The Outsiders was good. What I liked most about William Thorndike’s book was the efficiency of it. Much like the CEOs he describes, the pace of the book is quick, and focused on the most important things.

The Outsiders was good. What I liked most about William Thorndike’s book was the efficiency of it. Much like the CEOs he describes, the pace of the book is quick, and focused on the most important things.The book is an attempt to bust the availability bias towards the contemporary CEO. The people on magazines. The “action-oriented leader who works in a gleaming office building and is surrounded by an army of hardworking fellow MBAs.” That leadership style may work for some, but it’s not the only — as the subtitle says — blueprint for success.

As I read six big themes came up:

- Be different and find truths.

- Keep an (inner) scorecard.

- Decentralize.

- Forecasting well is hard; a high investments (in time) and low return activity.

- Keep a low overhead.

- Think like a croc.

Being different & finding truths

I do not believe the consensus view is necessarily correct — Howard Marks

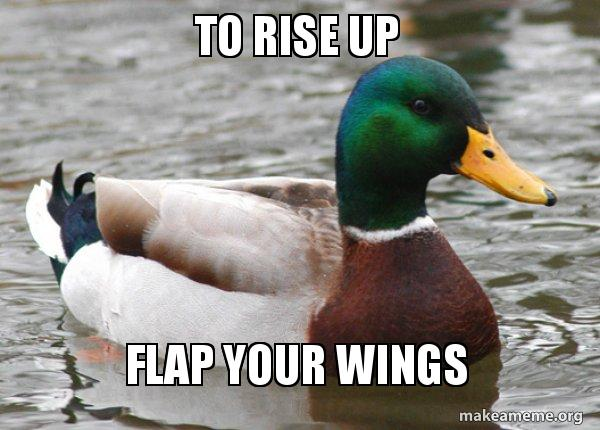

Each of the 8 outsiders Thorndike profiles earns their reputation because they outperformed both their industries/colleagues and the general market. This book looks at — in Warren Buffett’s words — ducks who flapped their wings and didn’t only sit on a rising tide.

To rise faster than the market, the outsiders had to be different. They have to answer the question Peter Thiel asks, what do you believe that is true that nobody else believes?

How did the outsiders do this?

For starters, most outsiders had “fresh eyes” and could “take a broom to the cobwebs,” writes Thorndike. They were well educated, yet poorly experienced as executives. This was a plus. They never succumbed to the things have always been this way momentum.

Another thing they did was relentlessly pursue the truth.“As a group they were, at their core, rational and pragmatic, agnostic, and clear eyed,” writes Thorndike.

“You are not right because others agree with you, but because your facts and reasoning are sound.” — Benjamin Graham

Finally, they were emotionally tough. It’s not easy to be different. Katherine Graham, for example, was on a “lonely path…a particularly difficult position for the only female executive in a high-profile, clubby, male-dominated industry.” Thorndike’s own experience mirror this. He writes, “in many ways the business world is like a high school cafeteria clouded with peer pressure.”

I saw this too in my research on startups that failed. Being different carries an emotional weight most underestimate.

One means of coping was to keep an inner scorecard.

Inner scorecard

If you are playing a different game, don’t keep the same score. Tom Murphy said, “The goal isn’t to have the longest trip, but to arrive at the station first using the least fuel.”

The outsiders did this mostly by focusing on cash and/or shareholder value. An emphasis on this metric meant matching means to those ends.

Thorndike writes that this was easier because many of these outsiders didn’t reside in New York City. “This distance helped insulate them from the din of Wall Street’s conventional wisdom.” They didn’t have someone yelling and telling that they were playing the wrong game.

Ed Catmull said that George Lucas moved to San Francisco to get away from the cacophony of Hollywood.

Seth Klarman recalls a client asking to come in and explain how they benchmarked his results. Klarman said, “I won’t meet with you. I’ll meet with you on anything else, but not that because it will change what I do.” Klarman didn’t want to know their score, how they kept it, or if it differed from his. He kept his own scorecard.

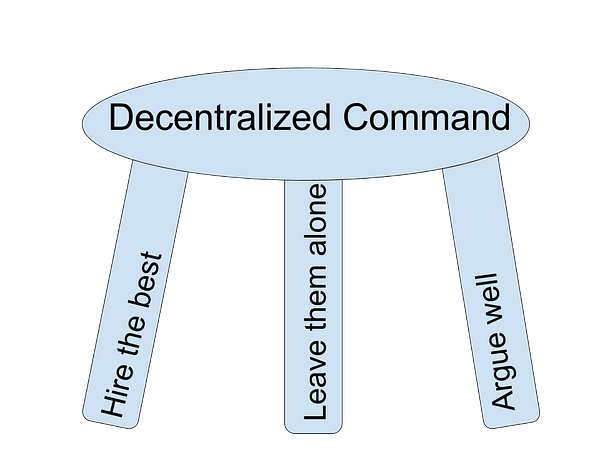

Decentralization

That so many great companies were run by so few people shouldn’t have surprised me, but it did. “Decentralization is the cornerstone of our philosophy,” read a CapCities annual report.

Tom Murphy said to “Hire the best people you can and leave them alone.” Warren Buffett suggested to “hire well, manage little.”

Decentralized command believes the people closest to the problem arrive at the best solutions. Andy Grove wrote:

“They (middle management) usually know more about upcoming change than the senior management because they spend so much time ‘outdoors’ where the winds of the real world blow in their faces.”

“I feel much safer back here in California than he does in ‘enemy territory.’ But is my perspective the right one? Or is his?”

Grove’s company — Intel — was saved because of decentralized command. “The process of adapting to change starts with employees who, through their daily work, adjust to the new outside forces.” It means letting people make their own good choices.

We’ve decentralized power in our operating business to a point just short of total abdication. — Charlie Munger

That said, communication still needs to happen. A third leg of the stool for decentralized command is arguing well.

Caesar Sweitzer said his Office of the Chairman meetings were “wrestling matches conducted in a constructive, collegial way.”

Grove too encouraged good arguments, “we developed a style of ferociously arguing with one another while remaining friends.” Scott Pioli said part of the coaching evaluation with the New England Patriots was whether or not you had an opinion.

Forecasting

Me and yo’ daughter, got’s this thing going on

(We got a special kind of thing going on)

You say it’s puppy love

We say it’s full grown

Hope that we feel this, feel this way forever

You can plan a pretty picnic

But you can’t predict the weather, Ms. Jackson– Outkast

The outsiders were great time managers. None fretted about appearances, and all committed to work with high returns. That meant reading, getting their hands dirty, and talking to people smarter than them. It meant few meetings, public relations, or forecasting.

“My only plan is to keep coming to work each day,” said Henry Singleton, “I like to steer the boat each day rather than plan ahead way into the future.”

The outsiders spend more time in the moment than in the future. Though Thorndike doesn’t address it in the book, I have two guesses why:

- The future is hard to predict.

- Plans have an anchoring effect.

Not only is the future hard to predict, but we tend to overestimate our own abilities. We watch sports because the players are great, but also think I could have done better than that(!) at each drop or missed putt. Maybe, but probably not.

Plans also anchor your thinking. Once you have a plan you have this thingand you start to compare options to the thing. It’s easy to get anchored to the thing.

Daniel Kahneman compares anchoring to ballparks. The anchor is the epicenter and once we drop it, it’s hard to move. If you peg returns or cost or anything to your thing, it becomes the comparison until it’s dislodged. Dislodging, of course, comes with a price of energy, time, and even money. The outsiders avoid this fuss.

Instead, Outsiders thought like crocodiles (more on that in a moment).

Low overhead

Here’s an easy business tip, keep a low overhead. “There’s an apparent inverse correlation between the construction of elaborate new headquarter buildings and investor returns,” writes Thorndike. Specifically debt interest, the evil twin of compound interest. Each outsider used debt like a chainsaw, with care and attention.

Without numerical fluency, in the part of life most of us inhibit, you are like a one-legged man in an ass-kicking contest. — Charlie Munger

Munger’s suggestion for numerical fluency applies here. Understand debt payments and positive cash flow, and the acolytes for positive cash flow are many.

- Sophia Amoruso slowly stair stepped into larger spaces as she grew Nasty Gal.

- Ben Horowitz’s lower overhead helped him get cash flow positive and keep control of his company.

- Yvon Chouinard ate cat food before he founded Patagonia.

- The Instagram founders lived on peanut butter sandwiches, two computers, and a rented server when they founded their company.

- Michael Ovitz — and his fellow founders — used borrowed office furniture, gifted office supplies, and had wives answer the phones of the early CAA.

A lower overhead gives you time, it avoids the hedonic treadmills, and steers clear of dealing with loss aversion.

Like a crocodile

There’s a joke in NBA commentary that people don’t like to trade with the San Antonio Spurs because that team has made so many good trades people assume they’re on the wrong end of one with them. The Spurs, like the outsiders, are crocodilian. They wait, wait, wait, and then GO!

Time after time a non-outsider CEO paid too much for an asset, failed to seize the opportunity, and needed to sell it in a worse climate than when they bought it. They were like a thirsty animal, needing any source of water. The outsiders were the crocodile.

- John Malone —scooped up Metropolitan Cable Companies

- Katherine Graham — scooped up overleveraged newspaper publishers

- Warren Buffett — scooped up a portion of Goldman Sachs

Not from the book, but applicable.

- Bill Belichick — scooped up Randy Moss from the Oakland Raiders.

The best managers never paid too much. Each outsider in the book had some level they would not cross, even by a hair. John Malone’s hurdle, for example, was 5X cash flow.

The crocodile does not pursue prey, it waits for it, and so did the outsiders. Warren Buffett describes his investing activity as “inactivity bordering on sloth.”

Richard Feynman espoused this mindset too. “The only way to solve such a thing (safe-cracking) is patience.”

[…] Six lessons learned from William Thorndike’s "The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success." (thewaiterspad) […]

LikeLike

[…] The Outsiders – The Waiter’s Pad […]

LikeLike

[…] Belichick evaluated assistant coaches based on their pushback and ideas. The Outsiders compared meetings to wrestling matches. Jeff Bezos and Andy Grove argue well with their […]

LikeLike

[…] succeed all the time. Charles Lindberg flew mail routes in whatever plane was available. In The Outsiders the twist is in the title. John Boyd was a fighter pilot who developed ground warfare […]

LikeLike

[…] CEOs – The Outsiders – writes William Thorndike have “crocodile-like […]

LikeLike

[…] book The Outsiders is great and we’ve covered it before – The Outsiders. In that post we introduced the decentralized command […]

LikeLike

[…] business leaders like The Outsiders and Intelligent Fanatics grow their businesses in any market condition. Great people grow their […]

LikeLike

[…] The other way is for decision making to be delegated down to the person at the problem. This is part of the decentralized command that Jocko Willink, Eric Maddox, and The Outsiders. […]

LikeLike

[…] capital. The best capital allocators are – probably – Intelligent Fanatics and Outsiders. Oh, and these two; Charlie Munger, early Warren Buffett, 2012 Warren Buffett, Bill Gates and […]

LikeLike