stakeholders mean commitments which reduce time and opportunity for solving problems. Sam Altman advises founders they get one other big thing – family, hobby, sport – besides their startup.

Fitzpatrick gives permission to stay small. “The temptation to look big makes you more fragile.” And reminds founders that smaller means agile, “big companies can’t innovate because their mistakes would be too expensive.”

This is the entrepreneur’s advantage.

Think about buying from an entrepreneur, it’s usually a terrible choice on some dimensions like size, permanence, and resources. But, “The reason they buy from a startup is that you’re doing something to make their life better in a way that no one else is.”

Much like IDEO, Fitzpatrick suggests starting with the customer’s actions. Look at what they do, not what they say.

Ask them about their life, not your product.

Ask them about the past, not the future.

Ask them and then listen, don’t talk.

This is all very cheap, it only takes time and not even full time. Consider making meetings and taking lunches, after work, or on the weekends. “Nothing is expensive until growth.” And don’t aim for growth until after people love it.

Then scale might come, and along with it a whole new set of responsibilities like lawyers, investors, and a team. Those are all further stakeholders. Don’t forget A rounds lead to B rounds and on down the line, “Being committed to fundraising brings a lot of extra admin tasks.”

That’s the scaled startup path and Fitzpatrick said that was all he knew early on because it’s all the media covered. But there are smaller startups too “No one writes about this in the press because it’s not a dramatic story.”

Bootstrappers pull money through time. “The main idea criteria is that someone will pay you money quickly, that’s it.” One way to do this is like how Peter Rahal did it with RXBAR.

Direct to consumer has very generous payment terms, immediate.

Being small also lets founders talk to their customers. Fitzpatrick said, “If you do a survey it gives you data you can put in a pie chart but you lose the depth of it.”

Quantitative data works for large organizations because of dapper decision desires, everyone wants to look logical. “It’s difficult to justify making decisions on that (conversational) data because it’s not statistically significant and it doesn’t feel rigorous but I’d much rather make a decision on a small amount of truthful data than a big amount of superficial data.”

Grant McCracken articulated the same problem.

“When a senior manager says, ‘Fine, that’s what you think, where are the numbers?’ And the best we can do is say, ‘Just trust us.’ It’s like, yeah right, ‘I’m not trusting my career, my children’s opportunity to go to college on your impression. Where’s the data?’ By data they don’t mean, I did an ethnography in someone’s kitchen. They mean, please could I have some numbers.”

This is why Paul Sonkin and Paul Johnson wrote the book Pitch the Perfect Investment, to help analysts understand the local logical of their managers.

Within organizations, there’s the decision but also how the decision appears.

And as groups grow, more people move away from the customer. They lose what McCracken calls “kitchen table data” or what Tricia Wang calls ‘dumpling stand data’. Larger organizations need to create ways for everyone to have a customer touchpoint. Kayak had a service phone everyone answered. RXBAR did too. Fitzpatrick said that some companies have their engineers ask one or two follow on questions about use when they are working on bug tickets and others have Friday parties users are invited to.

The goal is to reduce biases. The Mom Test is about reducing our bias toward kindness. “It’s not enough to talk to them,” said Fitzpatrick, “you have to talk to them properly.” How so? “If you can meet them in a cafe rather than an office you’re immediately going to get more honest feedback.”

Scott Belsky spoke with Debbie Millman about his career at Adobe, in VC, and writing The Messy Middle.

More than work. Belsky said he learned a lot from his grandfather, “things I wanted to emulate but not emulate as well.” For instance, “I think he struggled after the loss (sale) of that (his) company.”

Work keeps at bay three great evils; boredom, vice, and need concluded Voltaire. Michael Ovitz paid his dad’s employer to keep his dad employed. This was part of the warning Brynjolfsson and McAfee issued in their talks too. There’s more to work than work.

School. “Traditional schooling first failed us when it taught us to stay between the lines.” Schools reward ‘the one right answer. That’s fine for some things but less great for others. We’ve looked at how IDEO embraces a different model. We’ve also seen examples like Jerry Murrell, Peter Rahal, and Martine Rothblatt who demonstrate that entrepreneurial excellence doesn’t always fit in at school.

School, like other tools, is great for some things and less great for others. Our mistakes arrive thinking school is always the answer, like the hammer sees every problem as a nail.

Ignorant enough. “None of us knew what we were doing, but we shared a tremendous amount of initiative that overcompensated for our lack of experience.”

Enthusiasm, naivete, and optimism are essential for entrepreneurs. Sam Walton wrote, that it was a blessing to “be so green and ignorant” when he started in retail.

Communicate well. “To me, design was almost like a cheat to get something done better.” “The (CIA) team I was asked to speak with was the team that merchandises information to people in the field. They had so much information that they wanted people to pay attention to but if they don’t use design practices no one is going to look at it.”

Belsky faced the same problem baseball teams and basketball teams face. How do you communicate data to practioners? Daryl Morey and Jeff Luhnow have some ideas too.

Aha moments “This (how disorganized the creative world was) was the frustration that inspired Behance.” Glitches in the matrix are moments to pause and ask how something could be better. Keith Rabois said, “Anomalies are giving you hints for things you don’t understand; they’re an opportunity to find a paradigm shift.”

Follow your curiosity, wrote Brian Grazer. Scratch your own itch, but also ask customers if they face those moments too.

Does the glove fit? “The exit scenario (for Behance) never came up. We loved what we were doing.” Millman added, “If you really love what you’re doing it’s just part of your overall life.”

Jobs aren’t perfect but they can be fulfilling. Josh Wolfe said, “On Sundays when my peers were watching American football I would be reading and learning something.” Belsky said, “The competitive advantage is doing work no one wants to do.”

That’s worked for James Higgins, “When you go down market there is a premium associated with rolling up your sleeves, and getting in the weeds and making things happen. That process is something we really enjoy.”

**Be different enough now, be right enough later. “Entrepreneurship is about identifying edges that will someday become the center and building and leading teams over the long haul to turn such a vision into reality despite the odds.”

Josh Wolfe said he hopes people agree with him, only later. Paul Johnson and Paul Sonkin say that good investment pitches include why the market will come around to an undervalued idea.

Meetings. “A mock-up is worth a thousand meetings.”

Media BS. “It’s easy to tie a bow around the Behance story and I found it interesting that it was anything but.” The media business isn’t always about telling the truth. Andre Agassi for example, was given the glasses and the line at the end of a photo shoot and it became his motif. It wasn’t planned. It wasn’t him. But it took the narrative.

Argue well. One of the most important part of an organization is good discussion. James Mattis said that if you don’t bring up your shortcomings internally, the enemy will point them out for you. We’ll leave with four more quotes from Scott.

“Is it permissible for people to talk to you and raising their hand and saying ‘I disagree.’”

“We were proud of the fact that we could go in a room, duke it out, and it was a very healthy process because we were exposing each other’s blind spots.”

“I’ve always kept an elephant list, the third rail things nobody wants to talk about and I try to interject one or two elephants whenever we’re together.”

“This is a key part of kind of eliminating the organizational debt that accrues in any organization. Organizational debt is the accumulation of decisions leaders should have made but didn’t.”

Paul Johnson and Paul Sonkin are the authors of Pitch the Perfect Investment, a book they say is written for recent graduates, MBAs, and portfolio managers. They wanted to write the book, in part because, “It’s been our experience that once you’re a couple of years out of school and in the business you know everything.”

They are wrong about who this book is for.

This book could be for any organization. “We tried to create something with staying power,” said Sonkin. Many businesses search for alpha, “a variant perspective” as their differentiator.

Let’s see how.

…

All organizations need good communication. “Not getting an idea adopted into the portfolio is the equivalent of having no good ideas.” Scott Belsky opined the value of design to Debbie Millman and this obstacle exists in sports too.

The solution tends to be ease. Warren Buffett writes with ease, “I’m addressing partners. There’re 600,000 of them, but in my mind I usually have my two sisters.” Buffett is a great stock picker but he’s also avoided redemption stampedes.

Buffett doesn’t pontificate, he humanizes because the type of language matters. Michael Lewis wrote in Moneyball, “He (Paul DePodesta) doesn’t explain anything because Billy doesn’t want him to. Billy was forever telling Paul that when you try to explain probability theory to baseball guys, you just end up confusing them.”

What works in sports is visual and back and forth. Daryl Morey said it’s a “give and take,” in a relationship “where both of us (Morey and James Harden) can give feedback to each other that sometimes isn’t easy. Like, I’m not seeing what you’re seeing, let’s talk about it.”

In an investment shop, said Johnson, the managers need to give good feedback and the analysts need to ask more questions. Managers need to say (only) ‘No’ less and analysts need to ask ‘Why’ more. “They’re talking essentially two different languages which is why Paul and I tend to think of this as couple’s counseling.”

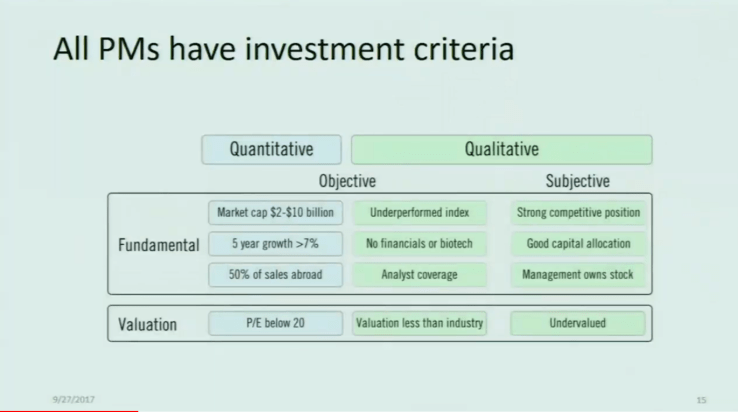

Their YouTube talk is full of good slides like this one and the 2X2 shows where communications can fall through the cracks.

Quantitative fundamentals are the easiest thing to get right because they are the most concrete whereas qualitative subjective valuations are much more nebulous. How much insider ownership matters? How large must a moat be?

Managers must be clear about their unstated subjective criteria if they want a decentralized command structure. The DC works for TV, AI, and Pizza. It works because the people closest to the situation know the most about it.

For analysts, it means figuring out four things; how much can I make, how much can I lose, why haven’t others grabbed this, when will others get it? These four questions are like the Five Whys, only for ‘Why is this a good investment?’

Analysts misstep because they misunderstand their mission. “Analysts say they get paid to analyze, no, they get paid to come up with ideas that go into the portfolio.”

Analysts should strive for the indirect approach. Paul Wagner, Tom Cruise’s agent, put it this way in Powerhouse:

I said, “I think it should be Tom Cruise,” and everybody went, “Whaaaaaaaaat?” Except Mike. He looked at me and said, “You do, do you? Hmm . . . interesting.” Then Dustin wanted to meet with Tom, so I said to Tom, “I have this crazy idea.” Others will probably say Tom was their idea and it probably “was,” because the art of agenting is to let clients have the great idea.

Johnson said, “I’ve met a lot of analysts that say, ‘I got very frustrated because before long it became his idea not my idea.’ That’s good. That’s what you want. You want them on the team and they’re not gonna buy unless it becomes their idea.”

Great organizations are Tolstoyian – alike. They have leaders that communicate well, they encourage debate, they have a diversity of thought, they have high expectations, they have extreme ownership, and they talk their customers and feel the winds of the real world.

Johnson’s and Sonkin’s book has those things and more specifics for investment managers and analysts. Sonkin’s YouTube channel has more interesting content and they teased (joked?) about a podcast coming soon.

Our first post on Marc Cohodes was based on his conversation with George Pearkes on Bespokecast. Today we’ll look at a sit-down interview with Grant Williams for Real Vision.

What’s great about short sellers like Cohodes (and Jim Chanos ) is their willingness to offer a different opinion. “I always say that free speech is free so long as it’s bullish,” said Cohodes in 2017. Internal, but cordial, dissent, argument, and conflict are good for organizations as steel sharpens steel.

…

“It all started in high school, I was never a good student. I was taking a tenth-grade economics class where we invested in stocks and I sort of got the bug then.” I wasn’t a great student, is a common refrain but we shouldn’s assume school is good or bad.

School is school. That said, lots of entrepreneurs like Peter Rahal don’t fit in school. Katrina Lake rearranged her schedule so school fit around her business. Tiffany Zhong said, “I don’t think everyone should drop out. There’s a lot more to that. What will you be doing instead and who will you be doing it with?”

For highly motivated, focused, and intelligent people the opportunity cost of school is too high. For most everyone else it’s not.

Cohode’s first investment was in coin drop arcade machines. For research, he visited arcades, talked the owners, and found that business was slowing. “I realized at the time that this isn’t for everyone and I’m genetically mutated to have the short selling gene.”

Getting as close to the customer as possible is where the best data is. “My rule of thumb is this, Chanos made so much sense when he was unwinding this Baldwin United business that it was a fraud. It made so much sense and I overlaid it against the long story which was so convoluted and made so little sense.”

But that Baldwin United trade went against the people and associates Cohodes worked for. “I didn’t mind taking shit (for selling Baldwin United) from the powers that be at the bank.” Organization work better with top-down support. Organization work better pushing down support, not directives. Organizations work better that way, but Marc’s independence made it indifferent.

Cohodes warns that “thesis creep is fatal” and as the facts, people, or situations change the investors must consider changing too.

Marc tries to find situations where the creep is less likely to creep. He’s uninterested in Tesla which is “one of these tastes great, less filling names. Elon says it tastes great, shorts says it’s less filling.” Tesla has too much sizzle around the steak that the company could run on fumes until it’s a great business.

Shorting is like lifeguard training, said Cohodes; reach, throw, row, go. You want to carefully try to save another person and only take risks when there’s no other option. “There are some guys who are interested in wresting a jaguar out of a tree. I’m interested in when a guy shoots the Jaguar out of a tree I’ll go in and cut him up. I don’t tackle anything that has momentum, something that’s un-analyzable, something that’s too hot. Like the FAANG stocks. I could care less.”

And, “I kind of view myself as a huge fish that’s sitting in the water near a waterfall. I’m just sort of meandering, not letting the current push me one way or the other. I’m watching all the food sources come down the waterfall. I’m thinking, ‘Do I want shrimp today? Do I want plankton today? Do I want a minnow today?'”

And, “I try to get into situations where I have a jump. Where I can out analyze, out think, or out hustle.”

Around the 49:00 mark there’s a nice conversation about Cohodes’s experiences in 2008 with Goldman Sachs and his investments. It’s a good reminder that we all operate in a system and all systems have rules that seem permanent but that can change in a moment.

To find the right shrimp, to find a jaguar that’s been wrestled to the ground, to find situations he can out hustle others, Cohodes has to know his shit. He does. “What people don’t realize is that I’m an investor. In life, you can be an investor or a trader. I’m an investor whose specialty is on the short side. When I short a company I know it better than the guy running it.”

When investigating Badger Daylight, “I started calling various North American operators and asked what their market was growing by and they said 2-3%. I asked how some can think it’s going to grow at 30-40% and the operators say those people are full of shit and they’re lying.”

Then he puts stuff on Twitter and “I get all sorts of feedback” from former customers, suppliers, competitors, regulators. Andrew McAfee and Erik Brynjolfsson noted this change in their book Machine, Platform, Crowd where the masses can come to better solutions than the masters.

Cohodes gets maligned because he’s direct with bad news when we want to hear good. We could all be more like Rick Federico, who called Cohodes and said if you’re going to short P.F. Chang’s at least call me first and I’ll address your issues. It’s like Michael Ovitz wrote, “When you tell someone the truth, all they can do is get upset – they can’t call you an idiot.”