Supported by Greenhaven Road Capital, finding value off the beaten path.

Paul Johnson and Paul Sonkin are the authors of Pitch the Perfect Investment, a book they say is written for recent graduates, MBAs, and portfolio managers. They wanted to write the book, in part because, “It’s been our experience that once you’re a couple of years out of school and in the business you know everything.”

They are wrong about who this book is for.

This book could be for any organization. “We tried to create something with staying power,” said Sonkin. Many businesses search for alpha, “a variant perspective” as their differentiator.

Let’s see how.

…

All organizations need good communication. “Not getting an idea adopted into the portfolio is the equivalent of having no good ideas.” Scott Belsky opined the value of design to Debbie Millman and this obstacle exists in sports too.

The solution tends to be ease. Warren Buffett writes with ease, “I’m addressing partners. There’re 600,000 of them, but in my mind I usually have my two sisters.” Buffett is a great stock picker but he’s also avoided redemption stampedes.

Buffett doesn’t pontificate, he humanizes because the type of language matters. Michael Lewis wrote in Moneyball, “He (Paul DePodesta) doesn’t explain anything because Billy doesn’t want him to. Billy was forever telling Paul that when you try to explain probability theory to baseball guys, you just end up confusing them.”

What works in sports is visual and back and forth. Daryl Morey said it’s a “give and take,” in a relationship “where both of us (Morey and James Harden) can give feedback to each other that sometimes isn’t easy. Like, I’m not seeing what you’re seeing, let’s talk about it.”

In an investment shop, said Johnson, the managers need to give good feedback and the analysts need to ask more questions. Managers need to say (only) ‘No’ less and analysts need to ask ‘Why’ more. “They’re talking essentially two different languages which is why Paul and I tend to think of this as couple’s counseling.”

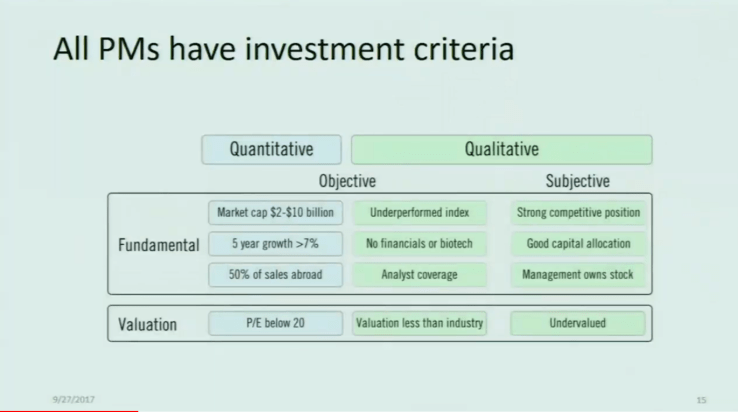

Their YouTube talk is full of good slides like this one and the 2X2 shows where communications can fall through the cracks.

Quantitative fundamentals are the easiest thing to get right because they are the most concrete whereas qualitative subjective valuations are much more nebulous. How much insider ownership matters? How large must a moat be?

Managers must be clear about their unstated subjective criteria if they want a decentralized command structure. The DC works for TV, AI, and Pizza. It works because the people closest to the situation know the most about it.

For analysts, it means figuring out four things; how much can I make, how much can I lose, why haven’t others grabbed this, when will others get it? These four questions are like the Five Whys, only for ‘Why is this a good investment?’

Analysts misstep because they misunderstand their mission. “Analysts say they get paid to analyze, no, they get paid to come up with ideas that go into the portfolio.”

Analysts should strive for the indirect approach. Paul Wagner, Tom Cruise’s agent, put it this way in Powerhouse:

I said, “I think it should be Tom Cruise,” and everybody went, “Whaaaaaaaaat?” Except Mike. He looked at me and said, “You do, do you? Hmm . . . interesting.” Then Dustin wanted to meet with Tom, so I said to Tom, “I have this crazy idea.” Others will probably say Tom was their idea and it probably “was,” because the art of agenting is to let clients have the great idea.

Johnson said, “I’ve met a lot of analysts that say, ‘I got very frustrated because before long it became his idea not my idea.’ That’s good. That’s what you want. You want them on the team and they’re not gonna buy unless it becomes their idea.”

It’s the Bill Walton, team-first approach.

…

Great organizations are Tolstoyian – alike. They have leaders that communicate well, they encourage debate, they have a diversity of thought, they have high expectations, they have extreme ownership, and they talk their customers and feel the winds of the real world.

Johnson’s and Sonkin’s book has those things and more specifics for investment managers and analysts. Sonkin’s YouTube channel has more interesting content and they teased (joked?) about a podcast coming soon.

Thanks for reading.

[…] Sonkin and Johnson noted that not getting ideas accepted by your boss is the equivalent of having no good ideas. Sometimes we need a thesaurus or dictionary to communicate our point. […]

LikeLike

[…] is something a lot of analysts, value investors or otherwise, miss said Sonkin and Johnson. They said there are four questions investment pitches must answer; how much can I make, how much […]

LikeLike

[…] so if you want the right behavior you really want the right language.” This echoes what Sonkin and Johnson said about good investing conversations. Misleading terms can sneak in “before you know it, […]

LikeLike

[…] is as important, if not more important, than the actual quantitative work that you do.” The Two Pauls remind analysts that their job isn’t to find good investments but to find good investments […]

LikeLike

[…] is as important, if not more important, than the actual quantitative work that you do.” The Pauls noted that not getting investment ideas into a portfolio is the same as not having any good […]

LikeLike

[…] persuading people to buy your ideas is a fundamental necessity.” Good ideas are not enough. The Pauls said that analysts aren’t paid to analyze. They’re paid to analyze and sell and idea to […]

LikeLike

[…] to USA basketball. Ed Catmull gave the backstory to ‘new Steve and old Steve.’ Paul Sonkin said that he reads the WSJ just to find the stupidest story. Sam Hinkie controlled everything but […]

LikeLike

[…] However, the largest potential gain in analytics (at least sports, circa 2020) is the implementation. It’s no use coming up with a good idea if you can’t get it into the portfolio. […]

LikeLike

[…] must convince her patients. The way we do each of these will change with time but these are the two parts any job. Put another way, it doesn’t matter how good the model is if people don’t follow […]

LikeLike